CE Form 1 (Statement of Financial Interests) can be filled out online quickly with FormsPal. Our PDF editor is easy to use and continuously updated based on user feedback. Follow these steps to get started:

Step 1: Click the "Get Form" button at the top of this page to open CE Form 1 in the FormsPal PDF editor.

Step 2: The editor lets you customize the PDF in multiple ways. Add text in any field, adjust existing entries, and insert your signature. All options are available in one tool.

This form requires specific financial information. Review the tips below to fill it out accurately:

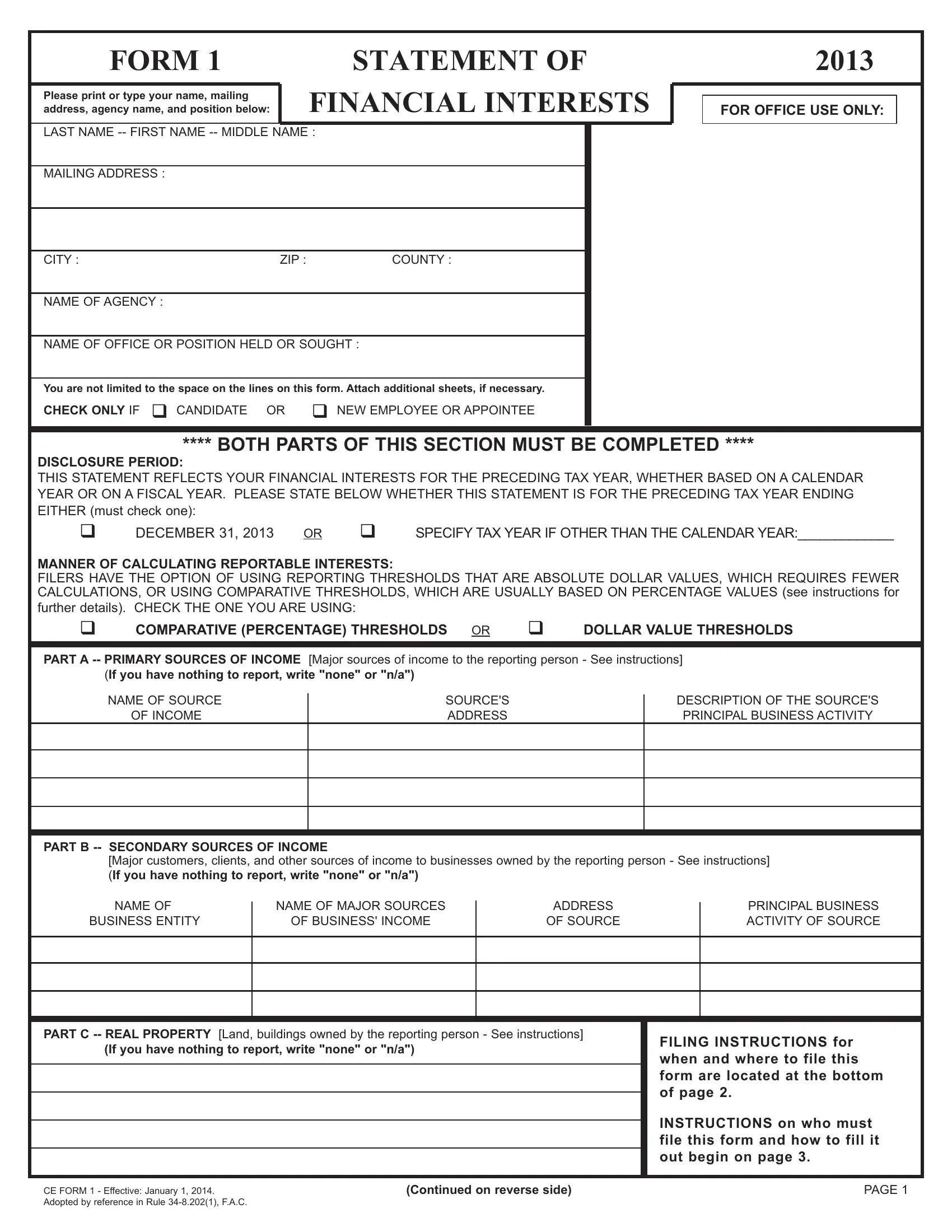

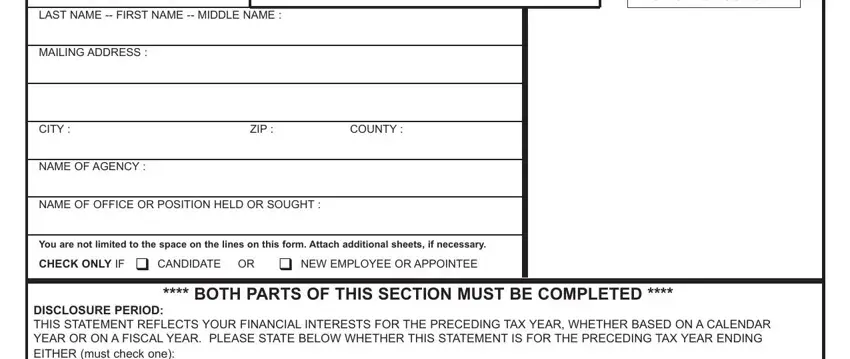

1. Begin with the disclosure period section, which includes the following fields:

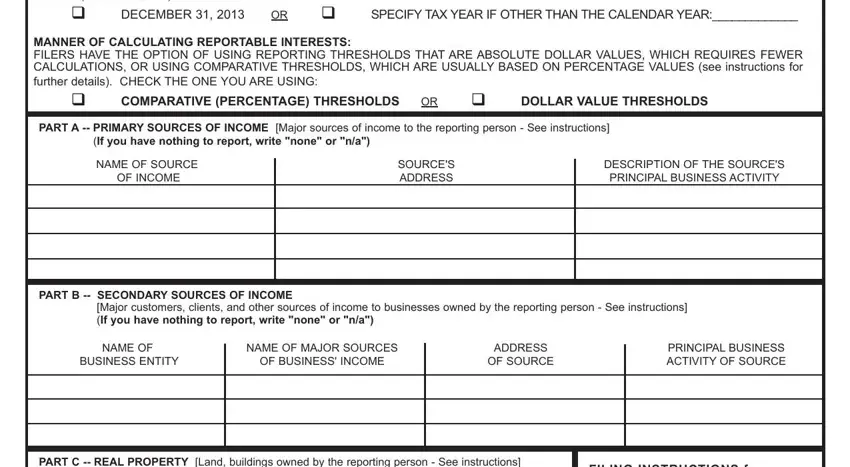

2. Complete all blank fields in this section: DISCLOSURE PERIOD, MANNER OF CALCULATING REPORTABLE, PART A - PRIMARY SOURCES OF INCOME, NAME OF SOURCE OF INCOME, SOURCES ADDRESS, DESCRIPTION OF THE SOURCES, PRINCIPAL BUSINESS ACTIVITY, PART B - SECONDARY SOURCES OF INCOME, Major customers and clients, NAME OF BUSINESS ENTITY, and NAME OF MAJOR SOURCES.

3. This section covers PART C - REAL PROPERTY, FILING INSTRUCTIONS for when and who must file, INSTRUCTIONS on who must file this form, CE FORM 1 Effective January, and Continued on reverse side. Complete each field carefully.

Many filers make errors in the INSTRUCTIONS section. Review all entries in this area before proceeding.

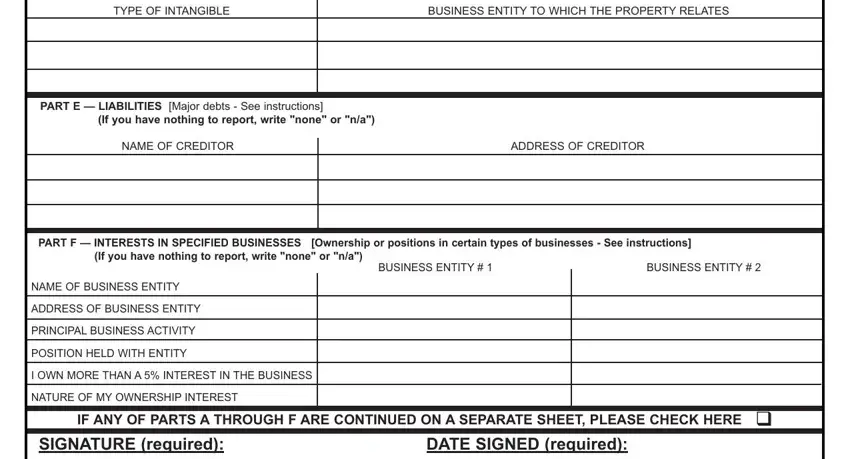

4. The final section requires additional details for: TYPE OF INTANGIBLE ASSET, BUSINESS ENTITY information, PART E - LIABILITIES, NAME OF CREDITOR, ADDRESS OF CREDITOR, PART F - INTERESTS IN SPECIFIED BUSINESS ENTITY, POSITION HELD WITH ENTITY, I OWN MORE THAN A 5% INTEREST IN THE ENTITY, and NATURE OF MY OWNERSHIP INTEREST. Fill in all applicable fields to complete your disclosure.

Step 3: Review all your entries and click "Done" to finalize the form. Download the completed CE Form 1 or return to edit it later. FormsPal keeps your data secure and private throughout the process.

Frequently Asked Questions About CE Form 1

Who is required to file CE Form 1?

CE Form 1 must be filed by local officers, specified state employees, state officers, and candidates running for positions that require Form 1 filers under Section 112.3145, Florida Statutes. This includes city and county officials, school board members, and many other local government positions.

When is CE Form 1 due?

The annual filing deadline is July 1 each year. New filers must submit their initial Form 1 within 30 days of starting a qualifying position. Late filing may result in civil penalties.

Where do I submit CE Form 1?

Local officers submit their completed form to their county Supervisor of Elections. State officers and specified state employees file with the Florida Commission on Ethics. All filers since the 2023 form year must use the Electronic Financial Disclosure Management System (EFDMS) for electronic submission.

What financial information does CE Form 1 require?

You must disclose primary and secondary income sources, intangible assets (stocks, bonds, investments), real property, liabilities over the reporting threshold, and any interests in specified businesses related to your public duties.

What is the penalty for not filing CE Form 1 on time?

Failure to file CE Form 1 by the July 1 deadline may result in civil penalties. The Florida Commission on Ethics may assess a fine of up to $25 per day for late filing, with a maximum penalty of $1,500 per violation.

For related Florida disclosure and financial forms, see also: Statement of Financial Interest, Florida Financial Affidavit, and ACT 221 Disclosure Form.