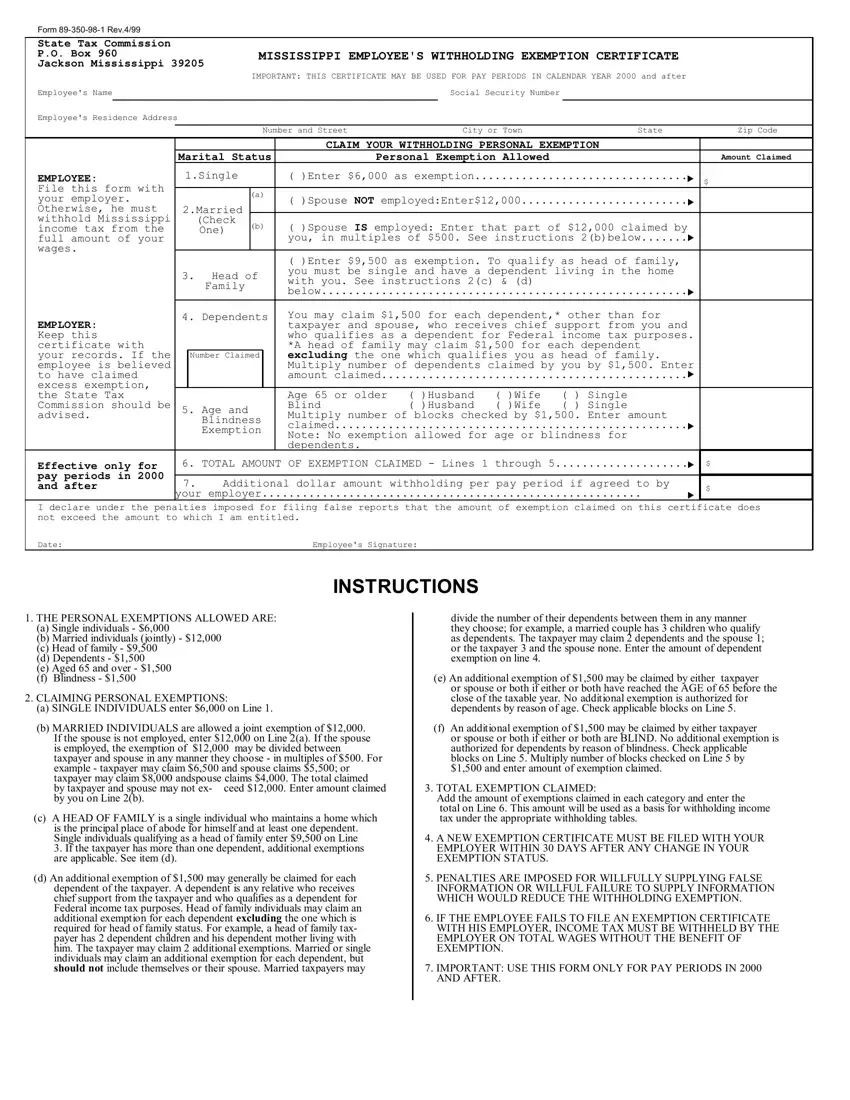

The Form 89-350-98-1, recognized as the Mississippi Employee's Withholding Exemption Certificate, serves as a crucial document for both employees and employers within the state. Revised in April 1999 and applicable for pay periods in the calendar year 2000 and beyond, this form plays a pivotal role in determining the amount of Mississippi state income tax to be withheld from an employee's wages. Through this form, individuals provide essential information, including their name, social security number, address, and details regarding their marital status and number of dependents. A distinctive feature of this certificate is its allowance for personal exemptions, varying for single individuals, married couples, heads of families, and additional exemptions for dependents, the elderly, and the blind. Employees are guided on how to calculate the exemptions they’re entitled to, with specific instructions for different categories such as marital status and age. This certification not only facilitates the accurate withholding of taxes, ensuring compliance with state tax regulations but also highlights the responsibilities of employers in retaining these certificates and the implications for employees who fail to submit one. Additionally, the form underscores the penalties associated with providing false information or omitting information that results in an incorrect withholding amount. The structured process outlined encourages both employees and employers to closely adhere to these guidelines to ensure the smooth operation of state tax withholding practices.

| Question | Answer |

|---|---|

| Form Name | Form 89 350 98 1 |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | Mississippi, false, multiples, online form 89 350 |