FormsPal's online PDF editor lets you fill out the 1120 Schedule D form directly in your browser with no software downloads required. Follow the steps below to complete, save, and download your finished form.

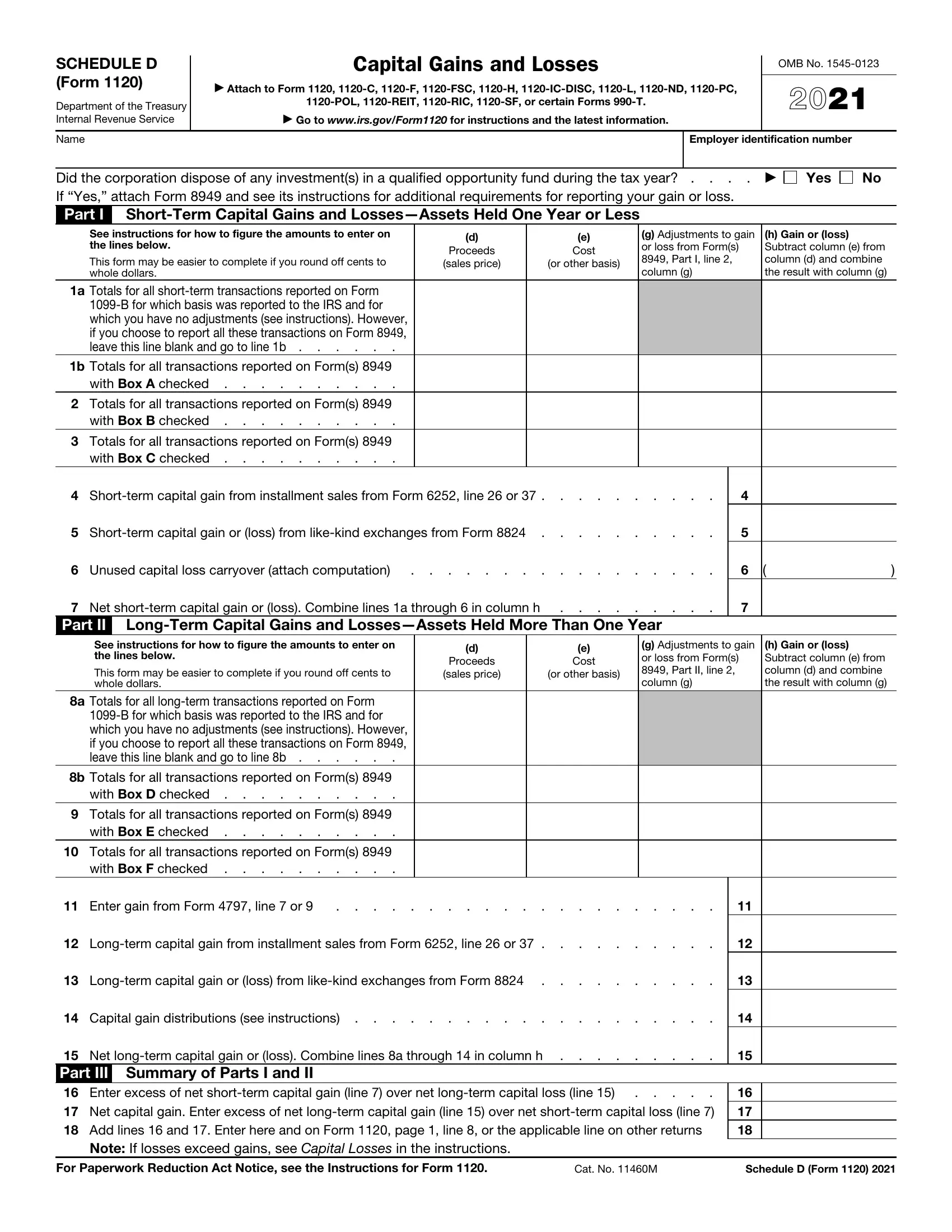

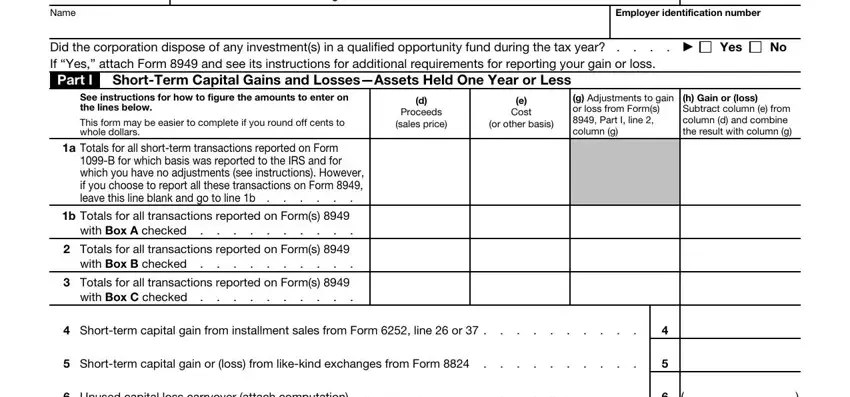

Step 1: Click the "Get Form" button at the top of this page to open the online editor. The 1120 Schedule D form loads immediately and is ready for data entry. Begin with Part I, which covers short-term capital transactions. For each transaction, enter the property description, acquisition and sale dates, sales price, cost or adjusted basis, and any adjustments for disallowed losses.

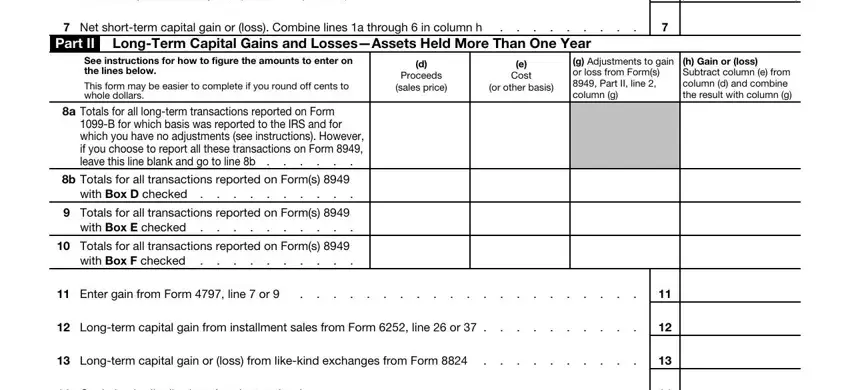

Step 2: The editor lets you update any text field, correct existing values, and add your signature as needed. Move to Part II for long-term capital transactions, which follow the same column structure as Part I. If you have multiple transactions, you may summarize them using the approved aggregated reporting method from Form 8949.

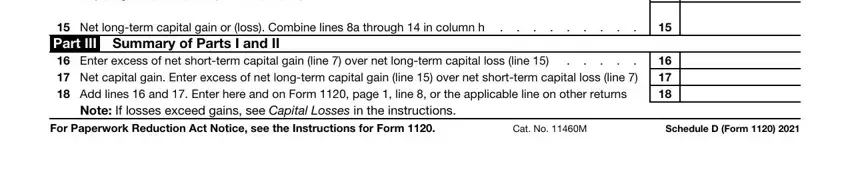

After completing Parts I and II, move to Part III. Enter the net short-term capital gain or loss from Part I and the net long-term capital gain or loss from Part II. The combined result on Part III is the amount that transfers to Form 1120. Review each entry carefully before finalizing, paying particular attention to the net long-term capital gain or loss line, which is a common source of errors.

Step 3: When you have reviewed all entries, click "Done" to save and finalize your 1120 Schedule D form. You can download a PDF copy, print it, or return later to make additional changes. FormsPal stores your data securely so it is ready whenever you need it.

Frequently Asked Questions About the 1120 Schedule D Form

What capital transactions go on Schedule D (Form 1120)?

Any sale or disposal of a capital asset held by the corporation during the tax year is reported on Schedule D. This includes stocks, bonds, and investment real estate. Business property sold at a gain may also qualify depending on how the asset was classified on the corporation's books.

Do I need Form 8949 when filing Schedule D?

In most cases, yes. Individual transactions are first reported on Form 8949, and the totals are then summarized on Schedule D. Some filers using an approved aggregated reporting method may enter totals directly on Schedule D without completing Form 8949 line by line.

What happens if the corporation reports a net capital loss on Schedule D?

A net capital loss cannot be deducted against ordinary income in the current year. The corporation may carry the loss back three years to offset capital gains from a prior return, which can produce a tax refund for that year. Any remaining loss not used in the carryback may be carried forward up to five years to reduce future capital gain income.

How long should corporations keep records related to Schedule D?

The IRS generally recommends keeping records that support amounts on a tax return for at least three years from the filing date. For capital assets, records of acquisition cost, improvements, and depreciation should be kept for as long as the asset is owned plus the carryback or carryforward period.