You can fill in BIR Form 1801 effortlessly in our online tool for PDF editing. The editor is continually improved by our staff, acquiring new features and turning out to be better. Getting underway is effortless. All you need to do is follow these easy steps directly below:

Step 1: Open the Estate Tax Return Editor

Click the "Get Form Button" above on this page to access our form editor. This way, you will find all that is necessary to fill out your Estate Tax Return file.

Step 2: Review and Begin Filling In the Form

Once you launch the tool, the form will be ready to fill in. Apart from filling out various fields, you may also perform other actions with the form, such as writing your own text, changing the initial text, inserting images, signing the PDF, and much more.

How to Fill In Each Section

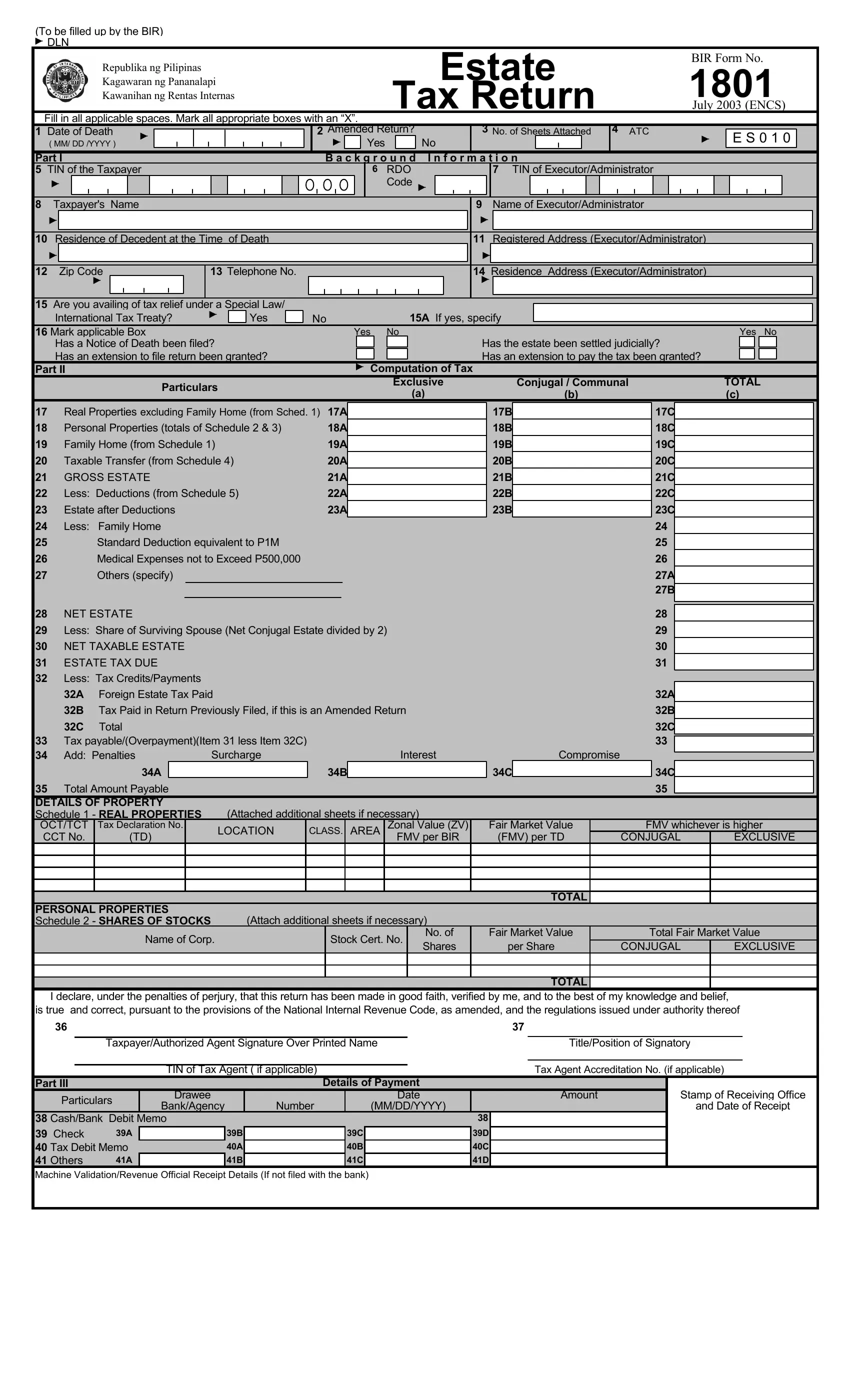

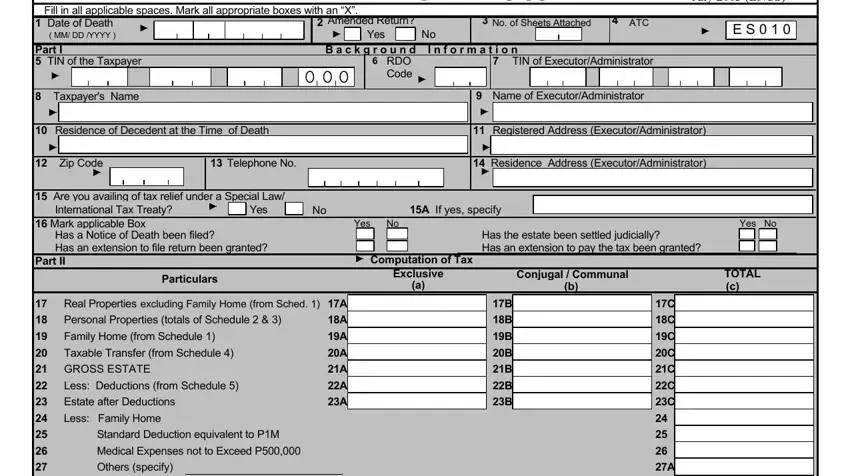

While filling out BIR Form 1801, ensure you complete all necessary blanks in their relevant area. This will help hasten the work, which allows your details to be handled promptly and accurately.

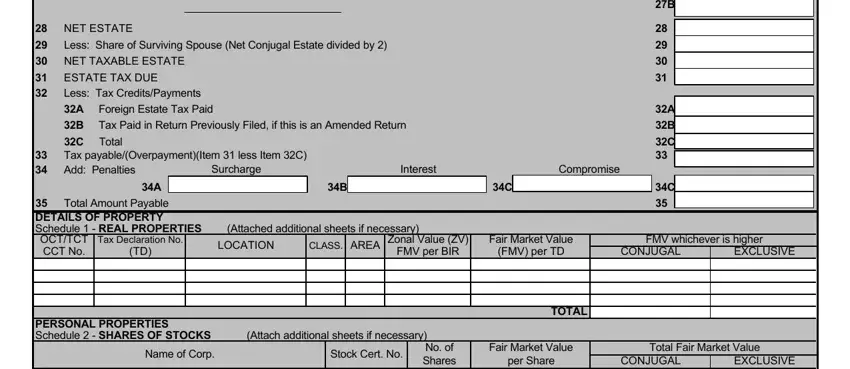

Once the first section is complete, fill in these fields: NET ESTATE, Less Share of Surviving Spouse, NET TAXABLE ESTATE, ESTATE TAX DUE, Less Tax Credits/Payments, A Foreign Estate Tax Paid, B Tax Paid in Return Previously, C Total, Tax Payable/Overpayment, Surcharge, Interest, Compromise, Total Amount Payable, and Tax Declaration No. Double check all entries before continuing.

Take care when filling out Tax Declaration No, as errors in this field are common. Review it carefully before submitting.

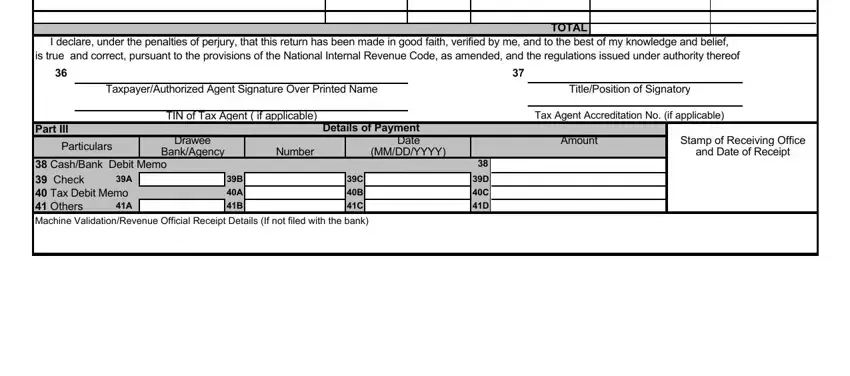

The following section covers: I declare under the penalties of, Taxpayer/Authorized Agent Signature, Title/Position of Signatory, TOTAL, TIN of Tax Agent if applicable, Tax Agent Accreditation No, Part III, Particulars, Drawee, Bank/Agency, Details of Payment Date, Number, MMDDYYYY, Cash/Bank Debit Memo, and Check/Tax Debit Memo. Complete every empty form field in this section.

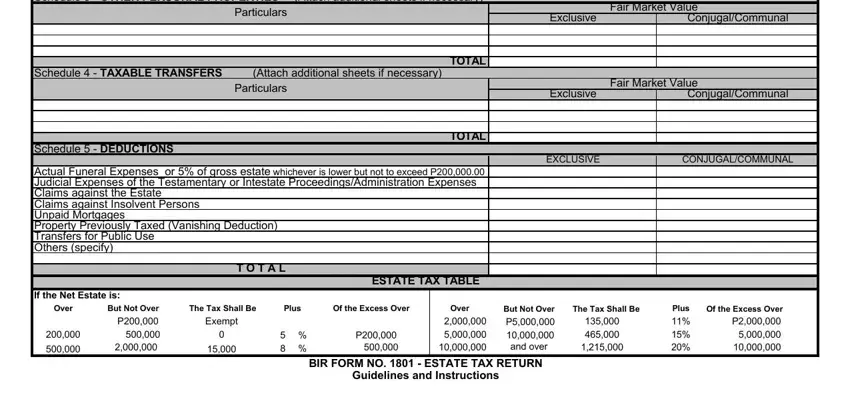

This next section requires additional information. Complete all the necessary fields: Schedule OTHER PERSONAL, Particulars, Fair Market Value, Exclusive, Conjugal/Communal, Schedule TAXABLE TRANSFERS, TOTAL, Schedule DEDUCTIONS, Actual Funeral Expenses, TOTAL, and ESTATE TAX TABLE.

Step 3: Save and Download Your Completed Return

After proofreading your filled blanks, click "Done" and you are good to go. Join FormsPal today and easily get access to this form, available for downloading. All alterations are saved, letting you change the document at a later stage if required. FormsPal offers secure form tools with no personal information recording or any type of sharing. Be assured that your information is safe with us.

Frequently Asked Questions About the BIR Estate Tax Return

What is the estate tax rate for BIR Form 1801?

Under the TRAIN Law effective January 2018, the estate tax rate is a flat 6% on the net taxable estate. There is no longer a graduated rate schedule for Philippine estate tax.

Who is required to file the estate tax return?

Executors, administrators, or legal heirs are required to file when the gross estate exceeds PHP 200,000 or when it includes registrable properties such as real estate or motor vehicles.

What is the deadline for filing?

The estate tax return must be filed and the tax paid within one year from the date of the decedent's death. The BIR may grant extensions of up to 30 days in meritorious cases.

What other BIR forms may be required alongside Form 1801?

Depending on the estate's income and business interests, you may also need the BIR Form 1701 Annual Income Tax Return, the BIR Form 1701Q Quarterly Income Tax Return, or the BIR Form 1601-E Expanded Withholding Tax Return.