Filling out IRS Form 1120-A takes just a few steps using FormsPal's free online PDF editor. No software download is required. Open the form in your browser and complete each part in order.

How to Edit IRS Form 1120-A Online for Free

Step 1: Open the Form

Click the "Get Form" button at the top of this page to open Form 1120-A in the FormsPal editor. The form loads directly in your browser.

Step 2: Enter Corporate Identification

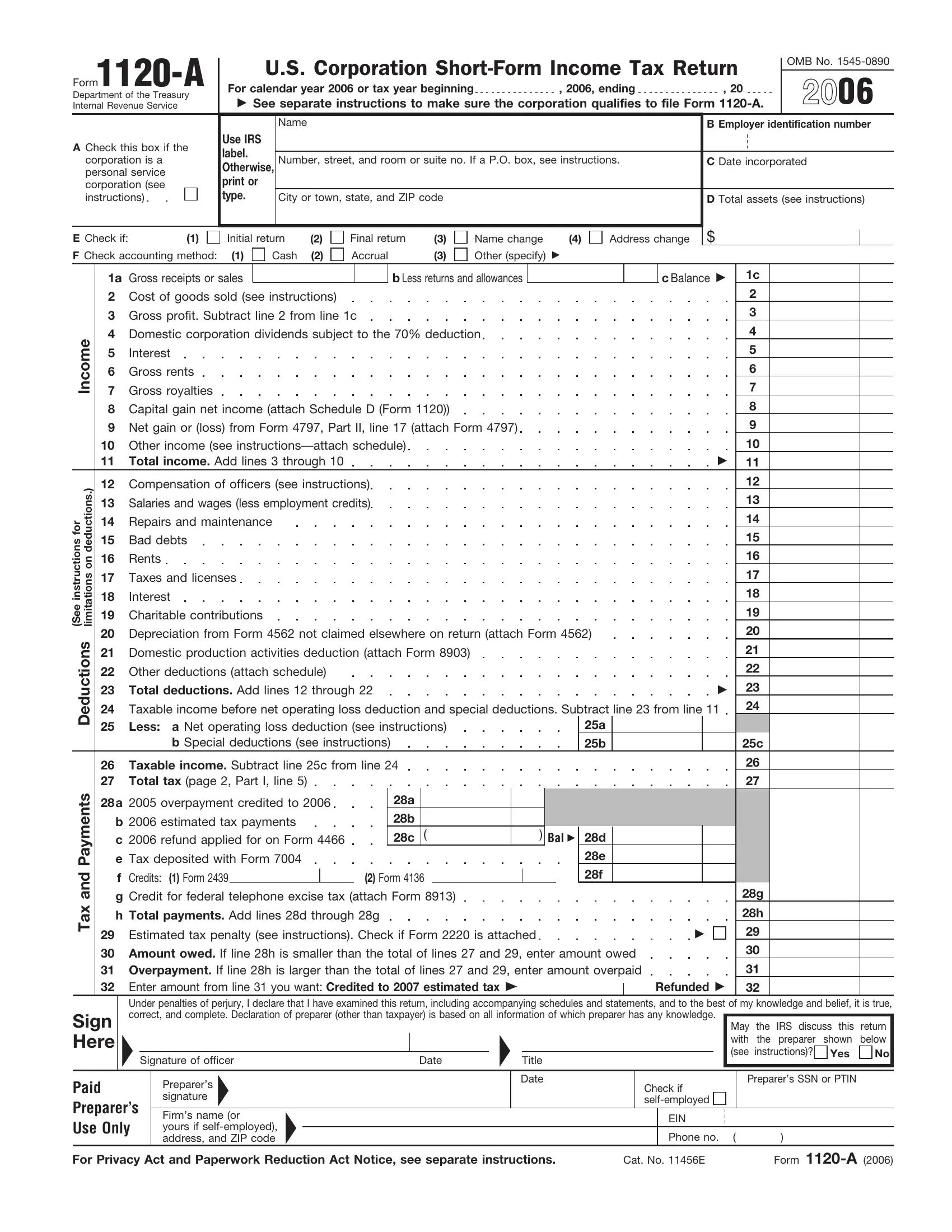

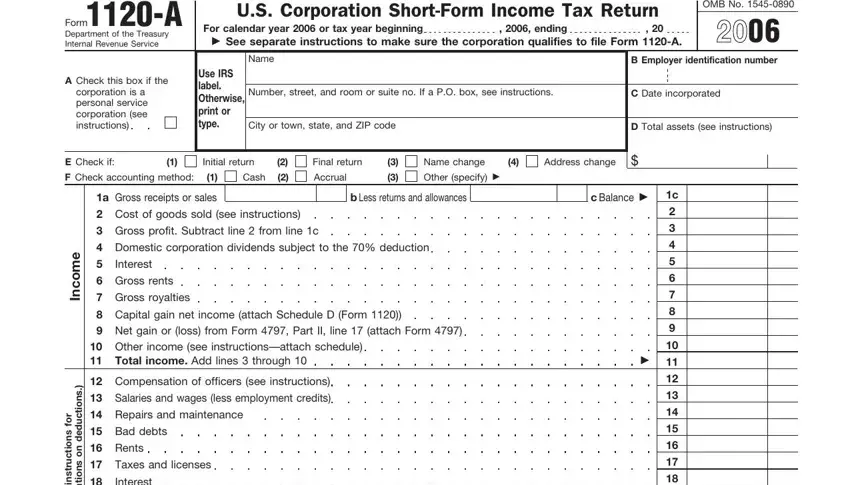

Fill in your corporation's legal name, address, employer identification number (EIN), and the applicable tax year at the top of the form. Verify the EIN matches IRS records before continuing. An incorrect EIN is one of the most common errors on Form 1120-A and can delay processing.

Step 3: Report Income and Deductions

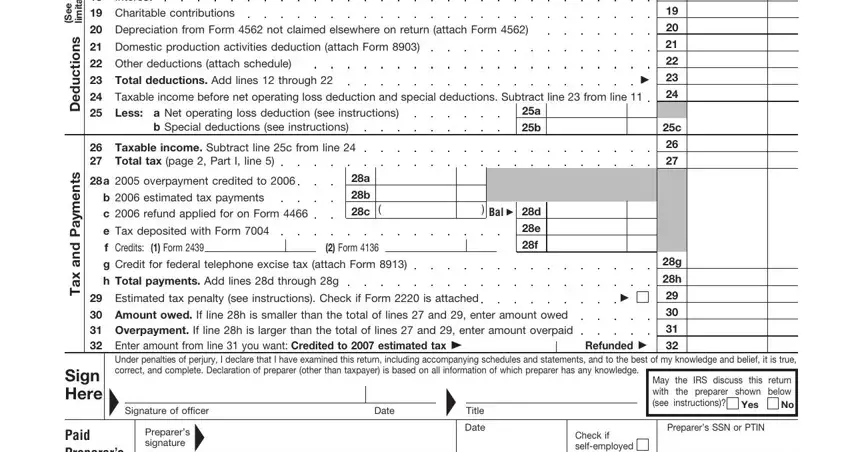

Complete Part I by entering gross receipts (before returns and allowances), cost of goods sold, dividends, interest, rents, and other income. Then complete Part II with all applicable deductions. Enter officer compensation in the designated schedule. Total income minus total deductions equals taxable income before special deductions.

Step 4: Compute the Tax

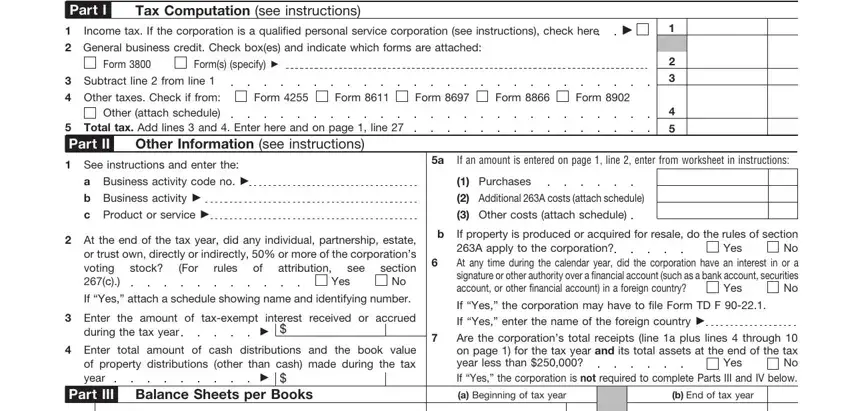

Part III applies the corporate income tax rate to taxable income and calculates total tax due. Subtract any credits and prior estimated tax payments. The result is the balance due or overpayment. Corporations that overpaid may apply the credit to the next tax year or request a refund.

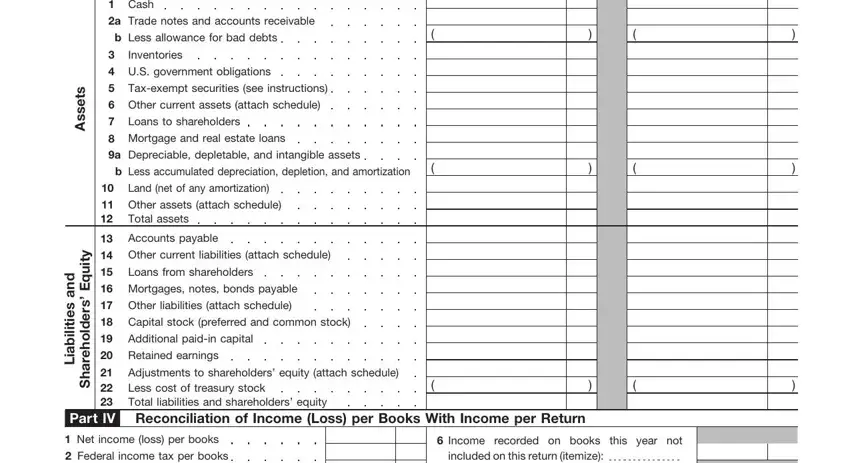

Step 5: Complete the Balance Sheet

Corporations with total assets of $25,000 or more must complete Part IV, the balance sheet per the books. Enter beginning-of-year and end-of-year figures for assets, liabilities, and shareholders' equity. Corporations below the $25,000 threshold may leave this section blank.

Step 6: Review and Download

Review the completed form for accuracy. Confirm all figures match your corporate records and that officer compensation is fully reported. Click "Done" to finalize, then download the PDF. Sign up for a free 7-day FormsPal trial to save and retrieve your completed forms at any time.

Common Mistakes When Filing Form 1120-A

- Incorrect EIN. The employer identification number must exactly match IRS records to avoid processing delays.

- Missing officer compensation schedule. All officers who received salary during the year must be reported in Schedule E.

- Skipping the balance sheet. Corporations with total assets at or above $25,000 must complete Part IV.

- Misreporting gross receipts. Gross receipts must be entered before returns and allowances, which are subtracted on a separate line.

- Filing when ineligible. Corporations that did not meet all eligibility criteria were required to file Form 1120, not Form 1120-A.

Frequently Asked Questions About Form 1120-A

Is Form 1120-A still accepted by the IRS?

No. The IRS discontinued Form 1120-A after the 2006 tax year. All C corporations filing for 2007 and later must use Form 1120. The 2006 version is available here for reference or amended return purposes.

What replaced Form 1120-A?

Form 1120 replaced Form 1120-A for all C corporations starting with the 2007 tax year. The full Form 1120 is longer and includes additional schedules, but it accepts filings from corporations of any size.

Can I amend a previously filed Form 1120-A?

Yes. To correct a previously filed Form 1120-A for the 2006 tax year, file the original form with Form 1120-X, the Amended U.S. Corporation Income Tax Return, to report the correction.

What was the penalty for filing Form 1120-A late?

For tax year 2006, the IRS charged a failure-to-file penalty of 5% of unpaid tax per month, up to 25%. A minimum penalty applied when the return was more than 60 days late. Filing Form 7004 for an extension before the deadline avoided this penalty if tax owed was paid on time.