In Massachusetts, there are a few specific forms that are required to be filed in order to start or continue proceedings in District Court. One such form is Form 1 309, also known as the "Complaint." This document is used to initiate a civil lawsuit by providing the basic facts of the case. The complaint must state the names of all parties involved, the damages being sought, and other important information. Filing a complaint is an important step in any legal proceeding, and it's important to make sure it is done correctly. If you have any questions about filing a complaint or need help completing this form, please contact an experienced attorney for assistance.

| Question | Answer |

|---|---|

| Form Name | Form 1 309 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | NONRESIDENT, certifies, successors, sc 1 309 form |

|

|

|

|

|

|

|

|

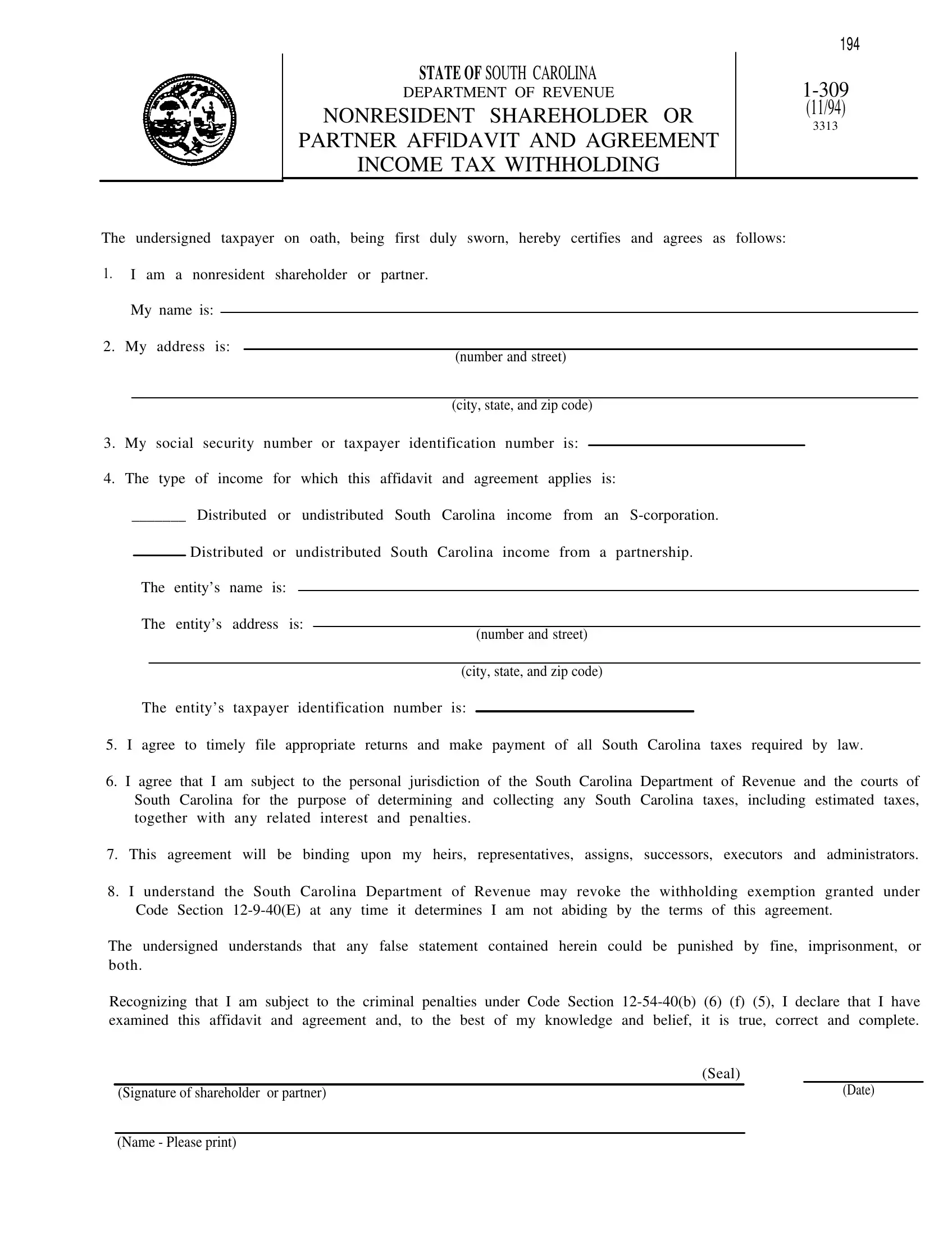

194 |

|

|

|

|

|

STATE OF SOUTH CAROLINA |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

DEPARTMENT OF REVENUE |

|

|

|

|

|

|

|

|

NONRESIDENT SHAREHOLDER OR |

|

(11/94) |

|

|

|

|

|

|

|

3313 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PARTNER AFFlDAVIT AND AGREEMENT |

|

|

|

|

|

|

|

|

INCOME TAX WITHHOLDING |

|

|

|

The undersigned |

|

taxpayer on oath, being first duly sworn, hereby certifies and |

agrees as follows: |

|

||||

1. |

I am a nonresident shareholder or partner. |

|

|

|

||||

|

My name is: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

My address |

is: |

|

|

|

|

||

|

|

|

|

|||||

|

|

|

|

|

(number and street) |

|

|

|

(city, state, and zip code)

3.My social security number or taxpayer identification number is:

4.The type of income for which this affidavit and agreement applies is:

_______ Distributed or undistributed South Carolina income from an

Distributed or undistributed South Carolina income from a partnership.

The entity’s name is:

The entity’s address is:

(number and street)

(city, state, and zip code)

The entity’s taxpayer identification number is:

5. I agree to timely file appropriate returns and make payment of all South Carolina taxes required by law.

6.I agree that I am subject to the personal jurisdiction of the South Carolina Department of Revenue and the courts of South Carolina for the purpose of determining and collecting any South Carolina taxes, including estimated taxes, together with any related interest and penalties.

7. This agreement will be binding upon my heirs, representatives, assigns, successors, executors and administrators.

8.I understand the South Carolina Department of Revenue may revoke the withholding exemption granted under Code Section

The undersigned understands that any false statement contained herein could be punished by fine, imprisonment, or both.

Recognizing that I am subject to the criminal penalties under Code Section

|

(Seal) |

||

(Signature of shareholder or partner) |

|

|

(Date) |

(Name - Please print)

INSTRUCTIONS

NONRESIDENT SHAREHOLDER OR PARTNER AFFIDAVIT AND AGREEMENT

INCOME TAX WITHHOLDING

Requirement to Make Withholding Payments

Code Section

Purpose of Affidavit

The affidavit is used by a nonresident shareholder or partner to request an exemption from the withholding required pursuant to Code Section

Who May Execute this Affidavit

Any nonresident shareholder or partner having South Carolina income from an

Where and When to Execute this Affidavit

.

Shareholder or Partner Instructions:

A shareholder or partner should fully complete the affidavit and submit it directly to the

The affidavit is valid for all subsequent years and should not be resubmitted to the entity as long as (1) the shareholder’s or partner's nonresident status remains unchanged or (2) the withholding exemption is not revoked by the Department of Revenue.

The

Partnerships should attach the affidavits to South Carolina form 1065 (partnership Return of Income) or form 4868 (Request for Extension of Time to File South Carolina TaX Return) and file with the Department of Revenue on or before the fifteenth day of the fourth month following the close of the partnerships tax year.

Affidavits remain valid for subsequent tax years and should only be filed with the Department of Revenue in the first year that the shareholder or partner submits an agreement to the entity.