Completing the Arizona Tax Return Form online is quick and easy with the FormsPal PDF tool. Follow the steps below to fill out and save your Arizona Form A1-QRT at no cost.

Step 1: Press the "Get Form" button at the top of this page to open the PDF editor.

Step 2: Once the tool opens, the form is ready to fill out. You can enter text in blank fields, modify existing text, add images, sign the document, and more.

You will need to provide specific information for each part of the form. Take your time to enter the correct details in every required field:

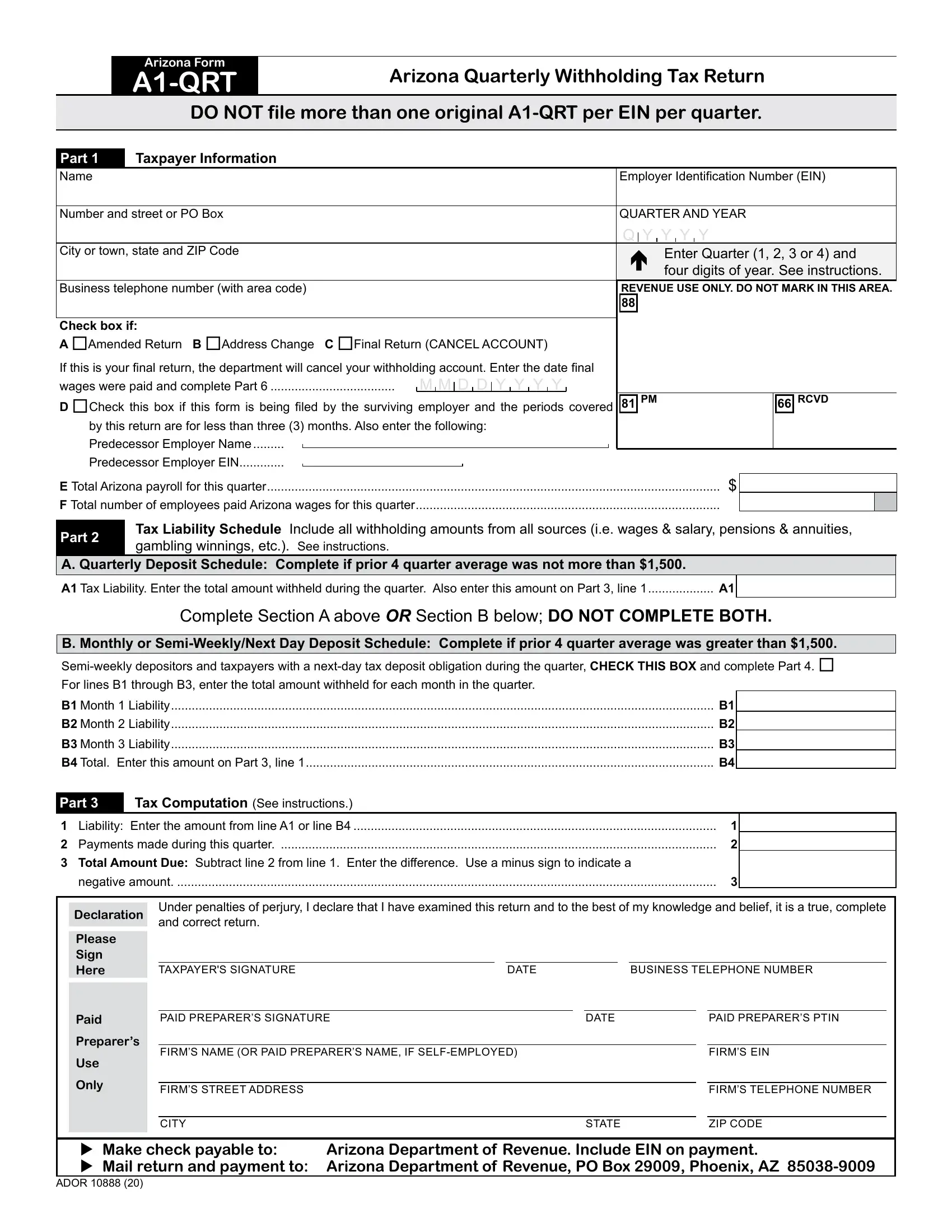

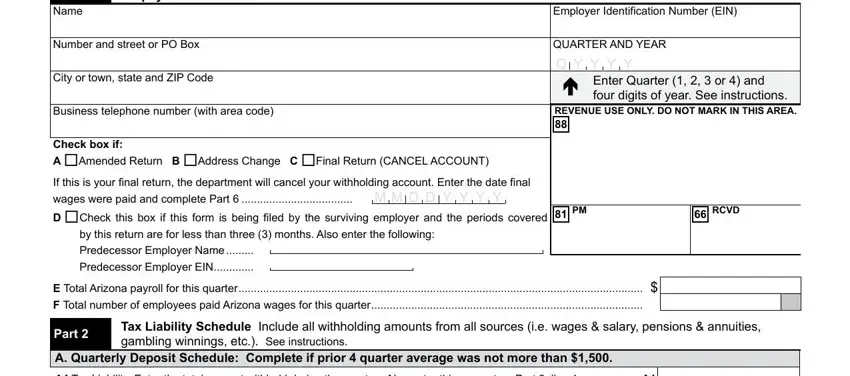

1. Begin filling in the Arizona Tax Return Form by completing the fields on the first page:

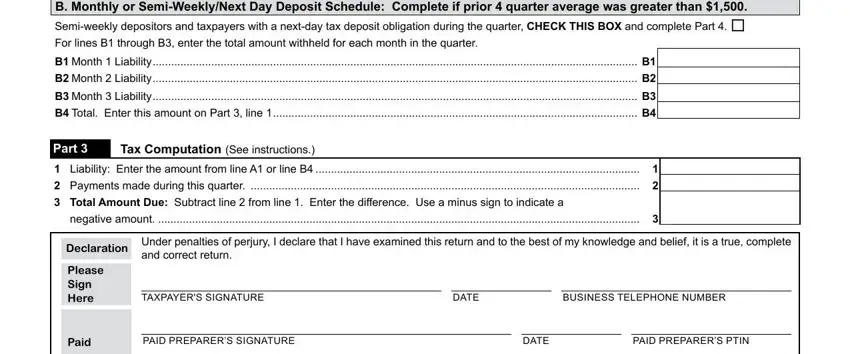

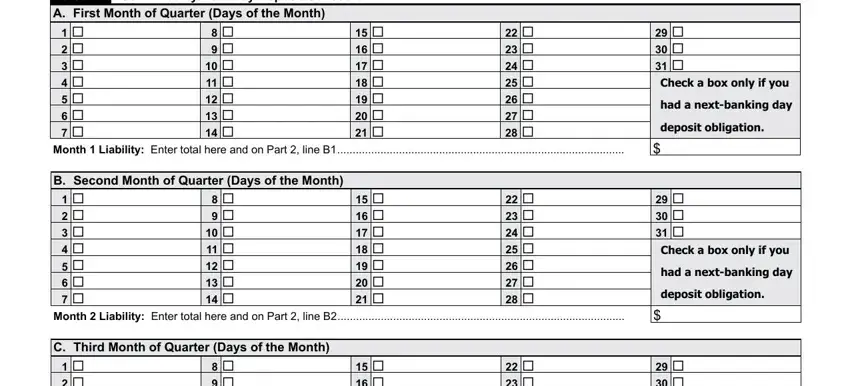

2. Next, enter the required details in the monthly or semi-weekly deposit schedule section, including monthly liability amounts for each month of the quarter, total liability, tax computation figures, and the declaration and signature fields.

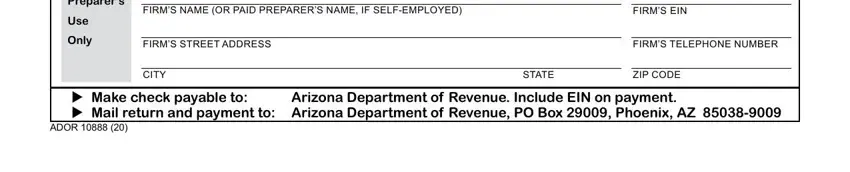

3. Complete the preparer fields if a paid preparer is filing on your behalf. Enter the firm name, EIN, street address, telephone number, city, state, and ZIP code. Make checks payable to the Arizona Department of Revenue.

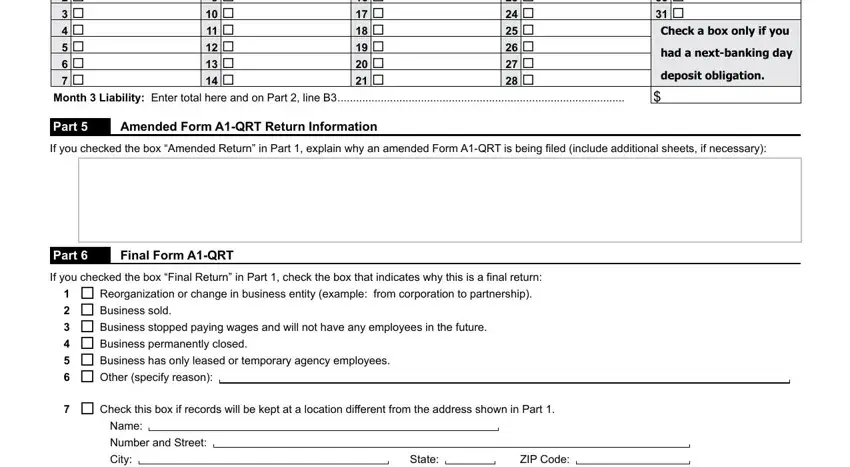

4. Part A covers the first month of the quarter. Part B covers the second month. Part C covers the third month. For each month, enter the total tax liability. If you had a next-banking-day deposit obligation, check the appropriate box.

5. The final section handles amended or final returns. Check the Amended Return box if you are correcting a prior filing. Check the Final Return box if you are ceasing business or no longer have withholding obligations. Complete the name and address fields in this section before submitting.

Step 3: After reviewing all your entries, click "Done" to finish. Create a free trial account to download your completed Arizona Tax Return Form or send it by email. Your document will be saved in your account for future access.

Frequently Asked Questions About Arizona Form A1-QRT

Who must file Arizona Form A1-QRT?

Any Arizona employer who withholds state income tax from employee wages must file Form A1-QRT each quarter. Employers who are approved by the Arizona Department of Revenue to remit on an annual basis are exempt from quarterly filing.

When is the Arizona A1-QRT form due?

The form is due by the last day of the month following each calendar quarter. The Q1 return (January through March) is due April 30. The Q2 return (April through June) is due July 31. The Q3 return (July through September) is due October 31. The Q4 return (October through December) is due January 31.

Can I file an amended Arizona Form A1-QRT?

Yes. To amend a previously filed A1-QRT, check the Amended Return box in the applicable section and provide corrected figures. Include a brief explanation of what was changed and why.

Do I need to file if I had no withholding activity for the quarter?

Arizona employers who are registered to withhold are still required to file even if no wages were paid during the quarter. File a zero return to remain in good standing with the Arizona Department of Revenue.

For related withholding and payroll forms, see the Income Withholding Form, the Earnings Withholding Order Form, and the Payroll Check Template.