Handling PDF forms online is definitely a piece of cake with this PDF tool. Anyone can fill in indiana form 130 short here without trouble. To maintain our tool on the leading edge of practicality, we work to integrate user-oriented capabilities and improvements on a regular basis. We're always thankful for any suggestions - join us in revampimg how you work with PDF forms. Here's what you'll need to do to start:

Step 1: Click the "Get Form" button in the top section of this webpage to open our PDF editor.

Step 2: The editor provides you with the opportunity to change PDF forms in various ways. Improve it by including any text, correct what's already in the PDF, and put in a signature - all close at hand!

It's straightforward to fill out the document with our practical tutorial! This is what you need to do:

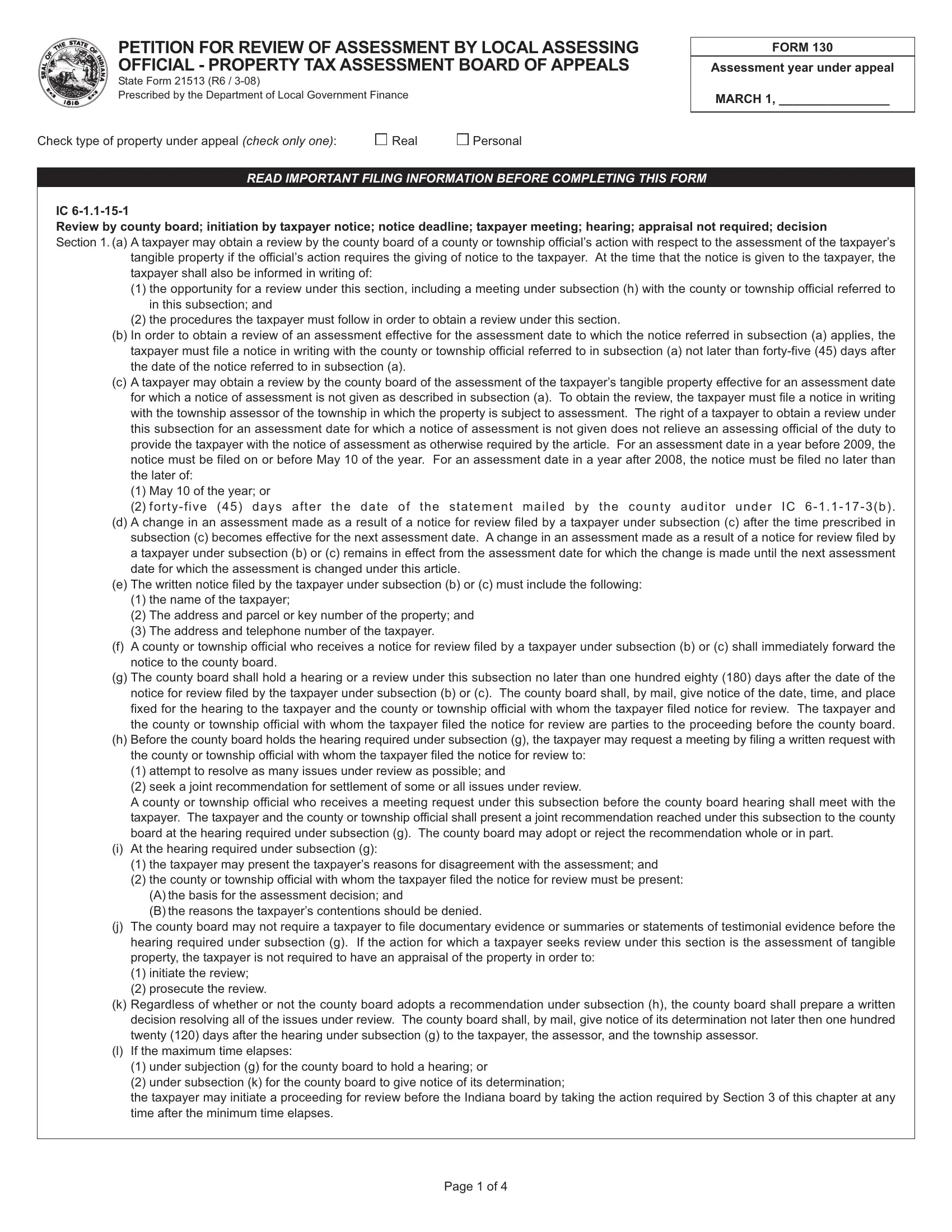

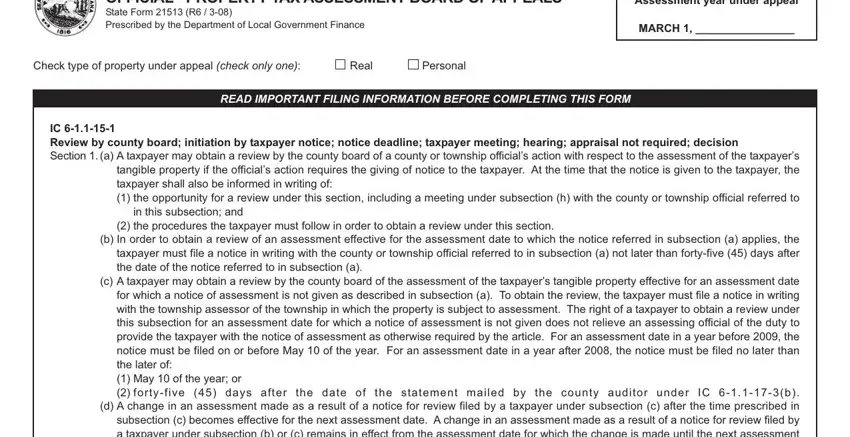

1. The indiana form 130 short needs particular details to be typed in. Make sure the subsequent blank fields are complete:

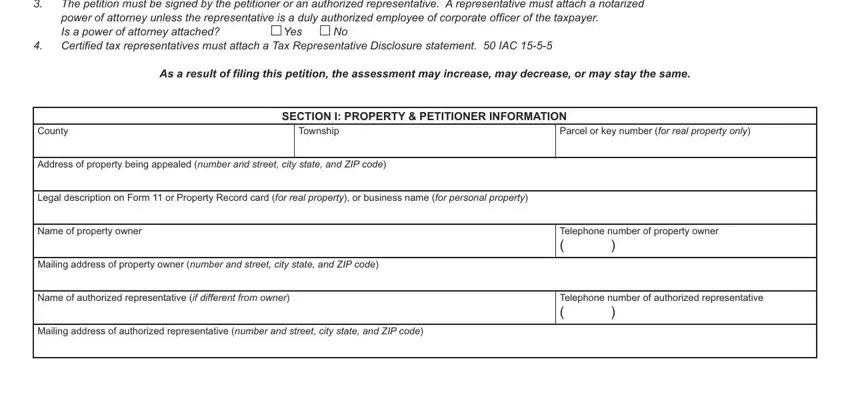

2. The third stage would be to complete these particular blank fields: GENERAL INSTRUCTIONS, Please print or type The, Yes, As a result of filing this, County, Township, Parcel or key number for real, SECTION I PROPERTY PETITIONER, Address of property being appealed, Legal description on Form or, Name of property owner, Mailing address of property owner, Name of authorized representative, Mailing address of authorized, and Telephone number of property owner.

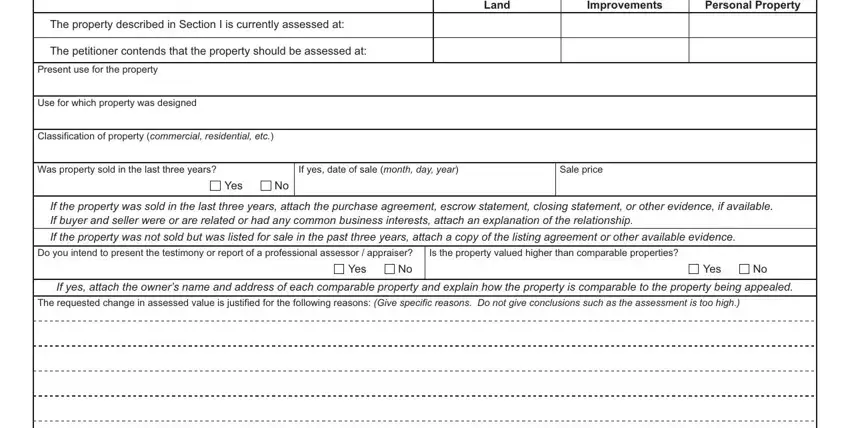

3. This next part is focused on Land, Improvements, Personal Property, The property described in Section, The petitioner contends that the, Present use for the property, Use for which property was designed, Classification of property, Was property sold in the last, If yes date of sale month day year, Sale price, Yes, If the property was sold in the, If the property was not sold but, and Do you intend to present the - fill in these blank fields.

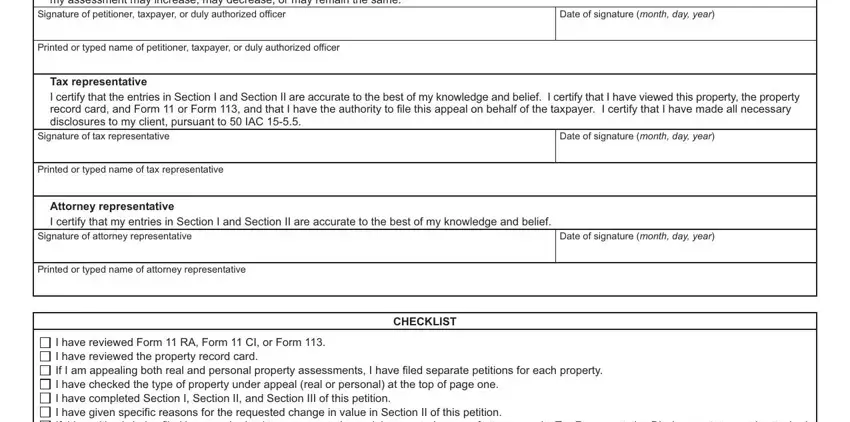

4. Filling in Petitioner taxpayer or duly, Signature of petitioner taxpayer, Date of signature month day year, Printed or typed name of, Tax representative I certify that, Signature of tax representative, Date of signature month day year, Printed or typed name of tax, Attorney representative I certify, Signature of attorney, Date of signature month day year, Printed or typed name of attorney, CHECKLIST, and I have reviewed Form RA Form CI is key in the fourth part - always take your time and fill in each and every blank!

5. To wrap up your document, this particular part requires a few additional fields. Filling out I have reviewed Form RA Form CI, and Page of should wrap up the process and you're going to be done in a short time!

Always be extremely attentive while completing I have reviewed Form RA Form CI and Page of, since this is where most people make some mistakes.

Step 3: Immediately after rereading the entries, press "Done" and you are good to go! Go for a free trial plan at FormsPal and gain instant access to indiana form 130 short - with all adjustments saved and accessible from your personal account page. FormsPal provides protected document tools devoid of personal data record-keeping or distributing. Be assured that your data is safe with us!