Understanding the intricacies of Form 26, known as the Running Account Bill, plays a pivotal role in the domain of contractual agreements and financial management within construction projects. Serving a dual purpose, this form facilitates both advance payments and payments for measured works, thereby ensuring a streamlined financial flow between contractors and project managers. Its design accommodates the detailing of executed work quantities, associated unit rates, and the resulting financial calculations, which are pivotal for maintaining transparency and accuracy in contractor payments. Noteworthy is the requirement for this document, particularly its final payments version, to be printed on yellow paper, a unique attribute that underscores its importance in the final settlement process. The form encapsulates a meticulous structure, divided into sections that cover accounts of work executed, certificates and signatures to validate the work, and a memorandum of payments that outlines advance payments, secured advances, and the actual payments to be made. This comprehensive approach ensures that all financial transactions are recorded meticulously, offering a safeguard against discrepancies and fostering trust between all involved parties. Moreover, the stipulation for the signing of certificates by designated officers adds an additional layer of verification, ensuring that the payments made or to be made are firmly rooted in the actual work completed, thus reinforcing accountability and precision in financial dealings.

| Question | Answer |

|---|---|

| Form Name | Form 26 |

| Form Length | 7 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 45 sec |

| Other names | secured advance form 26a cpwd pdf, secured advance form 26a cpwd, form number 26 is used for in civil engineering, running account bill form 26 pdf |

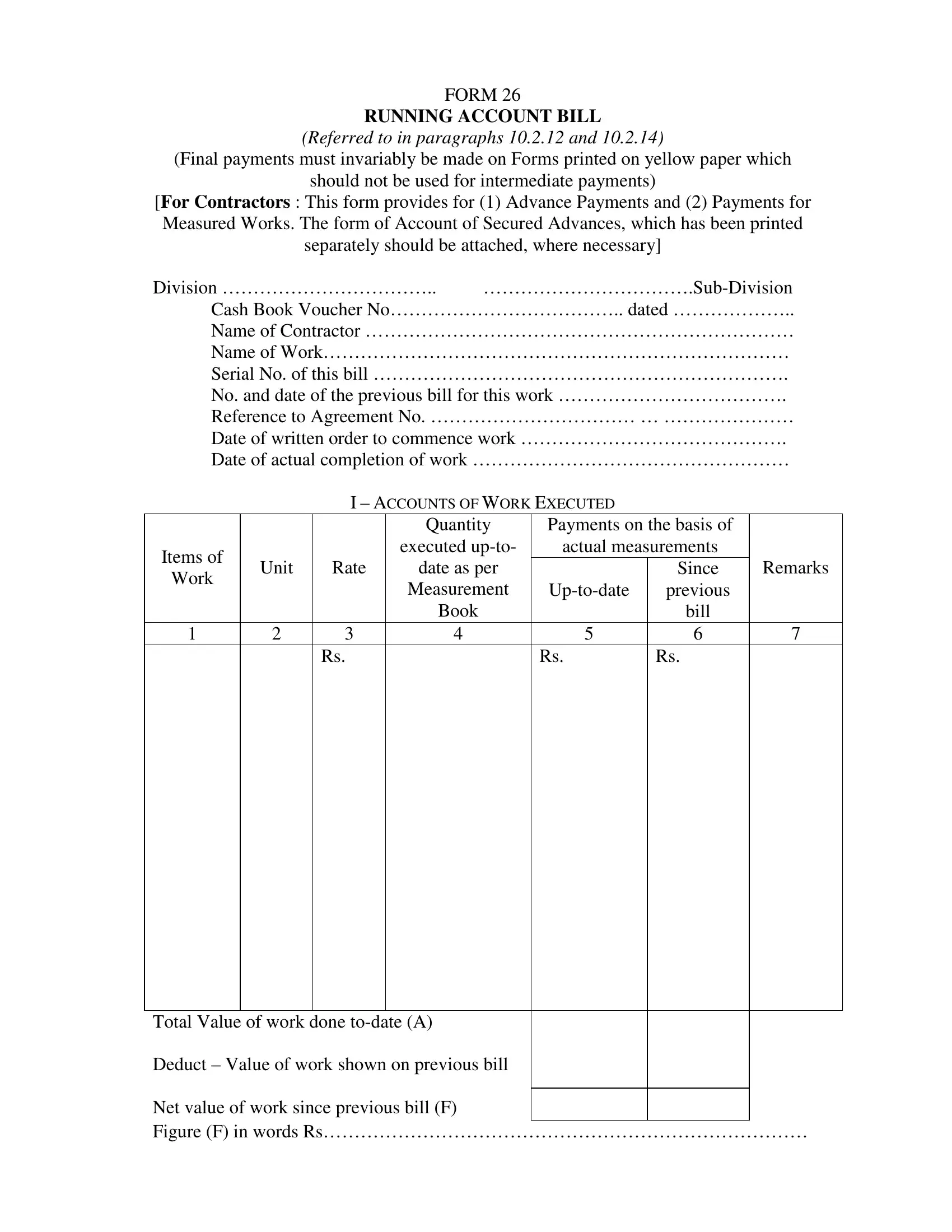

FORM 26

RUNNING ACCOUNT BILL

(Referred to in paragraphs 10.2.12 and 10.2.14)

(Final payments must invariably be made on Forms printed on yellow paper which

should not be used for intermediate payments)

[For Contractors : This form provides for (1) Advance Payments and (2) Payments for Measured Works. The form of Account of Secured Advances, which has been printed separately should be attached, where necessary]

Division ……………………………..

Cash Book Voucher No……………………………….. dated ………………..

Name of Contractor ……………………………………………………………

Name of Work…………………………………………………………………

Serial No. of this bill ………………………………………………………….

No. and date of the previous bill for this work ……………………………….

Reference to Agreement No. …………………………… … …………………

Date of written order to commence work …………………………………….

Date of actual completion of work ……………………………………………

|

|

I – ACCOUNTS OF WORK EXECUTED |

|

|

|

||

|

|

|

Quantity |

Payments on the basis of |

|

||

Items of |

|

|

executed |

actual measurements |

|

||

Unit |

Rate |

date as per |

|

Since |

Remarks |

||

Work |

|

||||||

|

|

Measurement |

previous |

|

|||

|

|

|

|

||||

|

|

|

Book |

|

bill |

|

|

1 |

2 |

3 |

4 |

5 |

6 |

|

7 |

|

|

Rs. |

|

Rs. |

Rs. |

|

|

|

|

|

|

|

|

|

|

Total Value of work done

Deduct – Value of work shown on previous bill

Net value of work since previous bill (F)

Figure (F) in words Rs……………………………………………………………………

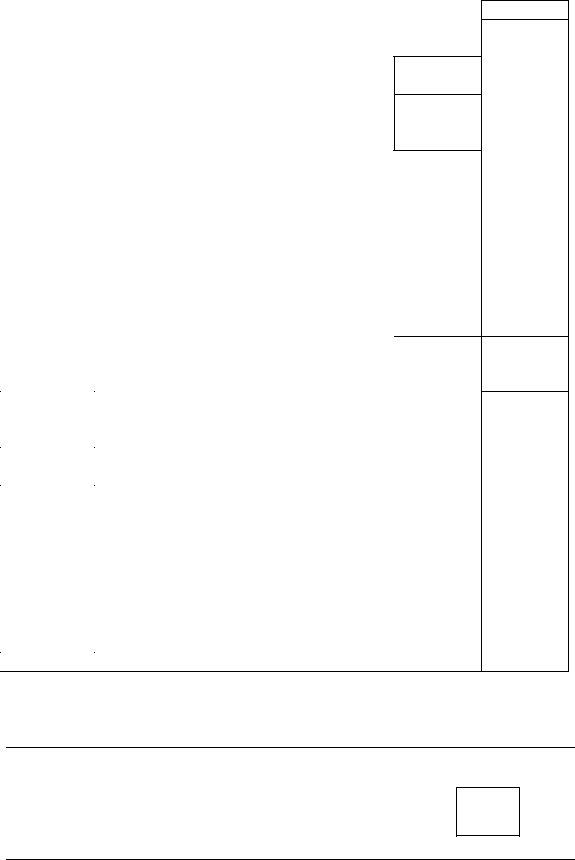

II– CERTIFICATES AND SIGNATURES

1.The measurements on which are based the entries in column 1 to 6 of Account I, were made by ………………………………. on …………………………… and are recorded at page …………… of Measurement Book No. ………………..

*2. Certified that in addition to and quite apart from the quantities of work actually executed as shown in column 4 of Account I, some work has actually been done in connection with several items and the value of such work (after deducting therefrom the proportionate amount of secured advances, if any, ultimately recoverable on account of the quantities of the materials used therein) is in no case, less than the advance payments as per item 2 of the memorandum of payments, made or proposed to be made, for the convenience of the contractor, in anticipation of and subject to the results of, detailed measurements, which will be made as soon as possible.

Dated signature of officer |

…………………….……… |

preparing the bill |

(Rank) …………………… |

¶ Dated signature of officer |

…………………….……… |

authorizing payment |

(Rank) …………………… |

……………………………….

Dated signature of contractor

* This certificate must be signed by the

¶This signature is necessary only when the officer who prepares the bill is not the officer who authorizes the payment. In such a case the two signatures are essential.

III – MEMORANDUM OF PAYMENTS

1. Total value of work actually measured, as per Acct.1, Col.5, Entry (A)

2. Total

Rs.

yet measured, as per details given below:

Rs.

(a)Total as per previous bill ………………….. (B)

(b)Since previous bill …………. as per page ………

of M.B. No. ……………………………… (D)

3.Total

………………………………………………

4.Total (items 1+2+3) …………………………………

5. Deduct – Amount withheld - |

|

|

Rs. |

|

Figures for |

(a) From previous bill as per last |

|

|

|

Running Account Bill…………….. |

|

|||

work |

|

|||

|

|

|

|

|

abstract |

(b) From this bill……………………… |

|

||

|

|

|||

|

6. Balance i.e., |

|||

|

7. Total amount of payments already made as per Entry |

|||

|

(K), of last Running Account Bill No. …………… of |

|||

|

…………forwarded with accounts for ………20……. |

|||

|

8. Payments now to be made, as detailed |

|

|

Rs. |

|

below : |

|

|

|

|

|

|

|

|

|

(a) By recovery of amounts creditable to |

|

||

|

this work - |

(a) |

|

|

|

…………………..………………. |

|

|

|

|

Total 5(b) +8 (a) ………………………(G) |

|

||

|

(b) By recovery of amounts creditable to |

|

||

|

other works or Heads of Account. (b) |

|

||

|

(i)0021- Income Tax @ 2% |

|

|

|

|

(ii) other Recoveries |

|

|

|

|

(c) By cheque ± ………………………. |

|

||

|

Total 8(b) + (c) ………………………...(H) |

|

||

5

Pay Rs. ¶ (…………………..) …………………………………………………………..

± (by cheque)

Dated initials of Disbursing Officer

Received Rs. ¶¶ (………………..) ……………………………………………………….

as per above memorandum, on account of this work.

Dated ……………. 20………..

Stamp

**Witness ……………………….Signature of contractor

Paid by me, vide cheque No………………. dated ………….20……….

Dated initials of person actually making the payment

* This figure should be tested to see that it agrees with the total of items 7 and 8.

±If the net amount to be paid is less than Rs.10 and it cannot be included in a cheque the payment should be made in cash, this entry being altered suitably and the alteration attested by dated initials.

¶ Here specify the net amount payable, vide item 8(c).

¶¶The payee’s acknowledgement should be for the gross amount paid as per item

8 (i.e. a+b+c).

**Payment should be attested by some known person when the payees acknowledgement is taken by mark, seal or thump impassion.

(±)May be considered for deletions in terms of Note 3 below Rule 42 of CGA (R&P) Riles, 1983

IV – REMARKS

(This space is reserved for any remarks which the Disbursing Officer or the Divisional Officer may wish to record in respect of the execution of the work, check of measurements or the state of contractor’s account.)

For use in Divisional Office

Checked

Accounts Clerk |

Divisional Accountant. |

|

|

For use in Pay and Accounts Office

Audited |

Reviewed |

Accountant |

JAO/AAO |

Pay & Accounts Officer |

FORM 26 A |

|

ACCOUNT OF SECURED ADVANCES |

|

(Referred to in paragraphs 10.2.14) |

|

(To be annexed to Form 26 where necessary) |

|

Division …………………………………. |

|

..…………………………….. |

|

Name of Contractor ……………………… |

Name of work……………………… |

…………………………… |

|

Cash Book Voucher No. …………………. dated ……………… |

|

S.No. of the Bill to which the Account pertains to ……………………… |

Reference to Agreement ……………… |

Quantity

outstanding

from

previous

bill

1

Deduct-

Quantity utilized in work measured since previous bill 2

Account of Secured Advance allowed on the Security of Materials Brought to Site

* Quantity |

Full Rate |

|

|

|

|

Reference to |

|

outstanding |

|

|

|

|

Divisional |

||

as |

|

|

Reduced rate |

|

|||

including |

Description |

|

** |

Officer’s |

|||

assessed |

|

at which |

|||||

quantity |

of |

Unit |

date amount |

written |

|||

by the |

advance is |

||||||

brought to |

Materials |

|

of advance |

orders |

|||

Divisional |

|

made |

|||||

site since |

|

|

|

authorizing |

|||

Officer |

|

|

|

|

|||

previous bill |

|

|

|

|

the advance |

||

|

|

|

|

|

|||

3 |

4 |

5 |

6 |

7 |

8 |

9 |

Reasons for

of Advance

when

outstanding for

more than 3

months

10

Total amount outstanding as per this account …………………. (C) ……………….

Deduct – Amount outstanding as per entry (C) of Annexure to the previous bill ……………………

Net amount since previous bill (in words) Rupees…………………………………………..(E)

*Entries relating to each description of materials should be posted thus in column 3. First enter the difference between quantities in Cols.1 & 2. Then show below this entry, the quantities, if any brought to site against which a further advance has been authorised, this entry being prefixed by the plus sign.

Finally, strike the total of the two entries, which will represent the total quantities outstanding. ** Entries in column 8 show the money values of the total quantities outstanding as per column 3.

Certificates and Signatures

¶Certified (1) that the plus quantities of materials shown in column 3 of the Account above have actually been brought by the Contractor to the site of the work and the contractor had not previously received any advance on their security (2) that these materials are of an imperishable nature and all are required by the Contractor for use on the work in connection with the items for which rates for finished work have been agreed upon, and (3) that a formal agreement in Form 31 signed and executed by the Contractor in accordance with Paragraphs 10.2.24 (a) of the Central Public Works Account Code in the Divisional Office.

Dated signature of Officer preparing the bill (Rank) ……………………..

±Dated signature of Officer authorizing payment (Rank) ……………………..

¶These Certificates must be signed by the

±This signature is necessary only when officer who prepares the bill is not the officer who authorizes the payment. In such a case the two signatures are essential.