If you are a taxpayer who has chosen to file an income tax return using the self-employment tax form, Form 8611, then there are a few things you should know about this form. The first is that it can be used by both sole proprietors and partners in partnerships, and the second is that it is typically used by taxpayers who earn income from self-employment. If you have any questions about whether or not Form 8611 is the right form for you, or if you need help completing it, be sure to consult with a tax professional.

| Question | Answer |

|---|---|

| Form Name | Form 8611 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | CUSIP, Recordkeeping, OMB, 8609-A |

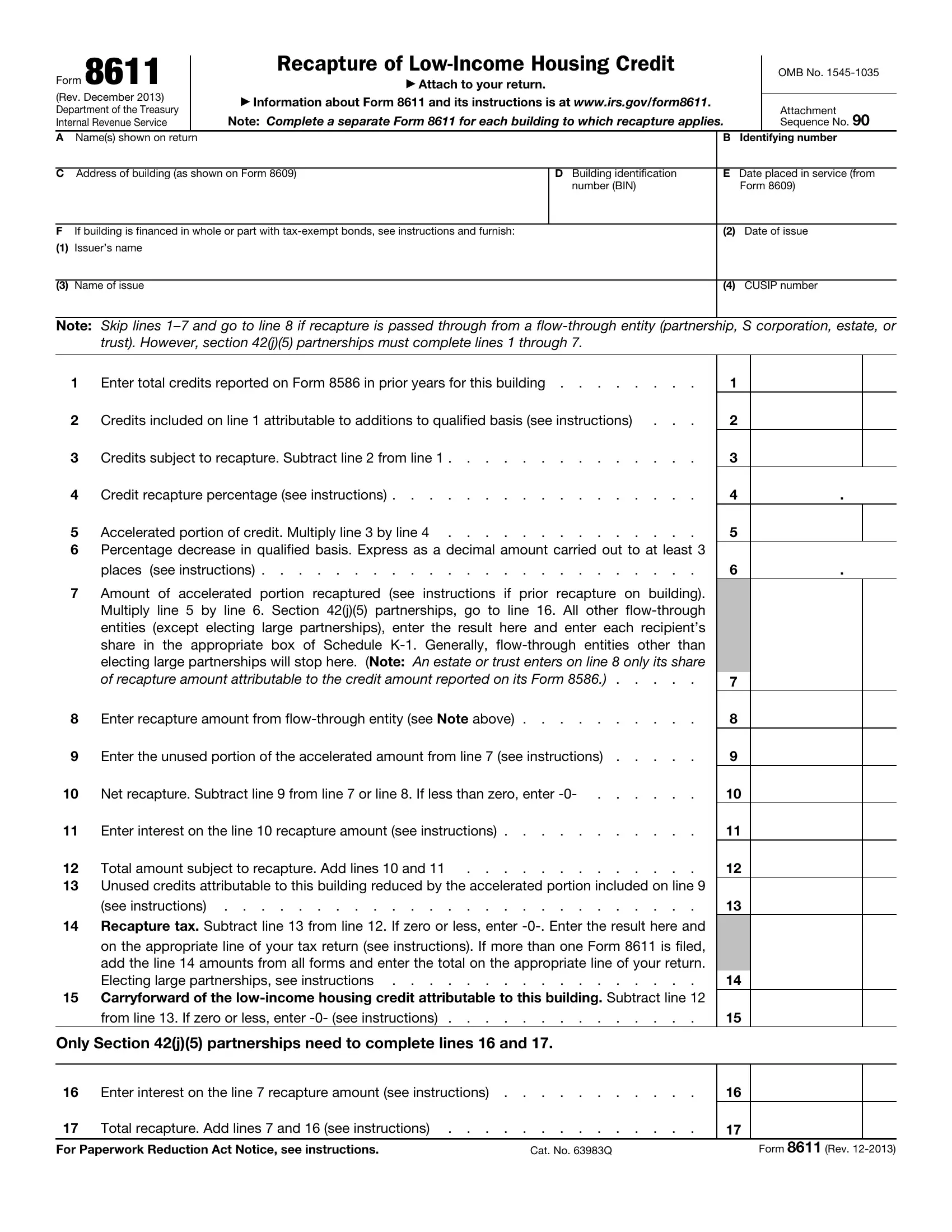

Form 8611

(Rev. December 2013)

Department of the Treasury

Internal Revenue Service

Recapture of

▶Attach to your return.

▶Information about Form 8611 and its instructions is at www.irs.gov/form8611. Note: Complete a separate Form 8611 for each building to which recapture applies.

OMB No.

Attachment Sequence No. 90

A Name(s) shown on return |

|

B |

Identifying number |

|

|

|

|

|

|

C |

Address of building (as shown on Form 8609) |

D Building identification |

E Date placed in service (from |

|

|

|

number (BIN) |

|

Form 8609) |

|

|

|

|

|

F |

If building is financed in whole or part with |

|

(2) |

Date of issue |

(1) |

Issuer’s name |

|

|

|

(3)Name of issue

(4)CUSIP number

Note: Skip lines

1 |

Enter total credits reported on Form 8586 in prior years for this building |

2 |

Credits included on line 1 attributable to additions to qualified basis (see instructions) . . . |

3 |

Credits subject to recapture. Subtract line 2 from line 1 |

4 |

Credit recapture percentage (see instructions) |

5 |

Accelerated portion of credit. Multiply line 3 by line 4 |

6Percentage decrease in qualified basis. Express as a decimal amount carried out to at least 3

places (see instructions) . . . . . . . . . . . . . . . . . . . . . . . .

7Amount of accelerated portion recaptured (see instructions if prior recapture on building). Multiply line 5 by line 6. Section 42(j)(5) partnerships, go to line 16. All other

electing large partnerships will stop here. (Note: An estate or trust enters on line 8 only its share of recapture amount attributable to the credit amount reported on its Form 8586.) . . . . .

8 |

Enter recapture amount from |

9 |

Enter the unused portion of the accelerated amount from line 7 (see instructions) |

10 |

Net recapture. Subtract line 9 from line 7 or line 8. If less than zero, enter |

11 |

Enter interest on the line 10 recapture amount (see instructions) |

12 |

Total amount subject to recapture. Add lines 10 and 11 |

13Unused credits attributable to this building reduced by the accelerated portion included on line 9

(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . .

14Recapture tax. Subtract line 13 from line 12. If zero or less, enter

on the appropriate line of your tax return (see instructions). If more than one Form 8611 is filed, add the line 14 amounts from all forms and enter the total on the appropriate line of your return. Electing large partnerships, see instructions . . . . . . . . . . . . . . . . .

15Carryforward of the

1 |

|

|

2 |

|

|

3 |

|

|

4 |

. |

|

5 |

|

|

6 |

. |

|

|

|

|

7 |

|

|

8 |

|

|

9 |

|

|

10 |

|

|

11 |

|

|

12 |

|

|

13 |

|

|

|

|

|

14 |

|

|

15 |

|

|

Only Section 42(j)(5) partnerships need to complete lines 16 and 17.

16 |

Enter interest on the line 7 recapture amount (see instructions) |

17 |

Total recapture. Add lines 7 and 16 (see instructions) |

16

17

For Paperwork Reduction Act Notice, see instructions. |

Cat. No. 63983Q |

Form 8611 (Rev. |

Form 8611 (Rev. |

Page 2 |

|

|

General Instructions

Section references are to the Internal Revenue Code.

Future Developments

For the latest information about developments related to Form 8611 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/form8611.

Purpose of Form

Use this form if you must recapture part of the

Decrease in qualified basis. The decrease may result from a change in the eligible basis or the applicable fraction. For example, a decrease in qualified basis may exist when units are not occupied by

Building dispositions. Disposing of a building or an interest therein will generate a credit recapture, unless it is reasonably expected that the building will continue to be operated as a qualified

See section 42(j) for more information.

Note. If the decrease in qualified basis is because of a change in the amount for which you are financially at risk on the building, then you must first recalculate the amount of credit taken in prior years under section 42(k) before you calculate the recapture amount on this form.

To complete this form you will need copies of the following forms that you have filed:

•Form 8586,

•Form 8609,

•Form

•Form 8611.

Note.

Recapture does not apply if:

•You disposed of the building or an ownership interest in it and you satisfy the requirements for avoiding recapture as outlined earlier under Building dispositions;

•You disposed of not more than

33 1/3% in the aggregate of your ownership interest in a building you held through a partnership, or you disposed of an ownership interest in a building you held through a partnership to which section 42(j)(5) applies or through an electing large partnership;

•The decrease in qualified basis does not exceed the additions to qualified basis for which credits were allowable in years after the year the building was placed in service; or

•The qualified basis is reduced because of a casualty loss, provided the property is restored or replaced within a reasonable period.

Recordkeeping

In order to verify changes in qualified basis from year to year, keep a copy of all Forms 8586, 8609,

Specific Instructions

Note. If recapture is passed through from a

Item F. If the building is financed with

(3)name of the issue, or if not named, other identification of the issue; and

(4)CUSIP number of the bond with the latest maturity date. If the issue does not have a CUSIP number, enter “None.”

Line 1. Enter the total credits claimed on the building for all prior years from all Forms 8586 (before reduction due to the tax liability limit) you have filed. Prior to the December 2006 revision of Form 8586, the credits (before reduction due to the tax liability limit) were reported in Part I. Do not include credits taken by a previous owner.

Line 2 Worksheet (*Line reference is to Form

a |

Enter the amount from line 10* |

b |

Multiply a by 2 |

c |

Enter the amount from line 11* |

d |

Subtract c from b |

eEnter decimal amount figured in step 1 of the instructions for line 14*. If line 14* does not apply to you,

enter

f |

Multiply d by e |

|

g |

Subtract f from d |

|

h |

Divide line 16* by line 15*. Enter the result here |

. . . . . . . . . . . . . . . . . . . |

iMultiply g by h. Enter this amount on line 2. (If more than one worksheet is completed, add the amounts

on i from all worksheets and enter the total on line 2.) . . . . . . . . . . . . . . . . .

a

b

c

d

e

f

g

h

i

Form 8611 (Rev. |

Page 3 |

|

|

Line 2. Determine the amount to enter on this line by completing a separate Line 2 Worksheet for each prior year for which line 7 of Form

Line 4. Enter the credit recapture percentage, expressed as a decimal carried to at least 3 places, from the table below:

IF the recapture |

|

THEN |

|

event occurs |

|

enter on |

|

in . . . |

|

line 4 . . . |

|

|

|

|

|

Years 2 through 11 . . . |

. |

. |

.333 |

Year 12 |

. |

. |

.267 |

Year 13 |

. |

. |

.200 |

Year 14 |

. |

. |

.133 |

Year 15 |

. |

. |

.067 |

Line 6. Enter the percentage decrease in qualified basis during the current year.

For this purpose, figure qualified basis without regard to any additions to qualified basis after the first year of the credit period. Compare any decrease in qualified basis first to additions to qualified basis. Recapture applies only if the decrease in qualified basis exceeds additions to qualified basis after the first year of the credit period.

If you disposed of the building or an ownership interest in it and did not satisfy the requirements for avoiding recapture as outlined earlier under Building dispositions, you must recapture all of the accelerated portion shown on line 5. Enter 1.000 on line 6.

Note. If the decrease causes the qualified basis to fall below the minimum

(1)(the

Line 7. If there was a prior recapture of accelerated credits on the building, do not recapture that amount again as the result of the current reduction in qualified basis. The example below demonstrates how to incorporate into the current (Year

4)recapture the first year (Year 1) accelerated portion as a result of a prior year (Year 2) recapture event.

Line 9. Figure the unused portion of the accelerated amount on line 7 by:

Step 1. Totaling the credits attributable to the building that you could not use in prior years.*

Step 2. Reducing the result of step 1 by any unused credits attributable to additions to qualified basis.

Step 3. Multiplying the result of step 2 by the decimal amount on line 4.

Step 4. Multiplying the result of step 3 by the decimal amount on line 6.

Step 5. Enter the result of step 4 on line 9.

*Generally, this is the amount of credit reported on line 1 of this Form 8611 reduced by the total low- income housing credits allowed on Form 8586 or Form 3800 for each year.

Special rule for electing large partnerships. Enter zero on line 9. An electing large partnership (defined in section 775) is treated as having fully used all prior year credits.

Line 11. Figure the interest separately for each prior tax year for which a credit is being recaptured. Interest must be figured at the overpayment rate determined under section 6621(a)(1) and compounded on a daily basis from the due date (not including extensions) of the return for the prior year until the earlier of (a) the due date (not including extensions) of the return for the recapture year, or (b) the date the return for the recapture year is filed and any income tax due for that year has been fully paid.

Tables of interest factors to figure daily compound interest were published in Rev. Proc.

(1)in the revenue rulings published quarterly in the Internal Revenue Bulletin.

Note. If the line 8 recapture amount is from a section 42(j)(5) partnership, the partnership will figure the interest and include it in the recapture amount reported to you. Enter

Line 13. Subtract the amount on line 9 from the total of all prior year unused credits attributable to the building (Step 1 of the line 9 instruction above). Enter the result on line 13.

Line 14. For information on how to report the recapture tax on Form 1040, see the instructions for line 60 (other taxes) in the Instructions for Form 1040. Form 1120 filers report the recapture tax on Form 1120, Schedule J, line 9b.

Special rule for electing large partnerships. Subtract the credit shown on Form 8586 from the total of the line

14 amounts from all Forms 8611. Enter the result (but not less than zero) on Form

Note. You must also reduce the current year

Line 15. Carry forward the

Line 7— Example. $2,700 of accelerated portion of

|

Year 1 |

Year 2 |

Year 3 |

Year 4* |

$270 |

$216 ($270 × .8 (20% |

$270 |

$189 ($270 × .7 (30% |

|

credit |

|

reduction in qualified |

|

reduction in qualified |

|

|

basis)) |

|

basis)) |

|

|

|

|

|

Recapture of Year 1 |

|

$18 ($270 × .333 × .2 |

|

$9 ($27 ($270 × .333 × |

|

(20% reduction in |

|

.3 (30% reduction in |

|

credit |

|

qualified basis)) |

|

qualified basis) minus |

|

|

|

|

$18 Year 2 recapture)) |

|

|

|

|

|

* You will have to complete the rest of the form to figure the recapture as the result of the current year reduction in basis as it affects the Year 2 and Year 3 credit.

Form 8611 (Rev. |

Page 4 |

|

|

Lines 16 and 17. Only section 42(j)(5) partnerships complete these lines. This is a partnership (other than an electing large partnership) that has at least 35 partners, unless the partnership elects (or has previously elected) not to be treated as a section 42(j)(5) partnership. For purposes of this definition, an individual and his or her spouse (and their estates) are treated as one partner.

For purposes of determining the credit recapture amount, a section 42(j)(5) partnership is treated as the taxpayer to which the

See the instructions for line 11 to figure the interest on line 16. The partnership must attach Form 8611 to its Form 1065 and allocate this amount to each partner on Schedule

partnership’s taxable income is allocated to each partner.

Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to give us the information. We need it to ensure that you are complying with these laws and to allow us to figure and collect the right amount of tax.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete and file this form will vary depending on individual circumstances. The estimated burden for individual taxpayers filing this form is approved under OMB control number

Recordkeeping . . . . 8 hr., 21 min.

Learning about the

law or the form . . . . . . . 1 hr.

Preparing and sending

the form to the IRS . . 1 hr., 10 min.

If you have comments concerning the accuracy of these time estimates or suggestions for making this form simpler, we would be happy to hear from you. You can write to the IRS at the address listed in the instructions for the tax return with which this form is filed.