You are able to complete form 730 effectively with our online PDF tool. FormsPal professional team is ceaselessly endeavoring to improve the tool and help it become much easier for clients with its multiple features. Enjoy an ever-improving experience now! By taking several easy steps, you can begin your PDF journey:

Step 1: Just press the "Get Form Button" at the top of this page to launch our pdf editing tool. Here you will find all that is needed to work with your document.

Step 2: With this handy PDF file editor, you could do more than simply fill in forms. Edit away and make your forms look faultless with custom textual content added in, or adjust the original input to perfection - all supported by the capability to insert almost any graphics and sign the file off.

Pay attention while filling out this form. Make sure every blank is filled in properly.

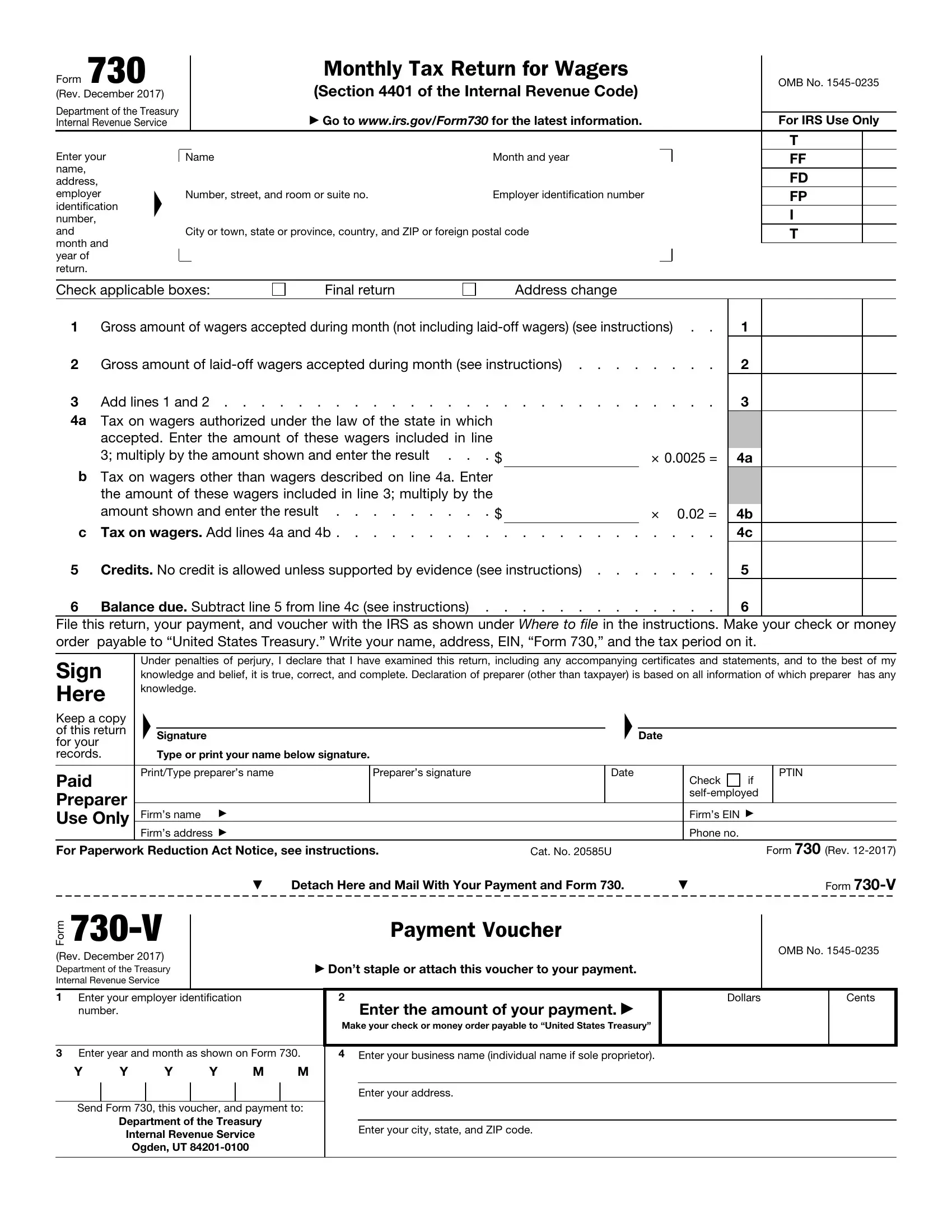

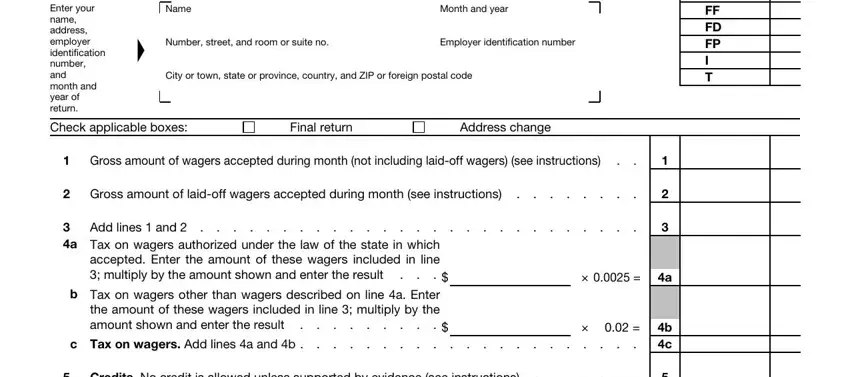

1. It is advisable to fill out the form 730 properly, hence pay close attention while filling in the parts including all these blank fields:

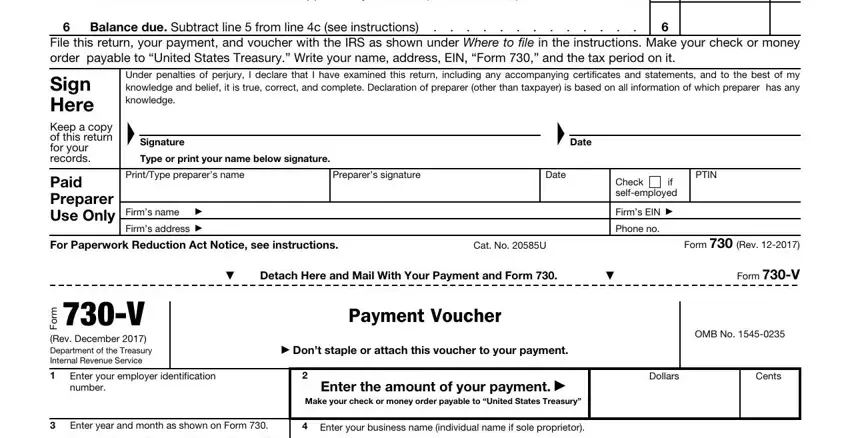

2. Once your current task is complete, take the next step – fill out all of these fields - Credits No credit is allowed, Balance due Subtract line from, File this return your payment and, Sign Here Keep a copy of this, Paid Preparer Use Only, Under penalties of perjury I, Signature, Date, Type or print your name below, PrintType preparers name, Preparers signature, Date, Firms name , Firms address , and PTIN with their corresponding information. Make sure to double check that everything has been entered correctly before continuing!

Regarding Balance due Subtract line from and Date, make sure that you double-check them in this section. The two of these are the most important ones in this document.

3. This step is normally hassle-free - fill out all the blanks in Send Form this voucher and, Department of the Treasury, Internal Revenue Service, Ogden UT , Enter your address, and Enter your city state and ZIP code in order to complete the current step.

Step 3: Reread the information you've entered into the blanks and then click the "Done" button. Obtain your form 730 when you register online for a 7-day free trial. Quickly get access to the pdf in your personal account page, together with any edits and adjustments conveniently preserved! FormsPal is invested in the personal privacy of all our users; we always make sure that all personal information used in our tool is kept confidential.