Once you open the online editor for PDFs by FormsPal, you may fill out or change Form 8835 right here. FormsPal expert team is ceaselessly working to improve the tool and make it even faster for clients with its extensive features. Enjoy an ever-improving experience now! Here is what you'll need to do to get started:

Step 1: Just press the "Get Form Button" above on this page to access our pdf editing tool. Here you'll find everything that is needed to work with your document.

Step 2: With this handy PDF editing tool, you can actually do more than simply fill out blank form fields. Edit away and make your forms seem sublime with custom text incorporated, or modify the original content to excellence - all comes along with an ability to incorporate almost any images and sign it off.

With regards to the fields of this particular form, here's what you should know:

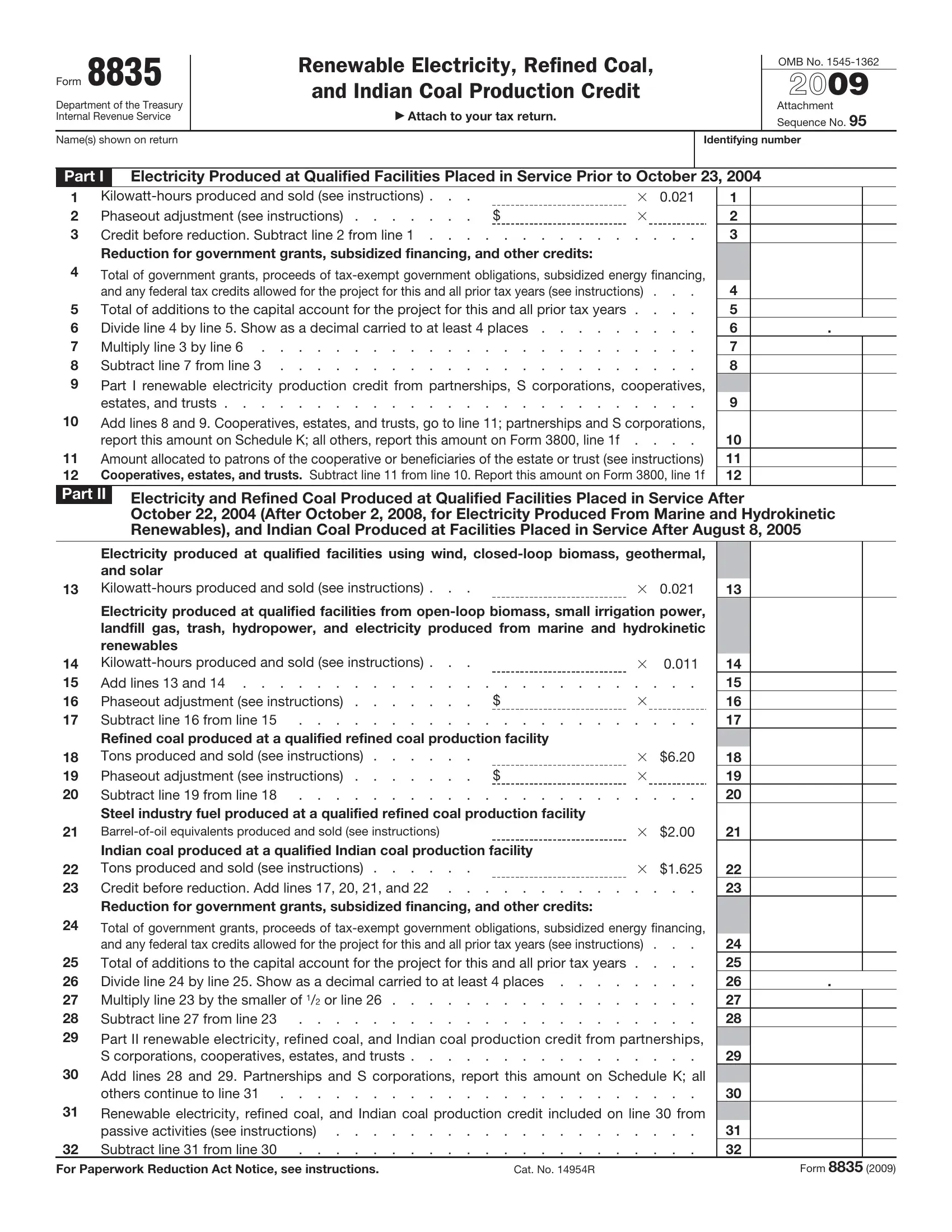

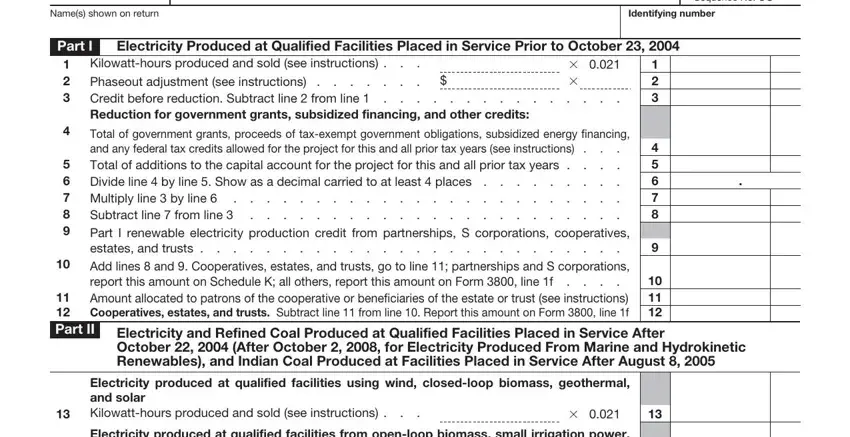

1. The Form 8835 requires particular information to be typed in. Ensure the subsequent blanks are complete:

2. Once this part is complete, you'll want to include the essential specifics in Electricity produced at qualified, Indian coal produced at a, Total of government grants, Multiply line by the smaller, and Subtract line from line Part II so that you can move forward further.

As to Subtract line from line Part II and Indian coal produced at a, make certain you take a second look in this current part. The two of these are the most significant fields in this document.

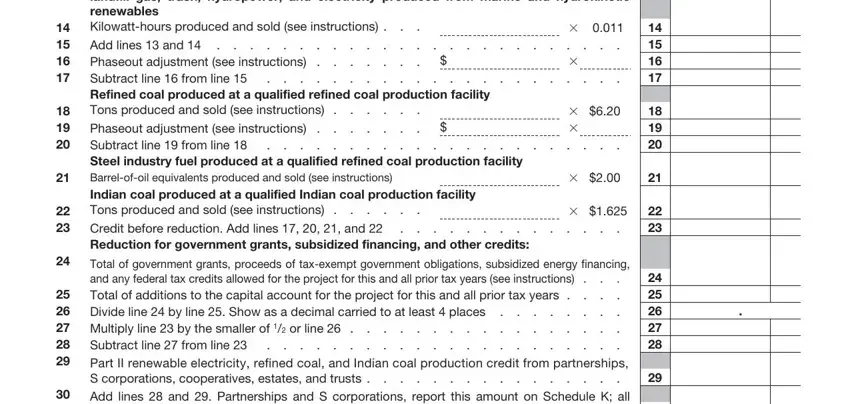

3. Your next part is hassle-free - fill in all of the blanks in Subtract line from line Part II, For Paperwork Reduction Act, Cat No R, and Form in order to finish this part.

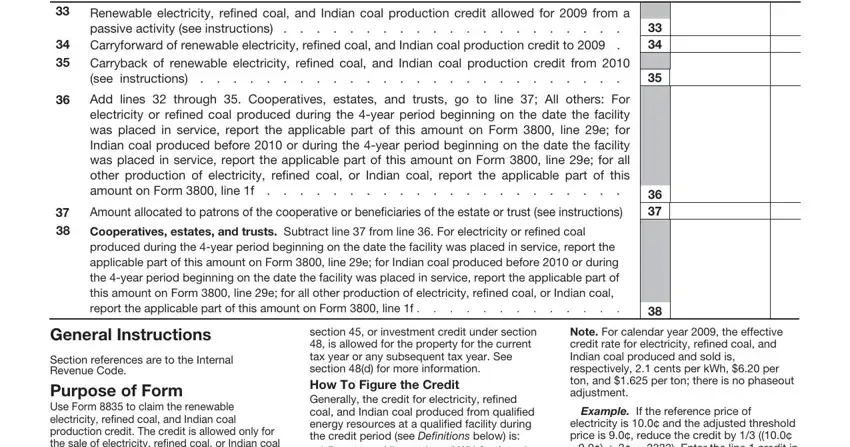

4. It is time to proceed to the next section! Here you'll have these Page, Renewable electricity refined coal, Add lines through Cooperatives, Amount allocated to patrons of the, Cooperatives estates and trusts, General Instructions, Section references are to the, section or investment credit, Note For calendar year the, Example If the reference price of, and electricity is and the adjusted blank fields to do.

Step 3: Immediately after looking through the form fields you have filled out, click "Done" and you are all set! After starting a7-day free trial account with us, you'll be able to download Form 8835 or email it immediately. The form will also be readily available through your personal account menu with your each and every edit. FormsPal is invested in the personal privacy of our users; we make sure all information put into our tool continues to be protected.