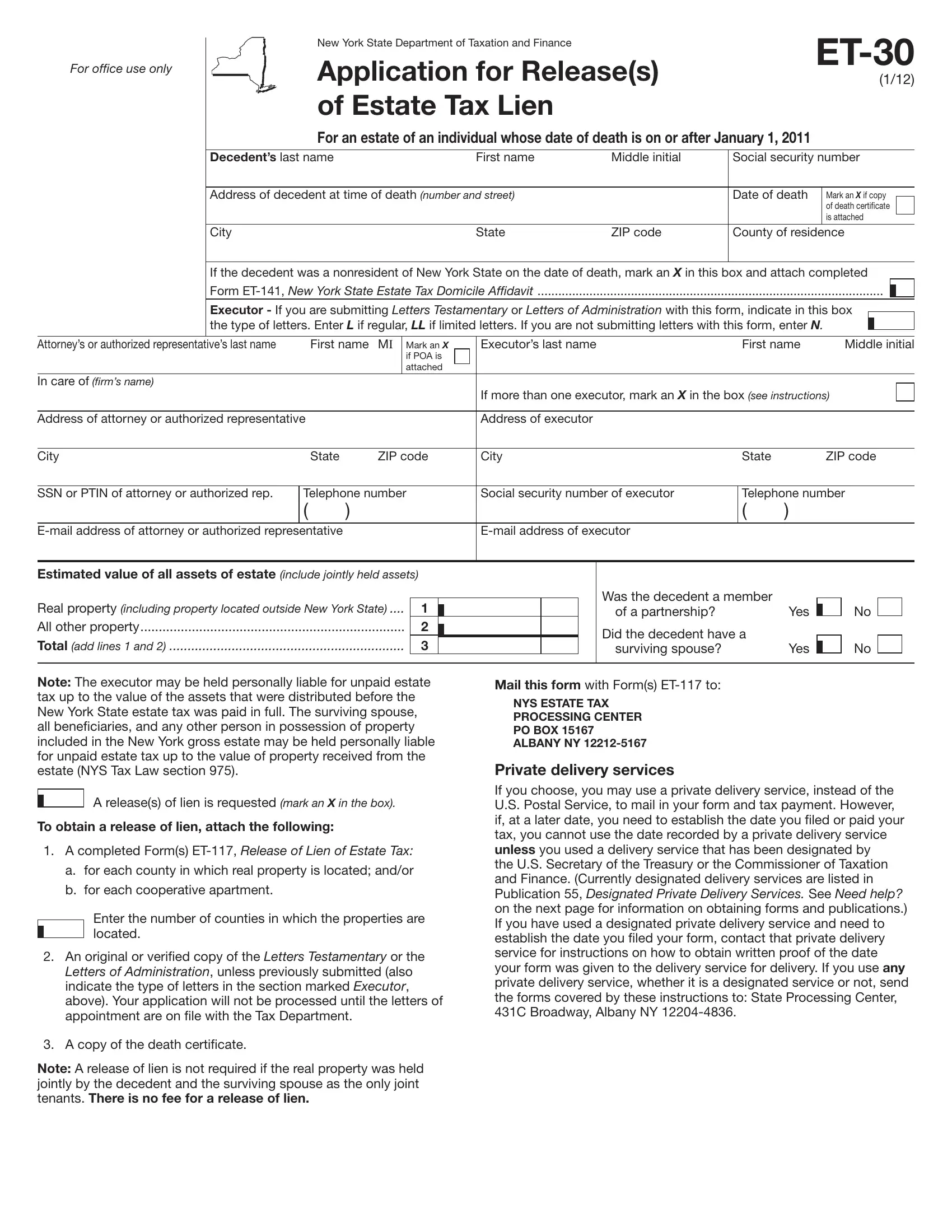

In the world of estate management and taxation in New York State, navigating through the procedures following the demise of a loved one can be intricate. One of the pivotal steps involves the ET-30 form, issued by the New York State Department of Taxation and Finance, which serves as an application for Release(s) of Estate Tax Lien for estates of individuals who have passed away on or after January 1, 2011. This form becomes crucial for executors or administrators tasked with managing the decedent's estate, ensuring that property can be transferred without the hindrance of a tax lien. It requests detailed information about the decedent, including their last name, social security number, and date of death, plus specifics about the estate's value and the existence of a surviving spouse or jointly held assets. Also, the form outlines the necessary attachments required for processing, such as the death certificate and Letters Testamentary or Letters of Administration, ensuring the executor's legal authority to act on behalf of the estate. Furthermore, the ET-30 form highlights different scenarios, depending on whether the estate involves properties within New York State for residents or non-residents, detailed instructions on obtaining a release of lien, and guidance on when to use alternate forms like the ET-706 or ET-85 for varying estate tax filing requirements. Navigating this form accurately is essential for executors to fulfill their duties, release estate tax liens, and distribute assets in accordance with the law, making understanding its specifications and requirements paramount for a smooth probate process.

| Question | Answer |

|---|---|

| Form Name | Et 30 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | et 30, form et 30 fillable application for release, fillable form et 30, et form |

|

|

|

New York State Department of Taxation and Finance |

|

|

|

|

|||||||||||||

For office use only |

|

|

Application for Release(s) |

|

|

|

||||||||||||||

|

|

|

|

|

(1/12) |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

of Estate Tax Lien |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

For an estate of an individual whose date of death is on or after January 1, 2011 |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Decedent’s last name |

|

|

|

|

First name |

Middle initial |

Social security number |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Address of decedent at time of death (number and street) |

|

Date of death |

Mark an X if copy |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

of death certiicate |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

is attached |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

|

State |

ZIP code |

County of residence |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

If the decedent was a nonresident of New York State on the date of death, mark an X in this box and attach completed |

|||||||||||||||||||

|

Form ET‑141, New York State Estate Tax Domicile Affidavit |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Executor - If you are submitting Letters Testamentary or Letters of Administration with this form, indicate in this box |

|

|

|

|

|||||||||||||||

|

the type of letters. Enter L if regular, LL if limited letters. If you are not submitting letters with this form, enter N. |

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attorney’s or authorized representative’s last name |

|

First name |

MI |

Mark an X |

Executor’s last name |

|

|

First name |

|

Middle initial |

||||||||||

|

|

|

|

|

if POA is |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

attached |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

In care of (firm’s name) |

|

|

|

|

|

|

If more than one executor, mark an X in the box (see instructions) |

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of attorney or authorized representative |

|

|

|

|

|

Address of executor |

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

ZIP code |

City |

|

|

State |

|

ZIP code |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SSN or PTIN of attorney or authorized rep. |

Telephone number |

Social security number of executor |

|

Telephone number |

||||||||||||||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E‑mail address of attorney or authorized representative |

|

|

|

|

E‑mail address of executor |

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Estimated value of all assets of estate (include jointly held assets) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Real property (including property located outside New York State) |

|

|

|

|

|

|

Was the decedent a member |

|

|

|

|

|

|

|

||||||

1 |

|

|

|

|

of a partnership? |

|

|

Yes |

|

No |

|

|

|

|||||||

All other property |

|

|

|

|

2 |

|

|

|

|

Did the decedent have a |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

................................................................Total (add lines 1 and 2) |

|

|

|

|

3 |

|

|

|

|

surviving spouse? |

|

|

Yes |

|

No |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: The executor may be held personally liable for unpaid estate tax up to the value of the assets that were distributed before the New York State estate tax was paid in full. The surviving spouse, all beneiciaries, and any other person in possession of property included in the New York gross estate may be held personally liable for unpaid estate tax up to the value of property received from the estate (NYS Tax Law section 975).

A release(s) of lien is requested (mark an X in the box).

To obtain a release of lien, attach the following:

1.A completed Form(s) ET‑117, Release of Lien of Estate Tax:

a.for each county in which real property is located; and/or

b.for each cooperative apartment.

Enter the number of counties in which the properties are located.

2.An original or veriied copy of the Letters Testamentary or the Letters of Administration, unless previously submitted (also indicate the type of letters in the section marked Executor, above). Your application will not be processed until the letters of appointment are on ile with the Tax Department.

3.A copy of the death certiicate.

Note: A release of lien is not required if the real property was held jointly by the decedent and the surviving spouse as the only joint tenants. There is no fee for a release of lien.

Mail this form with Form(s) ET‑117 to:

NYS ESTATE TAX

PROCESSING CENTER

PO BOX 15167

ALBANY NY

Private delivery services

If you choose, you may use a private delivery service, instead of the U.S. Postal Service, to mail in your form and tax payment. However, if, at a later date, you need to establish the date you iled or paid your tax, you cannot use the date recorded by a private delivery service unless you used a delivery service that has been designated by

the U.S. Secretary of the Treasury or the Commissioner of Taxation and Finance. (Currently designated delivery services are listed in Publication 55, Designated Private Delivery Services. See Need help? on the next page for information on obtaining forms and publications.) If you have used a designated private delivery service and need to establish the date you iled your form, contact that private delivery service for instructions on how to obtain written proof of the date your form was given to the delivery service for delivery. If you use any private delivery service, whether it is a designated service or not, send the forms covered by these instructions to: State Processing Center, 431C Broadway, Albany NY 12204‑4836.

Instructions

When to use Form

Use this form to obtain release(s) of an estate tax lien if you are the appointed executor or administrator of the estate, or the duly authorized representative of the executor, and fewer than nine months have passed since the date of death.

Note: Waivers are not required for the estate of an individual whose date of death is on or after February 1, 2000. However, the need to obtain a release of the estate tax lien before transferring real property remains.

Submit either Letters Testamentary or Letters of Administration with the application as proof of your appointment, unless previously submitted. To be acceptable, the letters of appointment must be current and must not restrict the executor from receiving estate assets.

Letters of appointment issued by a court outside New York State are acceptable if the decedent was not a resident of New York State at the time of death, and the court has jurisdiction over the decedent’s estate.

Enter the executor’s name, address, social security number, and telephone number in the area provided. If the estate has more than one executor, enter the information for any executor (preferably one who is a New York State resident) in the area provided, mark an X in the box, and attach a list of the other executors with their addresses, telephone numbers, and social security numbers.

When to use forms other than Form

Use Form ET‑706, New York State Estate Tax Return, when the estate is required to ile a New York State estate tax return, and either:

1.The estate has not obtained an extension of time to ile the estate tax return, and more than nine months have passed since the date of death; or

2.The estate obtained an extension of time to ile the estate tax return, and more than 15 months have passed since the date of death (the extension has expired).

Use Form ET‑85, New York State Estate Tax Certification, if either of the following applies:

1.The estate is not required to ile a New York State estate tax return, and either:

a.no executor or administrator has been appointed, or

b.more than nine months have passed since the date of death.

2.The estate is required to ile a New York State estate tax return, and either:

a.fewer than nine months have passed since the date of death, and an executor or administrator has not been appointed; or

b.more than nine but less than 15 months have passed since the date of death, and an extension of time to ile the estate tax return has been granted.

If the estate is subject to tax, an estimated payment may be required when Form ET‑85 is iled.

The term executor includes executrix, administrator, administratrix, or personal representative of the decedent’s estate; if no executor is appointed, qualiied, and acting within the United States, executor means any person in actual or constructive possession of any property of the decedent with suficient knowledge to ile an accurate return.

This person may ile Form ET‑85 or Form ET‑706 to obtain a release of lien, and must assume personal liability for all estate taxes that may be due.

If the executor has signed Form ET‑14, Estate Tax Power of Attorney, and it is being submitted with this application, attach it to the application and mark an X in the box.

Complete and attach Form ET‑117, Release of Lien of Estate Tax, if a release of lien is needed for real property or a cooperative apartment. Two parcels of real estate can be listed on one form. However, if the real property is located in different counties or a release of lien is needed for more than one cooperative apartment, a separate Form ET‑117 must be completed for each county or apartment. The name and address of the executor, or authorized representative, should be entered at the top of Form ET‑117 for mailing purposes.

Which estates must file a New York State estate tax return

An estate of an individual who was either a resident or citizen of the United States at the time of death must ile Form ET‑706 if the gross estate, plus federal adjusted taxable gifts and speciic exemption, exceeds $1,000,000, and either the decedent was a resident of New York State at the time of death, or the estate includes real or tangible personal property having an actual situs in New York State.

An estate of an individual who was a nonresident of the United States and not a U.S. citizen at the time of death must ile Form ET‑706 if the estate is required to ile a federal estate tax return and the estate includes real or tangible personal property having an actual situs in New York State.

Privacy notification — The Commissioner of Taxation and Finance may collect and maintain personal information pursuant to the New York State Tax Law, including but not limited to, sections 5‑a, 171, 171‑a, 287, 308, 429, 475, 505, 697, 1096, 1142, and 1415 of that Law; and may require disclosure of social security numbers pursuant to 42 USC 405(c)(2)(C)(i).

This information will be used to determine and administer tax liabilities and, when authorized by law, for certain tax offset and exchange of tax information programs as well as for any other lawful purpose.

Information concerning quarterly wages paid to employees is provided to certain state agencies for purposes of fraud prevention, support enforcement, evaluation of the effectiveness of certain employment and training programs and other purposes authorized by law.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Manager of Document Management, NYS Tax Department, W A Harriman Campus, Albany NY 12227; telephone (518) 457‑5181.

Need help?

Visit our Web site at www.tax.ny.gov

•get information and manage your taxes online

•check for new online services and features

Telephone assistance |

|

Estate Tax Information Center: |

(518) |

To order forms and publications: |

(518) |

Specific instructions

Complete the information requested about the decedent. Please verify that the decedent’s social security number is correctly entered on the application. Submit a photocopy of the death certiicate with the application.

For the estate of an individual who was not a resident of New York State at the time of his or her death, complete Form ET‑141, New York State Estate Tax Domicile Affidavit, and attach it to the return.

If a person is authorized to represent the executor regarding the estate, and the executor prefers the department contact that person, enter the name (last name irst) of the attorney, accountant, or enrolled agent representing the executor. Also enter the irm’s name, address, and telephone number in the areas provided.

Text Telephone (TTY) Hotline (for persons with hearing and speech disabilities using a TTY): If you have access to a TTY, contact us at

(518)

Persons with disabilities: In compliance with the

Americans with Disabilities Act, we will ensure that our lobbies, ofices, meeting rooms, and

other facilities are accessible to persons with

disabilities. If you have questions about special accommodations for persons with disabilities, call the information center.