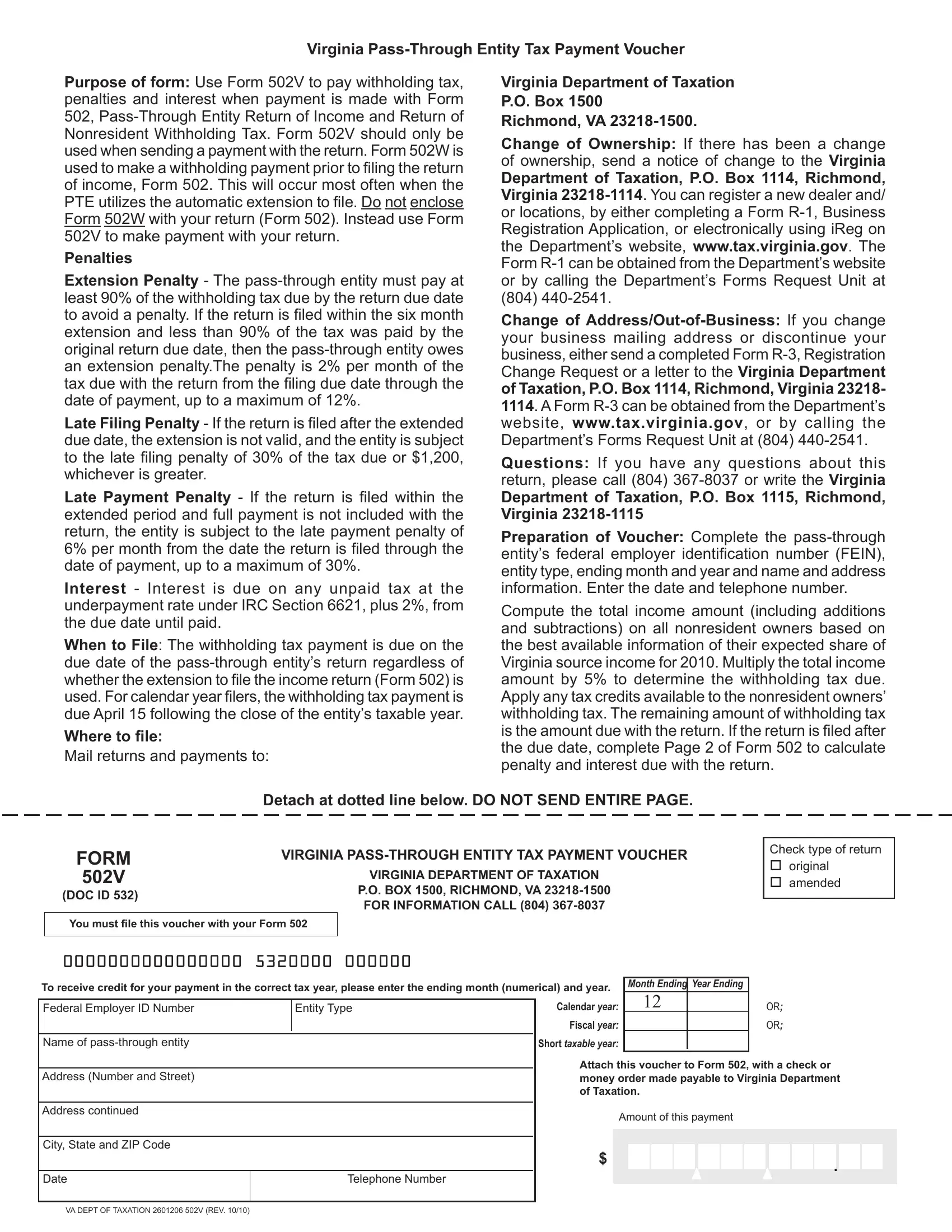

The intricacies of the Virginia Pass-Through Entity Tax Payment Voucher (Form 502V) underscore the complexities of tax compliance for pass-through entities within the state. This form plays a critical role in ensuring that withholding taxes, penalties, and interest are properly accounted for and paid in conjunction with the filing of Form 502, the Pass-Through Entity Return of Income. Unique to the process of making payments alongside the return, Form 502V must be utilized specifically in this context, with Form 502W designated for withholding payments prior to the return filing. Notably, the form outlines a penalty structure for entities that fail to meet the minimum payment threshold by the due date or that file returns late, including a specific extension penalty and late filing penalty, alongside penalties for late payments and associated interest charges. The due date for these payments aligns with the pass-through entity’s return due date, facilitating a streamlined process for calendar year filers and requiring attention to specified mailing addresses for submissions. Additionally, changes in ownership or business details necessitate further communication with the Virginia Department of Taxation, underscoring the importance of accurate and up-to-date business information. The preparation of the voucher itself demands meticulous attention to details including the federal employer identification number, entity type, and pertinent financial information, ensuring that the withholding tax due is accurately calculated and remitted. In sum, the Form 502V stands as a crucial component of the tax filing process for Virginia’s pass-through entities, framing a structured approach to tax liabilities and compliance.

| Question | Answer |

|---|---|

| Form Name | Va Form 502V |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | form 502v, virginia form 502v, 502V, subtractions |

Virginia

Purpose of form: Use Form 502V to pay withholding tax, penalties and interest when payment is made with Form 502,

used when sending a payment with the return. Form 502W is used to make a withholding payment prior to iling the return

of income, Form 502. This will occur most often when the PTE utilizes the automatic extension to ile. Do not enclose

Form 502W with your return (Form 502). Instead use Form 502V to make payment with your return.

Penalties

Extension Penalty - The

least 90% of the withholding tax due by the return due date to avoid a penalty. If the return is iled within the six month

extension and less than 90% of the tax was paid by the original return due date, then the

an extension penalty.The penalty is 2% per month of the tax due with the return from the iling due date through the

date of payment, up to a maximum of 12%.

Late Filing Penalty - If the return is iled after the extended

due date, the extension is not valid, and the entity is subject to the late iling penalty of 30% of the tax due or $1,200,

whichever is greater.

Late Payment Penalty - If the return is iled within the

extended period and full payment is not included with the return, the entity is subject to the late payment penalty of

6% per month from the date the return is iled through the date of payment, up to a maximum of 30%.

Interest - Interest is due on any unpaid tax at the underpayment rate under IRC Section 6621, plus 2%, from the due date until paid.

When to File: The withholding tax payment is due on the

due date of the

due April 15 following the close of the entity’s taxable year.

Where to ile:

Mail returns and payments to:

Virginia Department of Taxation

P.O. Box 1500

Richmond, VA

Change of Ownership: If there has been a change of ownership, send a notice of change to the Virginia

Department of Taxation, P.O. Box 1114, Richmond, Virginia

Registration Application, or electronically using iReg on the Department’s website, www.tax.virginia.gov. The

Form

Change of

your business mailing address or discontinue your business, either send a completed Form

Change Request or a letter to the Virginia Department

of Taxation, P.O. Box 1114, Richmond, Virginia 23218- 1114. A Form

Department’s Forms Request Unit at (804)

Questions: If you have any questions about this return, please call (804)

Department of Taxation, P.O. Box 1115, Richmond, Virginia

Preparation of Voucher: Complete the

entity type, ending month and year and name and address information. Enter the date and telephone number.

Compute the total income amount (including additions and subtractions) on all nonresident owners based on the best available information of their expected share of Virginia source income for 2010. Multiply the total income amount by 5% to determine the withholding tax due. Apply any tax credits available to the nonresident owners’

withholding tax. The remaining amount of withholding tax is the amount due with the return. If the return is iled after

the due date, complete Page 2 of Form 502 to calculate penalty and interest due with the return.

Detach at dotted line below. DO NOT SEND ENTIRE PAGE.

FORM |

VIRGINIA |

502V |

VIRGINIA DEPARTMENT OF TAXATION |

(DOC ID 532) |

P.O. BOX 1500, RICHMOND, VA |

|

FOR INFORMATION CALL (804) |

||

|

||

You must ile this voucher with your Form 502 |

|

|

|

|

Check type of return original amended

0000000000000000 |

5320000 000000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

To receive credit for your payment in the correct tax year, please enter the ending month (numerical) and year. |

|

Month Ending |

Year Ending |

|

|

|

|

|

|

|

|||||||||

|

|

|

CALENDAR year: |

|

12 |

|

|

|

|

|

|

OR; |

|||||||

Federal Employer ID Number |

|

Entity Type |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

FISCAL year: |

|

|

|

|

|

|

|

|

|

OR; |

||||||

Name of |

|

|

SHORT taxable year: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attach this voucher to Form 502, with a check or |

||||||||||||||||

Address (Number and Street) |

|

|

|||||||||||||||||

|

|

money order made payable to Virginia Department |

|||||||||||||||||

|

|

|

of Taxation. |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address continued |

|

|

|

|

Amount of this payment |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, State and ZIP Code |

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date |

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VA DEPT OF TAXATION 2601206 502V (REV. 10/10)