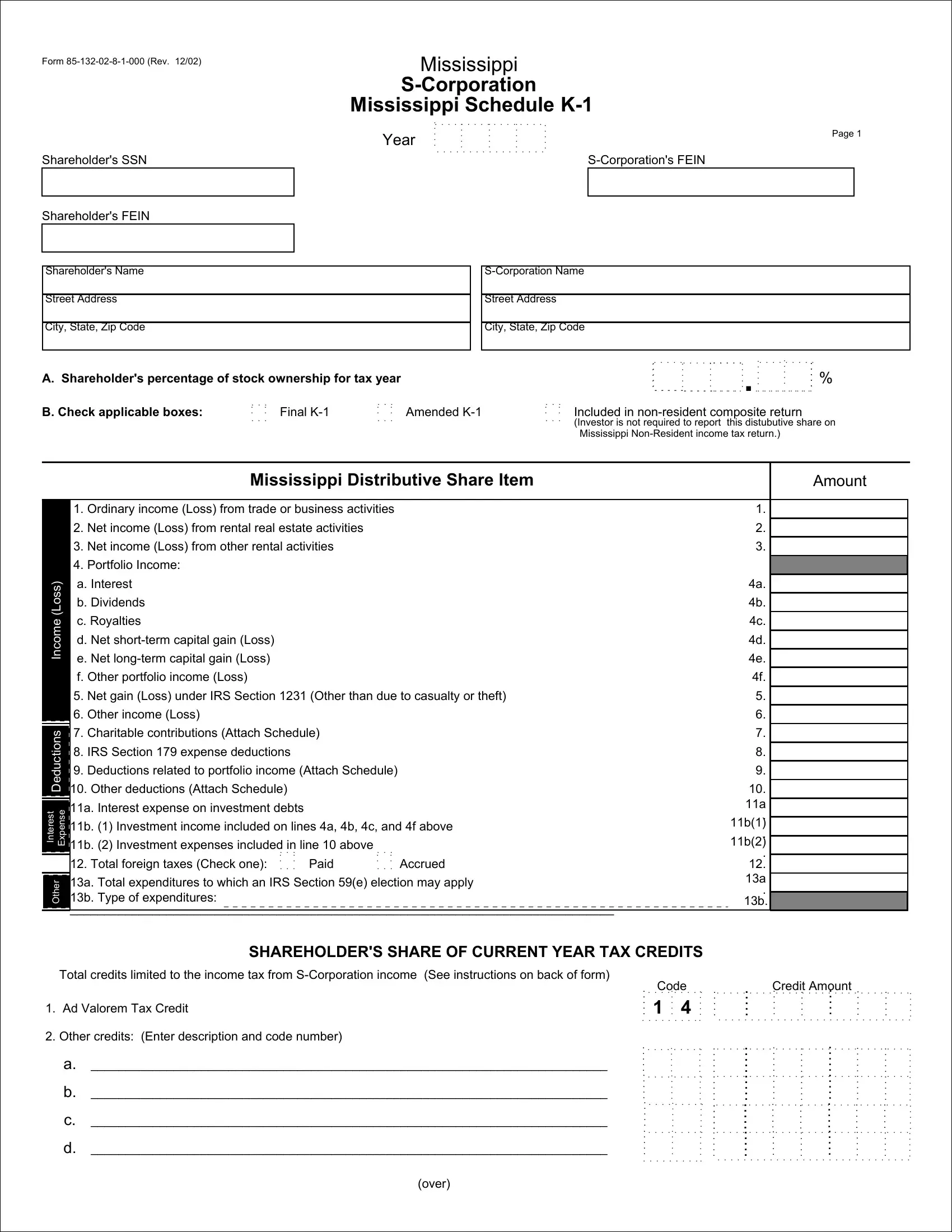

The Form 85-132-02-8-1-000, revised as of December 2002, serves as a critical document for Mississippi S-Corporations, providing a detailed Schedule K-1 for shareholders. This form comprehensively captures the shareholder's Social Security Number (SSN), the S-Corporation's Federal Employer Identification Number (FEIN), the shareholder's FEIN, and their respective names and addresses, alongside the shareholder’s percentage of stock ownership for the tax year. It facilitates the reporting of the Mississippi Distributive Share Items, emphasizing ordinary income or losses from various business activities, portfolio income, including interest and dividends, and specific income or losses such as those under IRS Section 1231 or from charitable contributions. Additionally, it itemizes deductions related to portfolio income, other deductions, and interest expenses on investment debts, presenting a methodology for the calculation of tax credits limited to income from S-Corporation activities. On page 2, the form outlines general restrictions on credits, detailing the utilization and carryforward guidelines for various tax credits available to shareholders, such as the ad valorem tax credit, the jobs tax credit, and the reforestation tax credit. This document not only provides key financial information for the year but also guides shareholders through the proper declaration and maximization of potential tax credits in accordance with Mississippi tax laws, making it an indispensable tool for S-Corporation shareholders within the state.

| Question | Answer |

|---|---|

| Form Name | Form 85 132 02 8 1 000 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 85132028 mississippi schedule k1 2014 form |