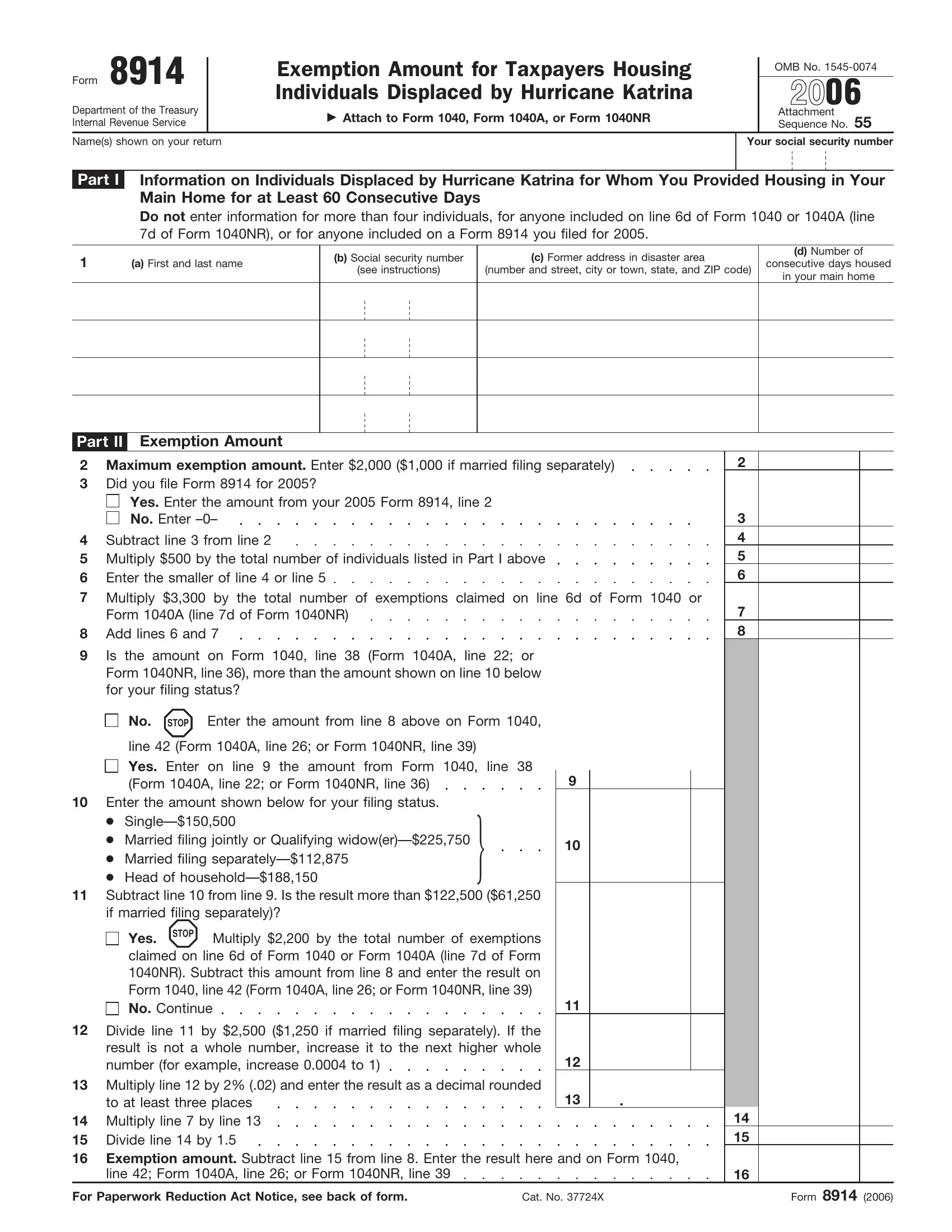

In the aftermath of Hurricane Katrina, a natural catastrophe that left untold devastation across multiple states, the Internal Revenue Service introduced Form 8914, a critical document designed to provide tax relief to those who opened their homes to individuals displaced by this unprecedented disaster. At its core, Form 8914, titled "Exemption Amount for Taxpayers Housing Individuals Displaced by Hurricane Katrina," offers a financial incentive in the form of an additional exemption amount for taxpayers who provided housing to displaced individuals in their main home for a minimum of 60 consecutive days. This provision underlines the government's commitment to supporting both the victims of the disaster and those who extended their generosity and resources to accommodate them. The form sets out clear guidelines regarding eligibility and the calculation of the exemption amount, capped at $2,000 ($1,000 if married filing separately), with adjustments based on the number of individuals housed and conditions established to ensure that only genuine cases are rewarded. Further unique stipulations include restrictions on claiming these exemptions for dependents or spouses and allowances for shared housing situations, making it essential for taxpayers to navigate the specifics of Form 8914 with great care. This initiative not only demonstrates a structured approach to post-disaster recovery but also fosters a culture of community support and resilience, amplifying the role of individual citizens in the nation's collective response to emergency situations.

| Question | Answer |

|---|---|

| Form Name | Form 8914 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | f8914 2006 irs form 8914 |