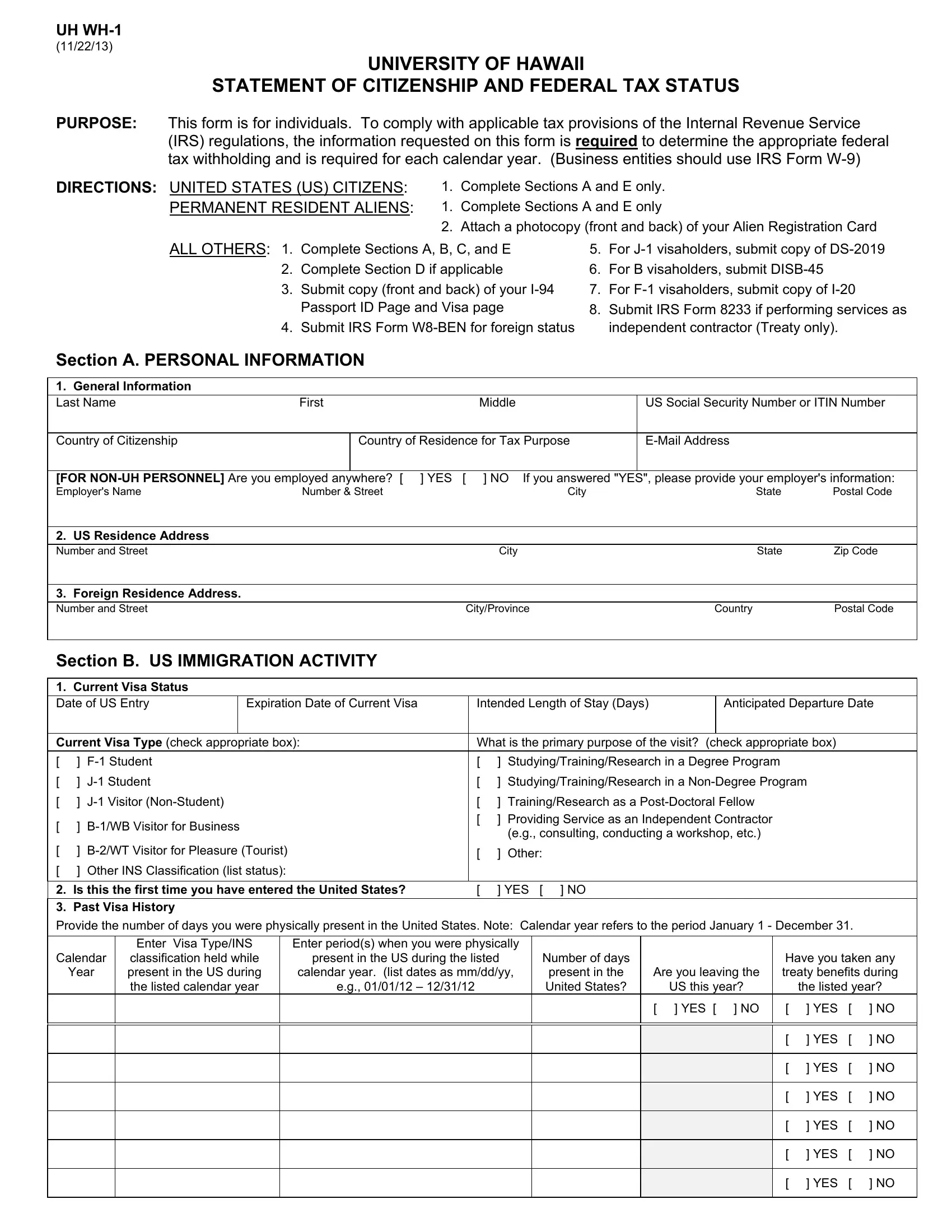

In today's globalized academic and professional environments, understanding the nuances of tax compliance is crucial for individuals interacting with institutions in the United States. One such critical document is the University of Hawaii's UH WH-1 form, which plays a pivotal role for individuals at this institution in navigating the complex landscape of tax obligations. The primary purpose of the UH WH-1 form, updated as of November 22, 2013, is to ensure compliance with the Internal Revenue Service (IRS) regulations by collecting necessary information to determine the appropriate federal tax withholding for individuals. This form is specifically designed for individuals, setting it apart from business entities, which are directed to use IRS Form W-9 instead. United States citizens, permanent resident aliens, and others with varied immigration and visa statuses, including J-1, B, and F-1 visaholders, are required to provide detailed personal, tax, and immigration information through this form. Each category of respondent must complete specific sections that cater to their status, ensuring accurate tax status determination and compliance with federal tax provisions. Additionally, the form serves an important function by facilitating the correct withholding of taxes, potentially leveraging tax treaties that could reduce the tax burden on the international members of the University of Hawaii community. The meticulous completion of the UH WH-1 form, including the certification of information under penalty of perjury and understanding the implications of tax treaty benefits, underscores its essential role in the international operation of academic institutions within the United States.

| Question | Answer |

|---|---|

| Form Name | Uh Wh 1 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | W8-BEN, SPT, visaholders, 2014 |

UH

(11/22/13)

UNIVERSITY OF HAWAII

STATEMENT OF CITIZENSHIP AND FEDERAL TAX STATUS

PURPOSE: This form is for individuals. To comply with applicable tax provisions of the Internal Revenue Service (IRS) regulations, the information requested on this form is required to determine the appropriate federal tax withholding and is required for each calendar year. (Business entities should use IRS Form

DIRECTIONS: UNITED STATES (US) CITIZENS: |

1. |

Complete Sections A and E only. |

PERMANENT RESIDENT ALIENS: |

1. |

Complete Sections A and E only |

|

2. |

Attach a photocopy (front and back) of your Alien Registration Card |

ALL OTHERS: 1. |

Complete Sections A, B, C, and E |

5. |

For |

2. |

Complete Section D if applicable |

6. |

For B visaholders, submit |

3. |

Submit copy (front and back) of your |

7. |

For |

|

Passport ID Page and Visa page |

8. |

Submit IRS Form 8233 if performing services as |

4. |

Submit IRS Form |

|

independent contractor (Treaty only). |

Section A. PERSONAL INFORMATION

1. General Information |

|

|

|

|

|

Last Name |

First |

Middle |

US Social Security Number or ITIN Number |

||

|

|

|

|

|

|

Country of Citizenship |

|

Country of Residence for Tax Purpose |

|

||

|

|

|

|

||

[FOR |

] YES [ ] NO If you answered "YES", please provide your employer's information: |

||||

Employer's Name |

Number & Street |

City |

State |

Postal Code |

|

2. |

US Residence Address |

|

|

|

Number and Street |

City |

State |

Zip Code |

|

|

|

|

|

|

3. |

Foreign Residence Address. |

|

|

|

|

|

|

|

|

Number and Street |

City/Province |

Country |

Postal Code |

|

Section B. US IMMIGRATION ACTIVITY

1. |

Current Visa Status |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Date of US Entry |

|

Expiration Date of Current Visa |

|

Intended Length of Stay (Days) |

|

Anticipated Departure Date |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Current Visa Type (check appropriate box): |

|

What is the primary purpose of the visit? (check appropriate box) |

|

|

||||||||||||||||

[ |

] |

|

|

|

|

|

[ |

] |

Studying/Training/Research in a Degree Program |

|

|

|

|

|||||||

[ |

] |

|

|

|

|

|

[ |

] |

Studying/Training/Research in a |

|

|

|||||||||

[ |

] |

|

|

[ |

] |

Training/Research as a |

|

|

|

|

||||||||||

[ |

] |

|

|

[ |

] |

Providing Service as an Independent Contractor |

|

|

|

|

||||||||||

|

|

|

|

(e.g., consulting, conducting a workshop, etc.) |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

[ |

] |

|

|

[ |

] |

Other: |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

[ |

] |

Other INS Classification (list status): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

2. |

Is this the first time you have entered the United States? |

[ |

] YES |

[ ] NO |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

3. |

Past Visa History |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Provide the number of days you were physically present in the United States. Note: Calendar year refers to the period January 1 - December 31. |

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

Enter |

Visa Type/INS |

|

Enter period(s) when you were physically |

|

|

|

|

|

|

|

|

|

|||||

Calendar |

classification held while |

|

present in the US during the listed |

|

Number of days |

|

|

|

|

Have you taken any |

||||||||||

|

Year |

present in the US during |

|

calendar year. (list dates as mm/dd/yy, |

present in the |

|

Are you leaving the |

|

treaty benefits during |

|||||||||||

|

|

|

the listed calendar year |

|

e.g., 01/01/12 – 12/31/12 |

|

|

|

United States? |

|

US this year? |

|

|

the listed year? |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[ ] YES [ ] NO |

|

[ |

] YES |

[ |

] NO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[ |

] YES |

[ |

] NO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[ |

] YES |

[ |

] NO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[ |

] YES |

[ |

] NO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[ |

] YES |

[ |

] NO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[ |

] YES |

[ |

] NO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[ |

] YES |

[ |

] NO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

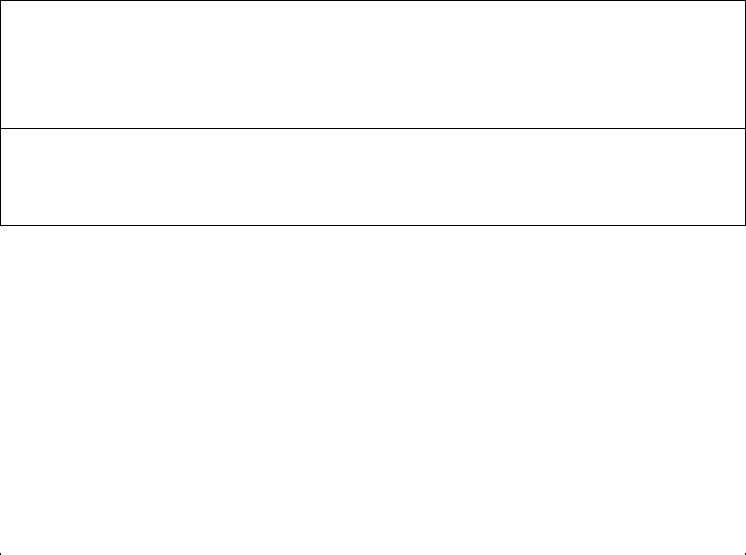

Section C. Tax Status Determination

STEP 1: Complete the Substantial Presence Test (SPT) by completing the table below. For F, J, M or Q Visaholders, please note the following:

For F, J, or M Student Visaholders:

For J or Q

Do NOT count any days during your first 5 years in the United States in which you held an F, J, or M student visa.

Do NOT count any days during your first 2 years in the previous 6 years in the United States in which you held a J or Q

|

|

ENTER TOTAL NUMBER OF DAYS |

|

|

|

|

|

|

CALENDAR |

PRESENT IN THE UNITED STATES |

|

CALCULATE TOTAL NUMBER OF DAYS TO |

|||

|

YEAR |

FOR EACH YEAR |

RATIO |

COUNT FOR EACH YEAR |

|

|

|

|

|

(A) |

(B) |

(A X B) |

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1/3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1/6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL # OF DAYS |

|

|

|

|

STEP 2: Please answer the following questions: |

|

|

|

|

|

||

|

|

|

|

|

|||

|

A. Does the TOTAL NUMBER OF DAYS TO COUNT for the current calendar year equal to 31 days or more? [ |

] YES |

[ |

] NO |

|||

|

B. Does the TOTAL # OF DAYS for all three years equal to 183 days or more? |

[ |

] YES |

[ |

] NO |

||

STEP 3: Determine your tax status:

If you marked “YES” to both questions A and B, then you passed the Substantial Presence Test and will be treated as a RESIDENT ALIEN (RA) FOR TAX PURPOSES for this calendar year. Go to and sign Section E below.

If you marked “No” to one or both questions, then you did not pass the Substantial Presence Test and will be treated as a NONRESIDENT ALIEN FOR TAX PURPOSES for this calendar year. Go to Section D below.

Section D. EXEMPTION FROM WITHHOLDING FOR THE NONRESIDENT ALIEN

1.All Payments made to Nonresident Aliens are subject to US federal tax withholding at a statutory rate of 30%.

However, you may claim an exemption from withholding or reduced rate via a US Tax Treaty if you meet the following requirements:

a. You must be a resident of a country that has a tax treaty with the US. (Consult IRS Publication 901, US Tax Treaties, at

Scholarship or Fellowship Article for Scholarship, Fellowship, Traineeship, and Stipend Payments.

OR

Independent Personal Services Article for Fee for Services, Honoraria, and Reportable Travel payments.

b.You must meet all requirements regarding residency, time, and dollar limitations described in the tax treaty.

c.You must have a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) to claim a treaty exemption.

2.Do you want to claim a treaty exemption from US federal tax withholding? (Check one box only.)

[ |

] YES |

I am a resident of a country that has a tax treaty with the US and has an applicable tax treaty article. Therefore, I claim |

|

|

exemption from US tax withholding via a US Tax Treaty with _________________________, my country of residence. |

|

|

I have attached one of the following IRS forms: (Consult IRS website for Forms and Instructions at |

|

|

http://www.irs.gov/formspubs/index.html) |

|

|

IRS Form 8233 for Fee for Services, Honoraria, and Reportable Travel payments. |

|

|

OR |

|

|

IRS Form |

[ |

] NO |

I choose not to claim a treaty exemption from US tax withholding, even though I am a resident of a country that has a tax |

|

|

treaty with the US and an applicable treaty article. I understand taxes will be withheld at 14% (Scholarships, Fellowship, |

|

|

Traineeship, or Stipend) or 30% (All other payments.). |

[ |

] NO |

I cannot claim a treaty exemption from US tax withholding because I do not meet the requirements stated in Part 1 above. |

|

|

I understand taxes will be withheld at 14% (Scholarships, Fellowship, Traineeship, or Stipend) or 30% (All other payments). |

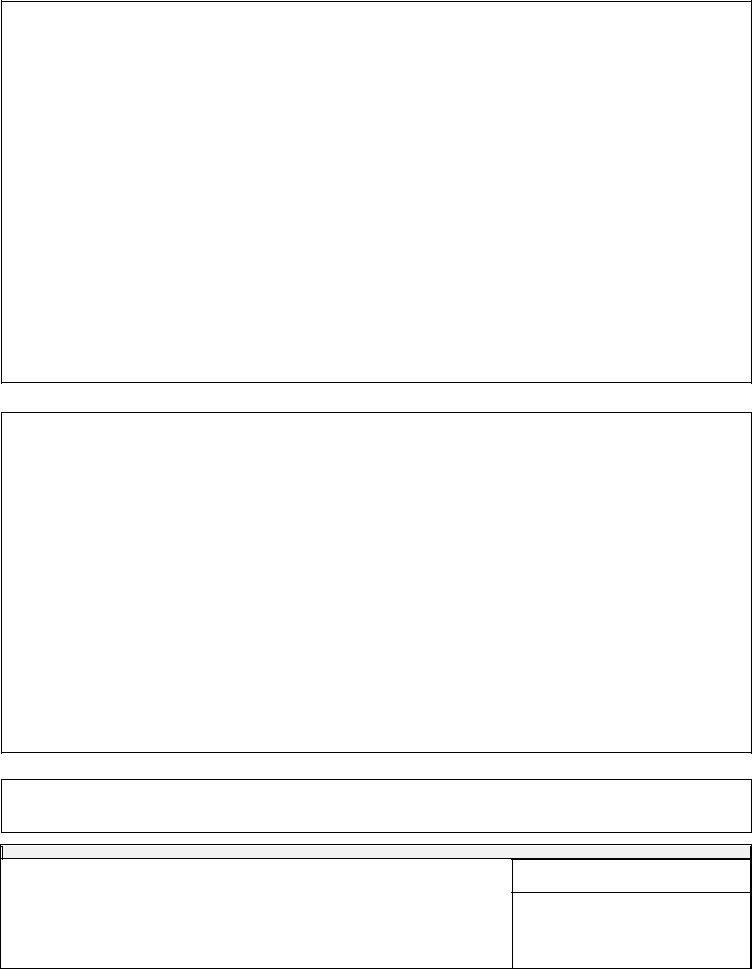

Section E. CERTIFICATION OF INFORMATION PROVIDED ON THIS FORM

Under penalties of perjury, I certify the information entered above is correct; and if a reduced rate of exemption from tax applies, I further certify that I have complied with all tax treaty requirements to qualify for the reduced rate. (For Resident Aliens, IRS has not notified me of backup withholding.)

Signature:Date:

Disbursing Office Use Only

Tax |

|

[ ] US Citizen |

|

|

[ ] Permanent Resident Alien |

Status: |

[ ] Resident Alien for Tax Purposes (SPT exp 12/____) |

|

[ ] Nonresident Alien |

||

|

|

|

|||

|

|

|

|

||

Nonresident Withholding: |

|

Expiration Date |

|||

[ |

] Statutory Rate of 30% |

Form 8233 |

______________ |

||

[ |

] Reduced Rate of 14% or ___% |

Form |

______________ |

||

[ |

] Exempt |

Form |

______________ |

||

|

|

|

|

|

|

Vendor Code

1099/1042 & WH Ind:

Initials |

Date |

|

|