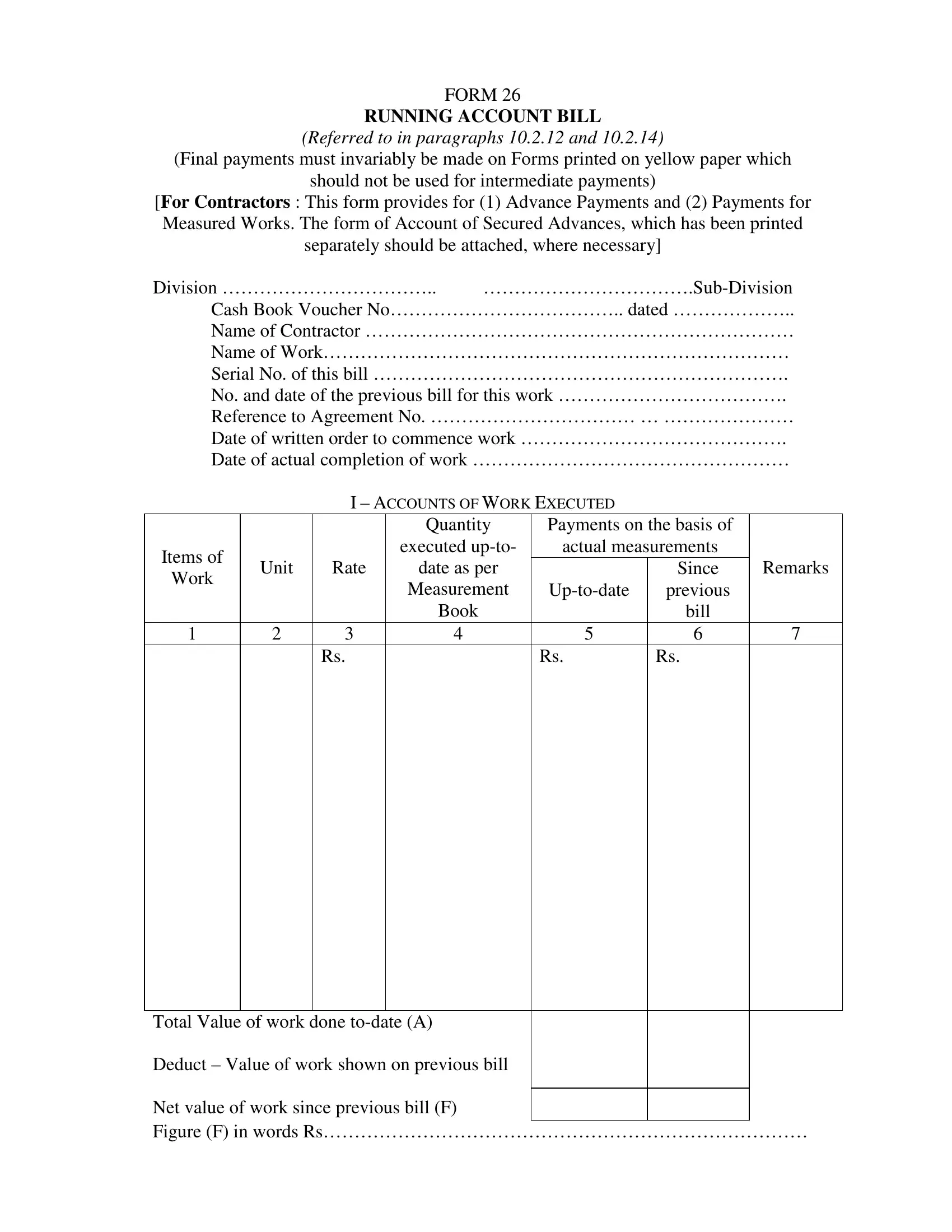

Understanding the intricacies of Form 26, known as the Running Account Bill, plays a pivotal role in the domain of contractual agreements and financial management within construction projects. Serving a dual purpose, this form facilitates both advance payments and payments for measured works, thereby ensuring a streamlined financial flow between contractors and project managers. Its design accommodates the detailing of executed work quantities, associated unit rates, and the resulting financial calculations, which are pivotal for maintaining transparency and accuracy in contractor payments. Noteworthy is the requirement for this document, particularly its final payments version, to be printed on yellow paper, a unique attribute that underscores its importance in the final settlement process. The form encapsulates a meticulous structure, divided into sections that cover accounts of work executed, certificates and signatures to validate the work, and a memorandum of payments that outlines advance payments, secured advances, and the actual payments to be made. This comprehensive approach ensures that all financial transactions are recorded meticulously, offering a safeguard against discrepancies and fostering trust between all involved parties. Moreover, the stipulation for the signing of certificates by designated officers adds an additional layer of verification, ensuring that the payments made or to be made are firmly rooted in the actual work completed, thus reinforcing accountability and precision in financial dealings.

| Question | Answer |

|---|---|

| Form Name | Form 26 |

| Form Length | 7 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 45 sec |

| Other names | secured advance form 26a cpwd pdf, secured advance form 26a cpwd, form number 26 is used for in civil engineering, running account bill form 26 pdf |