The Withholding Exemption Certificate, designated as Form 499 R-4.1, serves a pivotal role in the financial relationship between employees and employers within the Commonwealth of Puerto Rico. Updated in December 2016, this form enables employees to communicate their eligibility for personal exemptions, exemptions for dependents, and allowances based on various deductions directly to their employers. This structured communication ensures that the withheld income tax accurately reflects an employee’s fiscal standing, leveraging regulations established by the Puerto Rico Internal Revenue Code of 2011. Significantly, the form includes options for married employees, military spouses under the Military Spouses Residency Relief Act, and young individuals aged between 16 and 26, to declare specific tax considerations. Additionally, it outlines the importance of accurately reporting these exemptions and allowances, as any changes require the filing of an amended certificate to maintain compliance with the Code. The form also integrates a provision for employees to authorize additional withholding at their discretion, reinforcing the flexibility and personalized approach to tax planning and compliance within Puerto Rico's tax framework. Through the proper completion and submission of this document, employees can ensure their employers withhold the correct amount of income tax, ultimately aligning their payroll deductions with their personal and dependent exemptions as well as their eligible deductions, thus avoiding potential misunderstandings and the inadvertent misapplication of tax liabilities.

| Question | Answer |

|---|---|

| Form Name | Withholding Exemption Certificate Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | puerto rico withholding form, puerto rico withholding, 499 r 4 1, puerto rico tax withholding form 2021 |

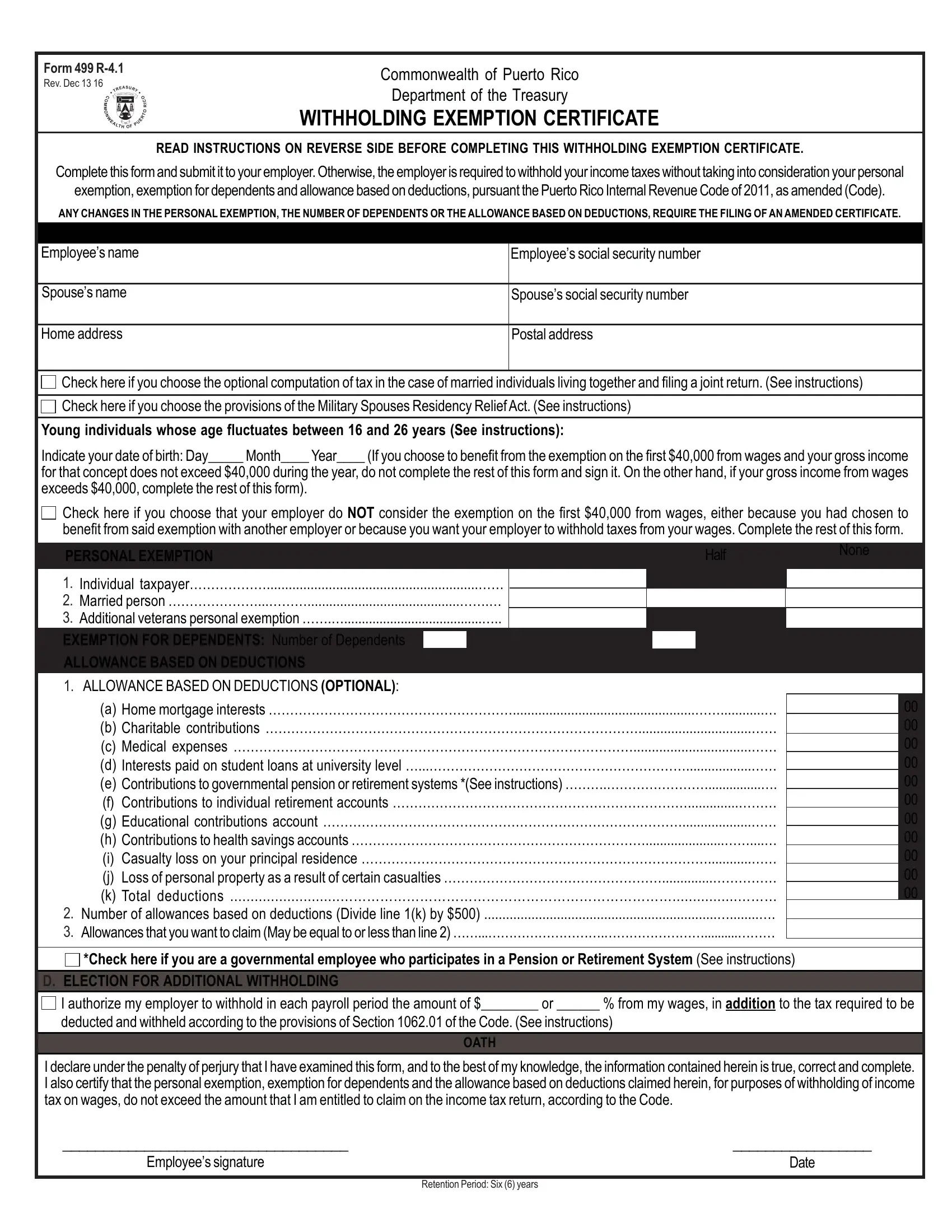

Form 499

Rev. Dec 13 16

Commonwealth of Puerto Rico

Department of the Treasury

WITHHOLDING EXEMPTION CERTIFICATE

READ INSTRUCTIONS ON REVERSE SIDE BEFORE COMPLETING THIS WITHHOLDING EXEMPTION CERTIFICATE.

Complete this form and submit it to your employer. Otherwise, the employer is required to withhold your income taxes without taking into consideration your personal

exemption, exemption for dependents and allowance based on deductions, pursuant the Puerto Rico Internal Revenue Code of 2011, as amended (Code).

ANY CHANGES IN THE PERSONAL EXEMPTION, THE NUMBER OF DEPENDENTS OR THE ALLOWANCE BASED ON DEDUCTIONS, REQUIRE THE FILING OF AN AMENDED CERTIFICATE.

FOR EMPLOYEE’S USE ONLY

Employee’s name

Spouse’s name

Employee’s social security number

Spouse’s social security number

Home address

Postal address

Check here if you choose the optional computation of tax in the case of married individuals living together and filing a joint return. (See instructions)

Check here if you choose the provisions of the Military Spouses Residency Relief Act. (See instructions)

Young individuals whose age fluctuates between 16 and 26 years (See instructions):

Indicate your date of birth: Day_____ Month____ Year____ (If you choose to benefit from the exemption on the first $40,000 from wages and your gross income

for that concept does not exceed $40,000 during the year, do not complete the rest of this form and sign it. On the other hand, if your gross income from wages exceeds $40,000, complete the rest of this form).

Check here if you choose that your employer do NOT consider the exemption on the first $40,000 from wages, either because you had chosen to benefit from said exemption with another employer or because you want your employer to withhold taxes from your wages. Complete the rest of this form.

A. PERSONAL EXEMPTION |

Complete |

Half |

None |

|

(less withholding) |

(more withholding) |

|||

1. |

Individual taxpayer………………..........................................................…… |

|

|

|

|

|

|

||

2. |

Married person …………………...………..........................................…….… |

|

|

|

3. |

Additional veterans personal exemption …….….......................................….. |

|

|

|

B. EXEMPTION FOR DEPENDENTS: Number of Dependents |

|

Complete Exemption |

|

Joint Custody |

C.ALLOWANCE BASED ON DEDUCTIONS

1.ALLOWANCE BASED ON DEDUCTIONS (OPTIONAL):

(a)Home mortgage interests …………………………………………………..................................................……............…

(b)Charitable contributions ……………………………………………………………………………...............................……

(c)Medical expenses …………………………………………………………………………………................................……

(d)Interests paid on student loans at university level …...……………………………………………………..................……

(e)Contributions to governmental pension or retirement systems *(See instructions) ……….……………………...............….

(f) Contributions to individual retirement accounts ……………………………………………………………..............………

(g)Educational contributions account …………………………………………………………………………...................……

(h)Contributions to health savings accounts ……………………………………………………………......................……....…

(i) Casualty loss on your principal residence ………………………………………………………………………............……

(j) Loss of personal property as a result of certain casualties ……………………………………………..............……………

(k)Total deductions ...........................…………………………………………………………………................………

2.Number of allowances based on deductions (Divide line 1(k) by $500) ................................................................…........….

3.Allowances that you want to claim (May be equal to or less than line 2) ……...……………………….……………………..........………

*Check here if you are a governmental employee who participates in a Pension or Retirement System (See instructions)

D. ELECTION FOR ADDITIONAL WITHHOLDING

00

00

00

00

00

00

00

00

00

00

00

I authorize my employer to withhold in each payroll period the amount of $________ or ______ % from my wages, in addition to the tax required to be

deducted and withheld according to the provisions of Section 1062.01 of the Code. (See instructions)

OATH

I declare under the penalty of perjury that I have examined this form, and to the best of my knowledge, the information contained herein is true, correct and complete. I also certify that the personal exemption, exemption for dependents and the allowance based on deductions claimed herein, for purposes of withholding of income tax on wages, do not exceed the amount that I am entitled to claim on the income tax return, according to the Code.

___________________________________ |

_________________ |

Employee’s signature |

Date |

Retention Period: Six (6) years

INSTRUCTIONS

The Withholding Exemption Certificate (Form 499

Complete the upper part of the form, indicating your name, social security number, home and postal address. If you are married, include your spouse’s name and social security number, and indicate if you choose the optional computation of tax in the case of married individuals living together and filing a joint return (optional computation), as provided by Section 1021.03 of the Puerto Rico Internal Revenue Code of 2011, as amended (Code).

Under the Military Spouses Residency Relief Act (MSRRS), if you are the spouse of an active service member that was transferred under military orders to a new military station in any of the states, possessions or territories of the United States or the District of Columbia, you can keep your original residence or domicile for tax purposes. Indicate if you elect this option so that the employer is not required to withhold income tax for Puerto Rico purposes. Nevertheless, you may be subject to the payment of federal estimated tax or from the state, possession or territory for which you elected to keep as your residence or the employer may withhold federal, local or state taxes, as applicable.

If you are a young individual resident of Puerto Rico whose age fluctuates between 16 and 26 years at the end of the taxable year, you are entitled to an exemption on the first $40,000 of gross income from wages. To benefit from this exemption, indicate your date of birth. If your annual wage is more than $40,000, the excess over the first $40,000 will be taxed as ordinary income, to the extent that this amount is more than the withholding exemption to which you are entitled.

It is important to point out, that if the young employee has more than one job, the limit of $40,000 shall be applied on the aggregate wages. That is, on the total of all wages even if they come from more than one employer.

Since the exemption cannot be applied to an amount larger than $40,000, you must notify the employer (or employers) of your election, for them not to consider the exemption as you have chosen to benefit from it with another employer. Also, you may choose not to benefit from this exemption and elect that your employer withholds tax on your wages.

PART A - PERSONAL EXEMPTION

Indicate with an “X” your option regarding the personal exemption that your employer will consider to determine the income tax to be withheld.

Line 1 – An individual taxpayer (single person, married that granted prenuptial agreement of total separation of assets or married not living with spouse) may claim or not the personal exemption. If you want to claim the complete personal exemption, mark the column titled “Complete”. On the other hand, if you choose to claim no exemption at all, you may do so by marking the column titled “None”. An individual taxpayer cannot choose to consider “Half” of his/her personal exemption.

Line 2 - Married couples are entitled to only one personal exemption, therefore, each spouse cannot claim the complete personal exemption. If you are a married person, and both spouses receive wages subject to withholding, both of you should agree on how to claim the personal exemption and shall mark the corresponding column. If the married couple determines that only one of them will consider the complete personal exemption, such spouse shall mark the column titled “Complete”. In such case, the other spouse shall mark the column titled “None”. If you agreed with your spouse to divide the personal exemption in half, indicate so by marking the column titled “Half”. If you do not want to claim the personal exemption, mark the column titled “None”.

If you are married and choose the optional computation, the personal exemption will be considered on a 50% basis for each spouse. Therefore, each spouse may choose to consider the complete personal exemption or no personal exemption at all regarding this 50%.

Line 3 – Every veteran is entitled to claim an additional personal exemption. The veteran may claim the complete additional personal exemption or may choose to claim no additional personal exemption at all.

PART B - EXEMPTION FOR DEPENDENTS

Indicate the number of dependents that will be considered for the withholding computation. It shall be the same as the number that you will claim as dependents on your income tax return. Indicate separately in the corresponding box, the children for which you are entitled to joint custody and have not released the claim to exemption. In these cases, only 50% of the exemption will be considered.

If you are an employee who elected the optional computation, your exemption for dependents will be 50% of the total amount provided by Section 1033.18(b) of the Code, since in such cases each spouse is entitled to claim only half of the exemption for dependents, as provided in Section 1021.03 of the Code.

The Code provides that every employer, who receives an exemption certificate from an employee in which the number of dependents claimed exceeds 8, shall submit a copy of such certificate to the Secretary of the Treasury, as well as a copy of any written statement received from the employee to support the information contained in the certificate.

PART C - ALLOWANCE BASED ON DEDUCTIONS

You are entitled to certain allowances based on deductions which your employer shall consider in the determination of the amount of income tax to be withheld.

Line 1 – You have the option to consider in the withholding computation, the deductions that you will be able to claim on your income tax return. Such deductions will reduce the

amount of tax that the employer will withhold on your wages. If you do not wish to consider these deductions in the computation, do not complete this line.

Enter on lines 1(a) through 1(j), the amount of these deductions that you estimate you will be entitled to claim on your return. Such deductions are subject to the limitations and requirements provided in Section 1033.15 of the Code.

If you are married and choose the optional computation, the number of allowances shall be determined by dividing the deductions among the spouses. In the case of home mortgage interests, charitable contributions, medical expenses, and loss on your principal residence or personal property as a result of certain casualties, include 50% of each deduction. In the case of contributions to governmental pension or retirement systems, Individual Retirement Accounts, Educational Contribution Accounts, Health Savings Accounts and interests paid on student loans at university level, include the amount that corresponds individually.

Line· 1(e) – If you are a governmental employee, you shall consider the contributions made to your pension or retirement system. This amount will be 10% of your annual wage or the amount established by the system to which you contribute. Indicate with an “X” in the box at the·end of this Part C, if you are a governmental employee who participates in a pension or retirement system. If you work for an agency which payroll is processed by the

Department of the Treasury, do not consider your contributions to the pension or retirement system on this line. This deduction will automatically be considered in the·withholding computation.

Line 2 – Divide the amount figured on line 1(k) by $500. Any fraction obtained as a result of the preceding division exceeding 50%, shall be considered as an additional allowance.

Line 3 – Indicate the allowances that you wish to claim, from the amount determined on line

2.If you file as a married person living with spouse and do not choose the optional computation, you and your spouse shall be allowed to divide the total allowances as you wish, but based on complete allowances. However, any allowance considered by one spouse cannot be claimed by the other spouse.

PART D – ELECTION FOR ADDITIONAL WITHHOLDING

Any employee may elect for his/her employer to withhold an amount in addition to the one required by Section 1062.01(e) of the Code. Under no circumstances, this option will be allowed for an amount less than the tax determined according to the withholding tables approved by the Secretary based on the tax rates provided by the Code.

OATH

You declare under penalty of perjury, that you have examined this form, and that to the best of your knowledge, the information contained therein is true, correct and complete.

SIGNATURE

This form must be signed and dated by the employee.

PENALTIES

Any employee required to submit a withholding exemption certificate to his/her employer, who willfully provides false or fraudulent information, or who willfully fails to provide information which would require an increase in the tax to be withheld, shall be guilty of a misdemeanor as provided in Section 6041.08 of the Code.

In the case of employees who elect to consider the allowance for deductions provided in Section 1062.01(c)(2)(A)(ii) of the Code, in addition to the criminal penalty mentioned in the above paragraph, if 70% of the tax attributable to income derived from wages subject to withholding exceeds the tax withheld at source on said income, there shall be added to the tax the smaller of: (1) an amount equal to such excess, or (2) an amount equal to 18% of the amount for which such tax so determined exceeds the tax withheld.

INSTRUCTIONS TO THE EMPLOYER

The employer shall consider the information provided by the employee on this Exemption Certificate with respect to the personal exemption, exemption for dependents and allowance based on deductions in order to make the withholding according to the Employer’s Guide on the Withholding of Income Tax at Source on Wages (Withholding Guide) for the corresponding taxable year.

If the employee elects the provisions of the MSRRA, no withholding of tax at source on wages shall be made for Puerto Rico purposes. Nevertheless, such wages may be subject to withholding of federal taxes according to the provisions of the Internal Revenue Service.

If the number of dependents exceeds 8, submit copy of this Certificate to the Fiscal Audit Bureau, as well as copy of any written statement received from the employee to support the information contained on the certificate.

Employee whose age fluctuates between 16 and 26 years: In order for the employee to benefit from the exemption on the first $40,000 from wages, he/she must complete the information required in the heading and provide the date of birth. If the annual wage is equal or less than $40,000, the employee will not complete the rest of the form although he/she should sign it. If the annual wage is for a greater amount, the excess of the first $40,000 over the withholding exemption amount (Appendix 1 of the Withholding Guide) will be subject to withholding of tax, as it corresponds. For that, the employee must complete the rest of the form.

The employee may choose for his/her employer NOT to consider this exemption, either because he had chosen to benefit from it with another employer or because he/she wants his/ her employer to withhold tax from his/her wages. In that case, in addition to selecting the corresponding box, he/she will complete Parts A through D, as applicable.