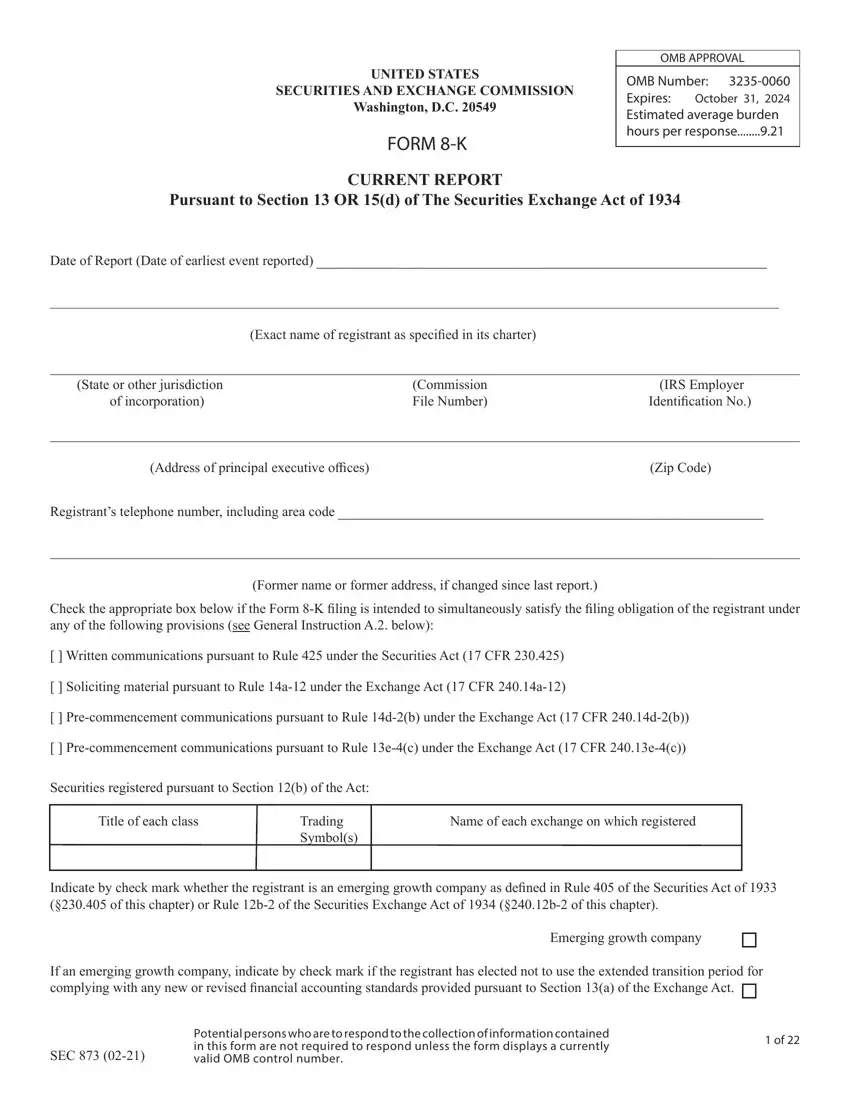

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

OMB APPROVAL

OMB Number: 3235-0060

Expires: October 31, 2024 Estimated average burden hours per response........9.21

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of The Securities Exchange Act of 1934

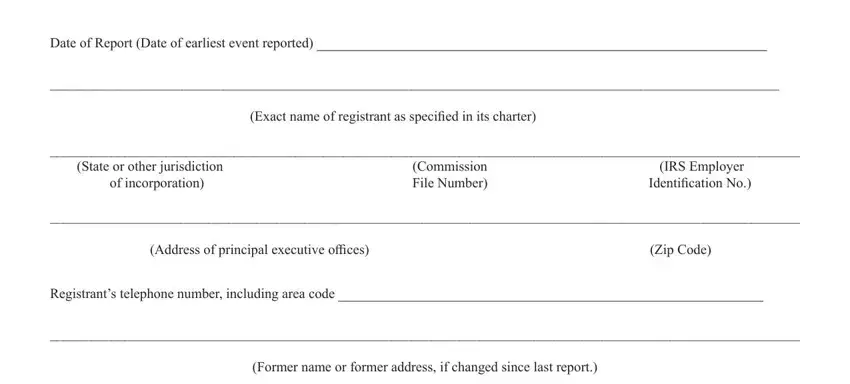

Date of Report (Date of earliest event reported) ______________________________________________________

_________________________________________________________________________________________________________

(Exact name of registrant as specified in its charter)

______________________________________________________________________________________________________________

(State or other jurisdiction |

(Commission |

(IRS Employer |

of incorporation) |

File Number) |

Identification No.) |

_____________________________________________________________________________________________________________

(Address of principal executive offices)(Zip Code)

Registrant’s telephone number, including area code ___________________________________________________

______________________________________________________________________________________________________________

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

[ ] Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

[ ] Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

[ ] Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

[ ] Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

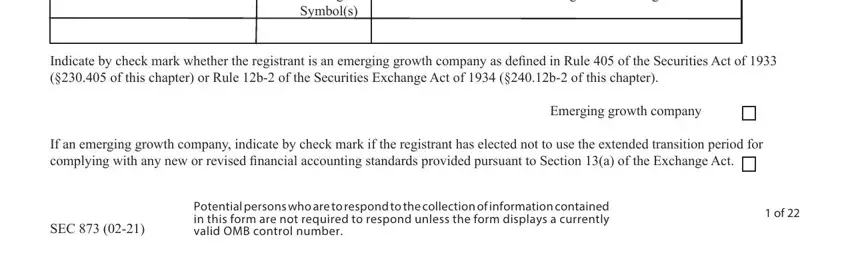

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading |

|

Symbol(s) |

Name of each exchange on which registered

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

|

|

Potential persons who are to respond to the collection of information contained |

1 of 22 |

|

SEC 873 (02-21) |

in this form are not required to respond unless the form displays a currently |

|

|

|

valid OMB control number. |

|

GENERAL INSTRUCTIONS

A. Rule as to Use of Form 8-K.

1.Form 8-K shall be used for current reports under Section 13 or 15(d) of the Securities Exchange Act of 1934, filed pursuant to Rule 13a-11 or Rule 15d-11 and for reports of nonpublic information required to be disclosed by Regulation FD (17 CFR 243.100 and 243.101).

2.Form 8-K may be used by a registrant to satisfy its filing obligations pursuant to Rule 425 under the Securities Act, regarding written communications related to business combination transactions, or Rules 14a-12(b) or Rule 14d-2(b) under the Exchange Act, relating to soliciting materials and pre-commencement communications pursuant to tender offers, respectively, provided that the Form 8-K filing satisfies all the substantive requirements of those rules (other than the Rule 425(c) requirement to include certain specified information in any prospectus filed pursuant to such rule). Such filing is also deemed to be filed pursuant to any rule for which the box is checked. A registrant is not required to check the box in connection with Rule 14a-12(b) or Rule 14d-2(b) if the communication is filed pursuant to Rule 425. Communications filed pursuant to Rule 425 are deemed filed under the other applicable sections. See Note 2 to Rule 425, Rule 14a-12(b) and Instruction 2 to Rule 14d-2(b)(2).

B.Events to be Reported and Time for Filing of Reports.

1.A report on this form is required to be filed or furnished, as applicable, upon the occurrence of any one or more of the events specified in the items in Sections 1 - 6 and 9 of this form. Unless otherwise specified, a report is to be filed or furnished within four business days after occurrence of the event. If the event occurs on a Saturday, Sunday or holiday on which the Commission is not open for business, then the four business day period shall begin to run on, and include, the first business day thereafter. A registrant either furnishing a report on this form under Item 7.01 (Regulation FD Disclosure) or electing to file a report on this form under Item 8.01 (Other Events) solely to satisfy its obligations under Regulation FD (17 CFR 243.100 and 243.101) must furnish such report or make such filing, as applicable, in accordance with the requirements of Rule 100(a) of Regulation FD (17 CFR 243.100(a)), including the deadline for furnishing or filing such report. A report pursuant to Item 5.08 is to be filed within four business days after the registrant determines the anticipated meeting date.

2.The information in a report furnished pursuant to Item 2.02 (Results of Operations and Financial Condition) or Item 7.01 (Regulation FD Disclosure) shall not be deemed to be “filed” for purposes of Section 18 of the Exchange Act or otherwise subject to the liabilities of that section, unless the registrant specifically states that the information is to be considered “filed” under the Exchange Act or incorporates it by reference into a filing under the Securities Act or the Exchange Act. If a report on Form 8-K contains disclosures under Item 2.02 or Item 7.01, whether or not the report contains disclosures regarding other items, all exhibits to such report relating to Item 2.02 or Item 7.01 will be deemed furnished, and not filed, unless the registrant specifies, under Item 9.01 (Financial Statements and Exhibits), which exhibits, or portions of exhibits, are intended to be deemed filed rather than furnished pursuant to this instruction.

3.If the registrant previously has reported substantially the same information as required by this form, the registrant need not make an additional report of the information on this form. To the extent that an item calls for disclosure of developments concerning a previously reported event or transaction, any information required in the new report or amendment about the previously reported event or transaction may be provided by incorporation by reference to the previously filed report. The term previously reported is defined in Rule 12b-2 (17 CFR 240.12b-2).

4.Copies of agreements, amendments or other documents or instruments required to be filed pursuant to Form 8-K are not required to be filed or furnished as exhibits to the Form 8-K unless specifically required to be filed or furnished by the applicable Item. This instruction does not affect the requirement to otherwise file such agreements, amendments or other documents or instruments, including as exhibits to registration statements and periodic reports pursuant to the requirements of Item 601 of Regulation S-K.

5.When considering current reporting on this form, particularly of other events of material importance pursuant to Item 7.01 (Regulation FD Disclosure) and Item 8.01(Other Events), registrants should have due regard for the accuracy, completeness and currency of the information in registration statements filed under the Securities Act which incorporate by reference information in reports filed pursuant to the Exchange Act, including reports on this form.

6.A registrant’s report under Item 7.01 (Regulation FD Disclosure) or Item 8.01 (Other Events) will not be deemed an admission as to the materiality of any information in the report that is required to be disclosed solely by Regulation FD.

C. Application of General Rules and Regulations.

1.The General Rules and Regulations under the Act (17 CFR Part 240) contain certain general requirements which are applicable to reports on any form. These general requirements should be carefully read and observed in the preparation and filing of reports on this form.

2.Particular attention is directed to Regulation 12B (17 CFR 240.12b-1 et seq.) which contains general requirements regarding matters such as the kind and size of paper to be used, the legibility of the report, the information to be given whenever the title of securities is required to be stated, and the filing of the report. The definitions contained in Rule 12b-2 should be especially noted. See also Regulations 13A (17 CFR 240.13a-1 et seq.) and 15D (17 CFR 240.1 5d-1 et seq.).

D.Preparation of Report.

This form is not to be used as a blank form to be filled in, but only as a guide in the preparation of the report on paper meeting the requirements of Rule 12b-12 (17 CFR 240.12b-12). The report shall contain the number and caption of the applicable item, but the text of such item may be omitted, provided the answers thereto are prepared in the manner specified in Rule 12b-13 (17 CFR 240.12b-13). To the extent that Item 1.01 and one or more other items of the form are applicable, registrants need not provide the number and caption of Item 1.01 so long as the substantive disclosure required by Item 1.01 is disclosed in the report and the number and caption of the other applicable item(s) are provided. All items that are not required to be answered in a particular report may be omitted and no reference thereto need be made in the report. All instructions should also be omitted.

E. Signature and Filing of Report.

Three complete copies of the report, including any financial statements, exhibits or other papers or documents filed as a part thereof, and five additional copies which need not include exhibits, shall be filed with the Commission. At least one complete copy of the report, including any financial statements, exhibits or other papers or documents filed as a part thereof, shall be filed, with each exchange on which any class of securities of the registrant is registered. At least one complete copy of the report filed with the Commission and one such copy filed with each exchange shall be manually signed. Copies not manually signed shall bear typed or printed signatures.

F. Incorporation by Reference.

If the registrant makes available to its stockholders or otherwise publishes, within the period prescribed for filing the report, a press release or other document or statement containing information meeting some or all of the requirements of this form, the information called for may be incorporated by reference to such published document or statement, in answer or partial answer to any item or items of this form, provided copies thereof are filed as an exhibit to the report on this form.

G. Use of this Form by Asset-Backed Issuers.

The following applies to registrants that are asset-backed issuers. Terms used in this General Instruction G. have the same meaning as in Item 1101 of Regulation AB (17 CFR 229.1101).

1.Reportable Events That May Be Omitted.

The registrant need not file a report on this Form upon the occurrence of any one or more of the events specified in the following:

(a)Item 2.01, Completion of Acquisition or Disposition of Assets;

(b)Item 2.02, Results of Operations and Financial Condition;

(c)Item 2.03, Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement of a Registrant;

(d)Item 2.05, Costs Associated with Exit or Disposal Activities;

(e)Item 2.06, Material Impairments;

(f)Item 3.01, Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing;

(g)Item 3.02, Unregistered Sales of Equity Securities;

(h)Item 4.01, Changes in Registrant’s Certifying Accountant;

(i)Item 4.02, Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or Completed Interim Review;

(j)Item 5.01, Changes in Control of Registrant;

(k)Item 5.02, Departure of Directors or Principal Officers; Election of Directors; Appointment of Principal Officers;

(l) Item 5.04, Temporary Suspension of Trading Under Registrant’s Employee Benefit Plans; and

(m)Item 5.05, Amendments to the Registrant’s Code of Ethics, or Waiver of a Provision of the Code of Ethics. 2. Additional Disclosure for the Form 8-K Cover Page.

Immediately after the name of the issuing entity on the cover page of the Form 8-K, as separate line items, identify the exact name of the depositor as specified in its charter and the exact name of the sponsor as specified in its charter. Include a Central Index Key number for the depositor and the issuing entity, and if available, the sponsor.

3.Signatures.

The Form 8-K must be signed by the depositor. In the alternative, the Form 8-K may be signed on behalf of the issuing entity by a duly authorized representative of the servicer. If multiple servicers are involved in servicing the pool assets, a duly authorized representative of the master servicer (or entity performing the equivalent function) must sign if a representative of the servicer is to sign the report on behalf of the issuing entity.

INFORMATION TO BE INCLUDED IN THE REPORT

Section 1 - Registrant’s Business and Operations

Item 1.01 Entry into a Material Definitive Agreement.

(a)If the registrant has entered into a material definitive agreement not made in the ordinary course of business of the registrant, or into any amendment of such agreement that is material to the registrant, disclose the following information:

(1)the date on which the agreement was entered into or amended, the identity of the parties to the agreement or amendment and a brief description of any material relationship between the registrant or its affiliates and any of the parties, other than in respect of the material definitive agreement or amendment; and

(2)a brief description of the terms and conditions of the agreement or amendment that are material to the registrant.

(b)For purposes of this Item 1.01, a material definitive agreement means an agreement that provides for obligations that are material to and enforceable against the registrant, or rights that are material to the registrant and enforceable by the registrant against one or more other parties to the agreement, in each case whether or not subject to conditions.

Instructions.

1.Any material definitive agreement of the registrant not made in the ordinary course of the registrant’s business must be disclosed under this Item 1.01. An agreement is deemed to be not made in the ordinary course of a registrant’s business even if the agreement is such as ordinarily accompanies the kind of business conducted by the registrant if it involves the subject matter identified in Item 601(b)(10)(ii)

(A) - (D) of Regulation S-K (17 CFR 229.601(b)(10)(ii)(A) - (D)). An agreement involving the subject matter identified in Item 601(b) (10)(iii)(A) or (B) need not be disclosed under this Item.

2.A registrant must provide disclosure under this Item 1.01 if the registrant succeeds as a party to the agreement or amendment to the

agreement by assumption or assignment (other than in connection with a merger or acquisition or similar transaction).

3.With respect to asset-backed securities, as defined in Item 1101 of Regulation AB (17 CFR 229.1101), disclosure is required under this Item 1.01 regarding the entry into or an amendment to a definitive agreement that is material to the asset-backed securities transaction, even if the registrant is not a party to such agreement (e.g., a servicing agreement with a servicer contemplated by Item 1108(a)(3) of Regulation AB (17 CFR 229.1108(a)(3)).

4.To the extent a material definitive agreement is filed as an exhibit under this Item 1.01, schedules (or similar attachments) to the exhibits are not required to be filed unless they contain information material to an investment or voting decision and that information is not otherwise disclosed in the exhibit or the disclosure document. Each exhibit filed must contain a list briefly identifying the contents of all omitted schedules. Registrants need not prepare a separate list of omitted information if such information is already included within the exhibit in a manner that conveys the subject matter of the omitted schedules and attachments. In addition, the registrant must provide a copy of any omitted schedule to the Commission or its staff upon request.

5.To the extent a material definitive agreement is filed as an exhibit under this Item 1.01, the registrant may redact information from the exhibit if disclosure of such information would constitute a clearly unwarranted invasion of personal privacy (e.g., disclosure of bank account numbers, social security numbers, home addresses and similar information).

6.To the extent a material definitive agreement is filed as an exhibit under this Item 1.01, the registrant may redact provisions or

terms of the exhibit if those provisions or terms are both (i) not material and (ii) would likely cause competitive harm to the registrant if publicly disclosed, provided that the registrant intends to incorporate by reference this filing into its future periodic reports or registration statements, as applicable, in satisfaction of Item 601(b)(10) of Regulation S-K. If it chooses to redact information pursuant to this instruction, the registrant should mark the exhibit index to indicate that portions of the exhibit or exhibits have been omitted and include a prominent statement on the first page of the redacted exhibit that certain identified information has been excluded from the exhibit because it is both (i) not material and (ii) would likely cause competitive harm to the registrant if publicly disclosed. The registrant also must indicate by brackets where the information is omitted from the filed version of the exhibit.

If requested by the Commission or its staff, the registrant must promptly provide an unredacted copy of the exhibit on a supplemental basis. The Commission or its staff also may request the registrant to provide its materiality and competitive harm analyses on a supplemental basis. Upon evaluation of the registrant’s supplemental materials, the Commission or its staff may request the registrant to amend its filing to include in the exhibit any previously redacted information that is not adequately supported by the registrant’s materiality and competitive harm analyses.

The registrant may request confidential treatment of the supplemental material submitted under Instruction 6 of this Item pursuant to Rule 83 (§ 200.83 of this chapter) while it is in the possession of the Commission or its staff. After completing its review of the supplemental information, the Commission or its staff will return or destroy it at the request of the registrant, if the registrant complies with the procedures outlined in Rules 418 or 12b-4 (§ 230.418 or 240.12b-4 of this chapter).

Item 1.02 Termination of a Material Definitive Agreement.

(a)If a material definitive agreement which was not made in the ordinary course of business of the registrant and to which the registrant is a party is terminated otherwise than by expiration of the agreement on its stated termination date, or as a result of all parties completing their obligations under such agreement, and such termination of the agreement is material to the registrant, disclose the following information:

(1)the date of the termination of the material definitive agreement, the identity of the parties to the agreement and a brief description of any material relationship between the registrant or its affiliates and any of the parties other than in respect of the material definitive agreement;

(2)a brief description of the terms and conditions of the agreement that are material to the registrant;

(3)a brief description of the material circumstances surrounding the termination; and

(4)any material early termination penalties incurred by the registrant.

(b)For purposes of this Item 1.02, the term material definitive agreement shall have the same meaning as set forth in Item 1.01(b). Instructions.

1.No disclosure is required solely by reason of this Item 1.02 during negotiations or discussions regarding termination of a material definitive agreement unless and until the agreement has been terminated.

2.No disclosure is required solely by reason of this Item 1.02 if the registrant believes in good faith that the material definitive agreement has not been terminated, unless the registrant has received a notice of termination pursuant to the terms of agreement.

3.With respect to asset-backed securities, as defined in Item 1101 of Regulation AB (17 CFR 229.1101), disclosure is required under this Item 1.02 regarding the termination of a definitive agreement that is material to the asset-backed securities transaction (otherwise than by expiration of the agreement on its stated termination date or as a result of all parties completing their obligations under such agreement), even if the registrant is not a party to such agreement (e.g., a servicing agreement with a servicer contemplated by Item 1108(a)(3) of Regulation AB (17 CFR 229.1108(a)(3)).

Item 1.03 Bankruptcy or Receivership.

(a)If a receiver, fiscal agent or similar officer has been appointed for a registrant or its parent, in a proceeding under the U.S. Bankruptcy Code or in any other proceeding under state or federal law in which a court or governmental authority has assumed jurisdiction over substantially all of the assets or business of the registrant or its parent, or if such jurisdiction has been assumed by leaving the existing directors and officers in possession but subject to the supervision and orders of a court or governmental authority, disclose the following information:

(1)the name or other identification of the proceeding;

(2)the identity of the court or governmental authority;

(3)the date that jurisdiction was assumed; and

(4)the identity of the receiver, fiscal agent or similar officer and the date of his or her appointment.

(b)If an order confirming a plan of reorganization, arrangement or liquidation has been entered by a court or governmental authority having supervision or jurisdiction over substantially all of the assets or business of the registrant or its parent, disclose the following;

(1)the identity of the court or governmental authority;

(2)the date that the order confirming the plan was entered by the court or governmental authority;

(3)a summary of the material features of the plan and, pursuant to Item 9.01 (Financial Statements and Exhibits), a copy of the plan as confirmed;

(4)the number of shares or other units of the registrant or its parent issued and outstanding, the number reserved for future issuance in respect of claims and interests filed and allowed under the plan, and the aggregate total of such numbers; and

(5)information as to the assets and liabilities of the registrant or its parent as of the date that the order confirming the plan was entered, or a date as close thereto as practicable.

Instructions.

1.The information called for in paragraph (b)(5) of this Item 1.03 may be presented in the form in which it was furnished to the court or governmental authority.

2.With respect to asset-backed securities, disclosure also is required under this Item 1.03 if the depositor (or servicer if the servicer signs the report on Form 10-K (17 CFR 249.310) of the issuing entity) becomes aware of any instances described in paragraph (a) or

(b) of this Item with respect to the sponsor, depositor, servicer contemplated by Item 1108(a)(3) of Regulation AB (17 CFR 229.1108(a) (3)), trustee, significant obligor, enhancement or support provider contemplated by Items 1114(b) or 1115 of Regulation AB (17 CFR 229.1114(b) or 229.1115) or other material party contemplated by Item 1101(d)(1) of Regulation AB (17 CFR 1101(d)(1)). Terms used in this Instruction 2 have the same meaning as in Item 1101 of Regulation AB (17 CFR 229.1101).

Item 1.04 Mine Safety – Reporting of Shutdowns and Patterns of Violations.

(a)If the registrant or a subsidiary of the registrant has received, with respect to a coal or other mine of which the registrant or a subsidiary of the registrant is an operator

•an imminent danger order issued under section 107(a) of the Federal Mine Safety and Health Act of 1977 (30

U.S.C. 817(a));

•a written notice from the Mine Safety and Health Administration that the coal or other mine has a pattern of violations of mandatory health or safety standards that are of such nature as could have significantly and substantially contributed to the cause and effect of coal or other mine health or safety hazards under section 104(e) of such Act (30 U.S.C. 814(e)); or

•a written notice from the Mine Safety and Health Administration that the coal or other mine has the potential to have such a pattern, disclose the following information:

(1)The date of receipt by the issuer or a subsidiary of such order or notice.

(2)The category of the order or notice.

(3)The name and location of the mine involved.

Instructions to Item 1.04.

1.The term “coal or other mine” means a coal or other mine, as defined in section 3 of the Federal Mine Safety and Health Act of 1977 (30 U.S.C. 802), that is subject to the provisions of such Act (30 U.S.C. 801 et seq).

2.The term “operator” has the meaning given the term in section 3 of the Federal Mine Safety and Health Act of 1977 (30 U.S.C. 802).

Section 2 - Financial Information

Item 2.01 Completion of Acquisition or Disposition of Assets.

If the registrant or any of its subsidiaries consolidated has completed the acquisition or disposition of a significant amount of assets, otherwise than in the ordinary course of business, or the acquisition or disposition of a significant amount of assets that constitute a real estate operation as defined in § 210.3-14(a)(2) disclose the following information:

(a)the date of completion of the transaction;

(b)a brief description of the assets involved;

(c)the identity of the person(s) from whom the assets were acquired or to whom they were sold and the nature of any material relationship, other than in respect of the transaction, between such person(s) and the registrant or any of its affiliates, or any director or officer of the registrant, or any associate of any such director or officer;

(d)the nature and amount of consideration given or received for the assets and, if any material relationship is disclosed pursuant to paragraph (c) of this Item 2.01, the formula or principle followed in determining the amount of such consideration;

(e)if the transaction being reported is an acquisition and if a material relationship exists between the registrant or any of its affiliates and the source(s) of the funds used in the acquisition, the identity of the source(s) of the funds unless all or any part of the consideration used is a loan made in the ordinary course of business by a bank as defined by Section 3(a)(6) of the Act, in which case the identity of such bank may be omitted provided the registrant:

(1)has made a request for confidentiality pursuant to Section 13(d)(1)(B) of the Act; and

(2)states in the report that the identity of the bank has been so omitted and filed separately with the Commission; and

(f)if the registrant was a shell company, other than a business combination related shell company, as those terms are defined in Rule 12b-2 under the Exchange Act (17 CFR 240.12b-2), immediately before the transaction, the information that would be required if the registrant were filing a general form for registration of securities on Form 10 under the Exchange Act reflecting all classes of the registrant’s securities subject to the reporting requirements of Section 13 (15 U.S.C. 78m) or Section 15(d) (15 U.S.C. 78o(d)) of such Act upon consummation of the transaction. Notwithstanding General Instruction B.3. to Form 8-K, if any disclosure required by this Item 2.01(f) is previously reported, as that term is defined in Rule 12b-2 under the Exchange Act (17 CFR 240.12b-2), the registrant may identify the filing in which that disclosure is included instead of including that disclosure in this report.

Instructions.

1.No information need be given as to:

(i)any transaction between any person and any wholly-owned subsidiary of such person;

(ii)any transaction between two or more wholly-owned subsidiaries of any person; or

(iii)the redemption or other acquisition of securities from the public, or the sale or other disposition of securities to the public, by the issuer of such securities or by a wholly-owned subsidiary of that issuer.

2.The term acquisition includes every purchase, acquisition by lease, exchange, merger, consolidation, succession or other acquisition, except that the term does not include the construction or development of property by or for the registrant or its subsidiaries or the acquisition

of materials for such purpose. The term disposition includes every sale, disposition by lease, exchange, merger, consolidation, mortgage, assignment or hypothecation of assets, whether for the benefit of creditors or otherwise, abandonment, destruction, or other disposition.

3.The information called for by this Item 2.01 is to be given as to each transaction or series of related transactions of the size indicated. The acquisition or disposition of securities is deemed the indirect acquisition or disposition of the assets represented by such securities if it results in the acquisition or disposition of control of such assets.

4.An acquisition or disposition will be deemed to involve a significant amount of assets:

(i)if the registrant’s and its other subsidiaries’ equity in the net book value of such assets or the amount paid or received for the assets upon such acquisition or disposition exceeded 10 percent of the total assets of the registrant and its consolidated subsidiaries;

(ii)if it involved a business (see 17 CFR 210.11-01(d)) that is significant (see 17 CFR 210.11-01(b)). The acquisition of a business encompasses the acquisition of an interest in a business accounted for by the registrant under the equity method or, in lieu of the equity method, the fair value option; or

(iii)in the case of a business development company, if the amount paid for such assets exceeded 10 percent of the value of the total investments of the registrant and its consolidated subsidiaries.

The aggregate impact of acquired businesses are not required to be reported pursuant to this Item 2.01 unless they are related businesses (see 17 CFR 210.3-05(a)(3)), related real estate operations (see 17 CFR 210.3-14(a)(3)), or related funds (see 17 CFR 210.6-11(a)(3)), and are significant in the aggregate.

5.Attention is directed to the requirements in Item 9.01 (Financial Statements and Exhibits) with respect to the filing of:

(i)financial statements of businesses or funds acquired;

(ii)pro forma financial information; and

(iii)copies of the plans of acquisition or disposition as exhibits to the report.

Item 2.02 Results of Operations and Financial Condition.

(a)If a registrant, or any person acting on its behalf, makes any public announcement or release (including any update of an earlier announcement or release) disclosing material non-public information regarding the registrant’s results of operations or financial condition for a completed quarterly or annual fiscal period, the registrant shall disclose the date of the announcement or release, briefly identify the announcement or release and include the text of that announcement or release as an exhibit.

(b)A Form 8-K is not required to be furnished to the Commission under this Item 2.02 in the case of disclosure of material non- public information that is disclosed orally, telephonically, by webcast, by broadcast, or by similar means if:

(1)the information is provided as part of a presentation that is complementary to, and initially occurs within 48 hours after, a related, written announcement or release that has been furnished on Form 8-K pursuant to this Item 2.02 prior to the presentation;

(2)the presentation is broadly accessible to the public by dial-in conference call, by webcast, by broadcast or by similar means;

(3)the financial and other statistical information contained in the presentation is provided on the registrant’s website, together with any information that would be required under 17 CFR 244.100; and

(4)the presentation was announced by a widely disseminated press release, that included instructions as to when and how to access the presentation and the location on the registrant’s website where the information would be available.

Instructions.

1.The requirements of this Item 2.02 are triggered by the disclosure of material non-public information regarding a completed fiscal year or quarter. Release of additional or updated material non-public information regarding a completed fiscal year or quarter would trigger an additional Item 2.02 requirement.

2.The requirements of paragraph (e)(1)(i) of Item 10 of Regulation S-K (17 CFR 229.10(e)(1)(i)) shall apply to disclosures under this Item 2.02.

3.Issuers that make earnings announcements or other disclosures of material non-public information regarding a completed fiscal year or quarter in an interim or annual report to shareholders are permitted to specify which portion of the report contains the information required to be furnished under this Item 2.02.

4.This Item 2.02 does not apply in the case of a disclosure that is made in a quarterly report filed with the Commission on Form 10-Q (17 CFR 249.308a) or an annual report filed with the Commission on Form 10-K (17 CFR 249.310).

Item 2.03 Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement of a Registrant.

(a)If the registrant becomes obligated on a direct financial obligation that is material to the registrant, disclose the following information:

(1)the date on which the registrant becomes obligated on the direct financial obligation and a brief description of the transaction or agreement creating the obligation;

(2)the amount of the obligation, including the terms of its payment and, if applicable, a brief description of the material terms under which it may be accelerated or increased and the nature of any recourse provisions that would enable the registrant to recover from third parties; and

(3)a brief description of the other terms and conditions of the transaction or agreement that are material to the registrant.

(b)If the registrant becomes directly or contingently liable for an obligation that is material to the registrant arising out of an off-balance sheet arrangement, disclose the following information:

(1)the date on which the registrant becomes directly or contingently liable on the obligation and a brief description of the transaction or agreement creating the arrangement and obligation;

(2)a brief description of the nature and amount of the obligation of the registrant under the arrangement, including the material terms whereby it may become a direct obligation, if applicable, or may be accelerated or increased and the nature of any recourse provisions that would enable the registrant to recover from third parties;

(3)the maximum potential amount of future payments (undiscounted) that the registrant may be required to make, if different; and

(4)a brief description of the other terms and conditions of the obligation or arrangement that are material to the registrant.

(c)For purposes of this Item 2.03, direct financial obligation means any of the following:

(1)a long-term debt obligation means a payment obligation under long-term borrowings referenced in FASB ASC paragraph 470- 10-50-1 (Debt Topic) as may be modified or supplemented;

(2)a finance lease obligation means a payment obligation under a lease that would be classified as a finance lease pursuant to FASB ASC Topic 842, Leases, as may be modified or supplemented;

(3)an operating lease obligation means a payment obligation under a lease that would be classified as an operating lease pursuant to FASB ASC Topic 840, as may be modified or supplemented; or

(4)a short-term debt obligation that arises other than in the ordinary course of business.

(d)For purposes of this Item 2.03, off-balance sheet arrangement means any transaction, agreement or other contractual arrangement to which an entity unconsolidated with the registrant is a party, under which the registrant has:

(1)Any obligation under a guarantee contract that has any of the characteristics identified in FASB ASC paragraph 460-10-15-4 (Guarantees Topic), as may be modified or supplemented, and that is not excluded from the initial recognition and measurement provisions of FASB ASC paragraphs 460-10-15-7, 460-10-25-1, and 460-10-30-1.

(2)A retained or contingent interest in assets transferred to an unconsolidated entity or similar arrangement that serves as credit, liquidity or market risk support to such entity for such assets;

(3)Any obligation, including a contingent obligation, under a contract that would be accounted for as a derivative instrument, except that it is both indexed to the registrant’s own stock and classified in stockholders’ equity in the registrant’s statement of financial position, and therefore excluded from the scope of FASB ASC Topic 815, Derivatives and Hedging, pursuant to FASB ASC subparagraph

815-10-15-74(a), as may be modified or supplemented; or

(4)Any obligation, including a contingent obligation, arising out of a variable interest (as defined in the FASB ASC Master Glossary), as may be modified or supplemented) in an unconsolidated entity that is held by, and material to, the registrant, where such entity provides financing, liquidity, market risk or credit risk support to, or engages in leasing, hedging or research and development services with, the registrant.

(e)For purposes of this Item 2.03, short-term debt obligation means a payment obligation under a borrowing arrangement that is scheduled to mature within one year, or, for those registrants that use the operating cycle concept of working capital, within a registrant’s operating cycle that is longer than one year, as discussed in FASB ASC paragraph 210-10-45-3 (Balance Sheet Topic).

Instructions.

1.A registrant has no obligation to disclose information under this Item 2.03 until the registrant enters into an agreement enforceable against the registrant, whether or not subject to conditions, under which the direct financial obligation will arise or be created or issued. If there is no such agreement, the registrant must provide the disclosure within four business days after the occurrence of the closing or settlement of the transaction or arrangement under which the direct financial obligation arises or is created.

2.A registrant must provide the disclosure required by paragraph (b) of this Item 2.03 whether or not the registrant is also a party to the transaction or agreement creating the contingent obligation arising under the off-balance sheet arrangement. In the event that neither the registrant nor any affiliate of the registrant is also a party to the transaction or agreement creating the contingent obligation arising under the off-balance sheet arrangement in question, the four business day period for reporting the event under this Item 2.03 shall begin on the earlier of (i) the fourth business day after the contingent obligation is created or arises, and (ii) the day on which an executive officer, as defined in 17 CFR 240.3b-7, of the registrant becomes aware of the contingent obligation.

3.In the event that an agreement, transaction or arrangement requiring disclosure under this Item 2.03 comprises a facility, program or similar arrangement that creates or may give rise to direct financial obligations of the registrant in connection with multiple transactions, the registrant shall:

(i)disclose the entering into of the facility, program or similar arrangement if the entering into of the facility is material to the registrant; and

(ii)as direct financial obligations arise or are created under the facility or program, disclose the required information under this Item 2.03 to the extent that the obligations are material to the registrant (including when a series of previously undisclosed individually immaterial obligations become material in the aggregate).

4.For purposes of Item 2.03(b)(3), the maximum amount of future payments shall not be reduced by the effect of any amounts that may possibly be recovered by the registrant under recourse or collateralization provisions in any guarantee agreement, transaction or arrangement.

5.If the obligation required to be disclosed under this Item 2.03 is a security, or a term of a security, that has been or will be sold pursuant to an effective registration statement of the registrant, the registrant is not required to file a Form 8-K pursuant to this Item 2.03, provided that the prospectus relating to that sale contains the information required by this Item 2.03 and is filed within the required time period under Securities Act Rule 424 (§230.424 of this chapter).

Item 2.04 Triggering Events That Accelerate or Increase a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement.

(a)If a triggering event causing the increase or acceleration of a direct financial obligation of the registrant occurs and the consequences of the event, taking into account those described in paragraph (a)(4) of this Item 2.04, are material to the registrant, disclose the following information:

(1)the date of the triggering event and a brief description of the agreement or transaction under which the direct financial obligation was created and is increased or accelerated;

(2)a brief description of the triggering event;

(3)the amount of the direct financial obligation, as increased if applicable, and the terms of payment or acceleration that apply; and

(4)any other material obligations of the registrant that may arise, increase, be accelerated or become direct financial obligations as a result of the triggering event or the increase or acceleration of the direct financial obligation.

(b)If a triggering event occurs causing an obligation of the registrant under an off-balance sheet arrangement to increase or be accelerated, or causing a contingent obligation of the registrant under an off-balance sheet arrangement to become a direct financial

10