Form 8951 can be completed effortlessly. Simply make use of FormsPal PDF editing tool to get it done in a timely fashion. To maintain our editor on the forefront of practicality, we strive to integrate user-oriented capabilities and enhancements regularly. We're always happy to receive suggestions - join us in reshaping the way you work with PDF forms. Here is what you'll have to do to start:

Step 1: Open the PDF file in our editor by pressing the "Get Form Button" above on this page.

Step 2: Using this advanced PDF editing tool, it's possible to accomplish more than simply complete forms. Edit away and make your forms look professional with custom textual content put in, or modify the file's original content to perfection - all supported by the capability to add stunning photos and sign the PDF off.

This PDF doc will need some specific details; to guarantee accuracy, be sure to bear in mind the next guidelines:

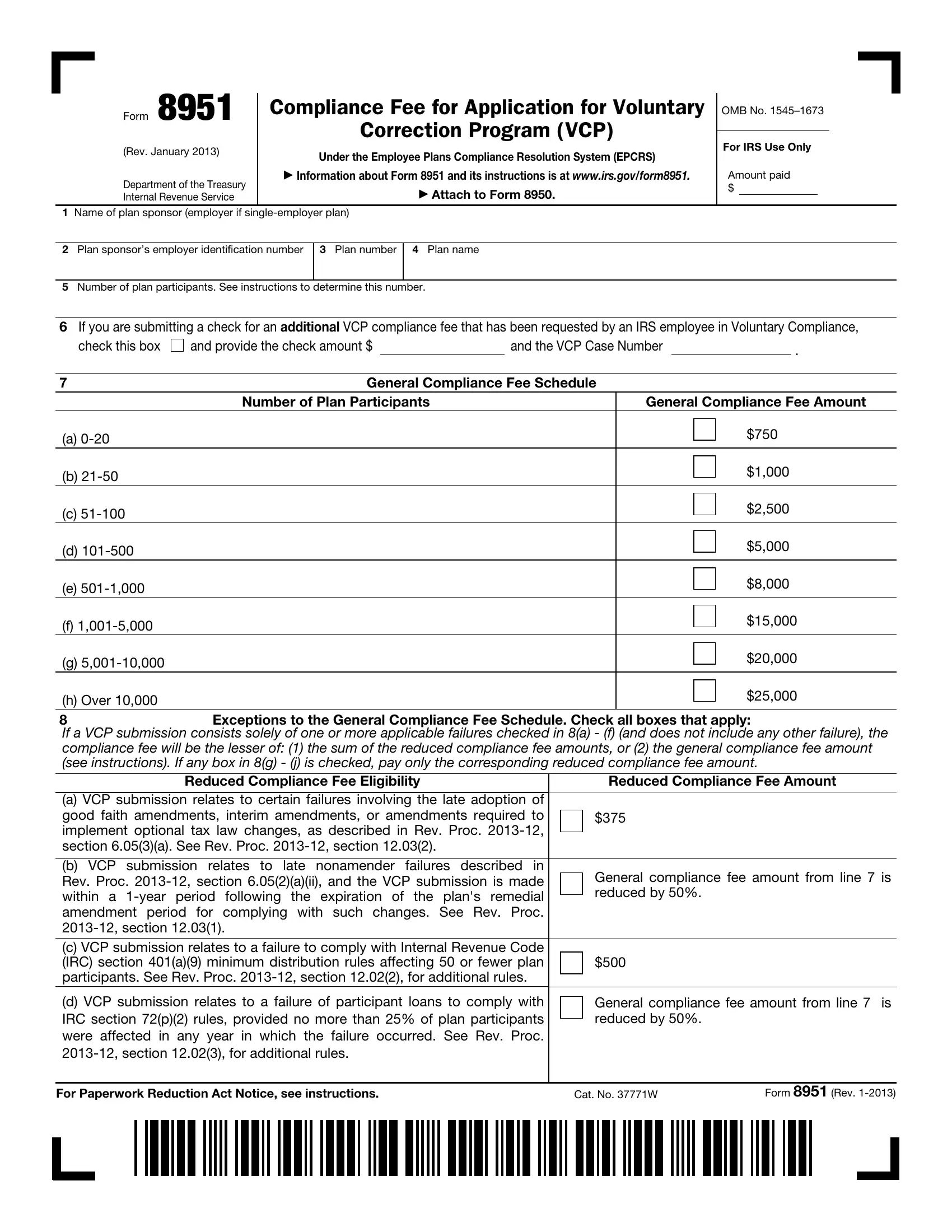

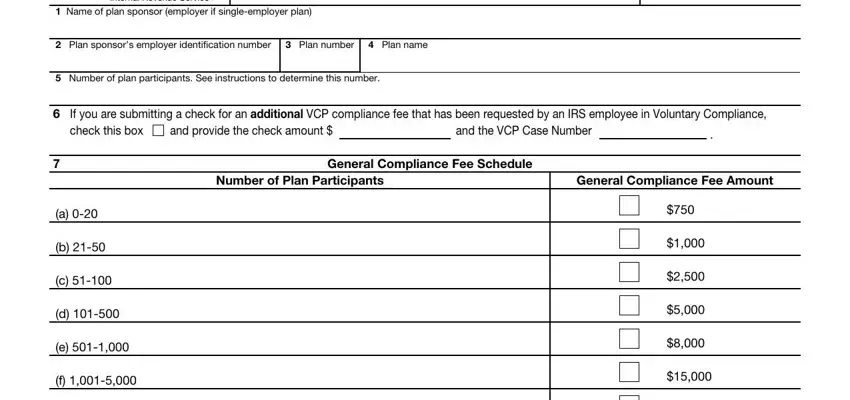

1. Whenever submitting the Form 8951, make sure to complete all essential blanks within the relevant form section. It will help expedite the work, making it possible for your information to be processed promptly and correctly.

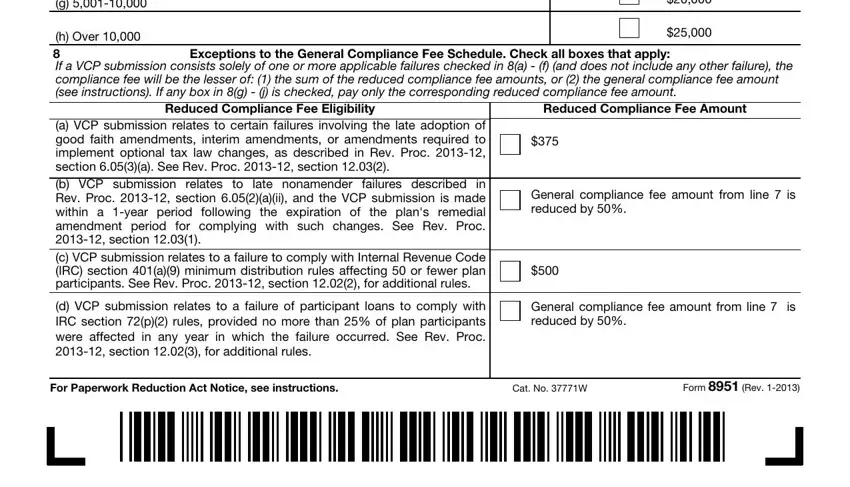

2. Right after the last section is filled out, go on to type in the applicable information in all these - h Over If a VCP submission, Exceptions to the General, Reduced Compliance Fee Eligibility, Reduced Compliance Fee Amount, a VCP submission relates to, d VCP submission relates to a, General compliance fee amount from, General compliance fee amount from, For Paperwork Reduction Act Notice, Cat No W, and Form Rev.

Be really careful when filling out a VCP submission relates to and Form Rev, because this is the part where most users make some mistakes.

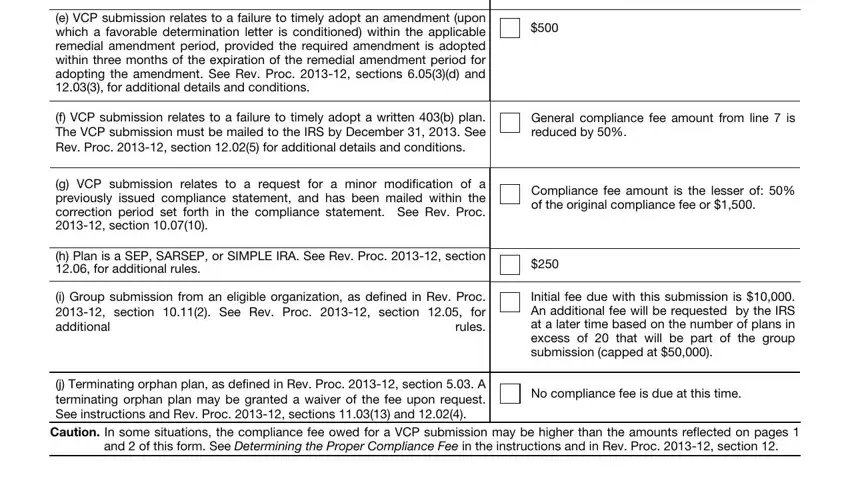

3. This third part is typically quite simple, e VCP submission relates to a, f VCP submission relates to a, General compliance fee amount from, g VCP submission relates to a, Compliance fee amount is the, h Plan is a SEP SARSEP or SIMPLE, i Group submission from an, Initial fee due with this, j Terminating orphan plan as, No compliance fee is due at this, and and of this form See Determining - all of these blanks needs to be completed here.

Step 3: Proofread the details you've inserted in the blank fields and then click on the "Done" button. Make a free trial subscription at FormsPal and acquire immediate access to Form 8951 - downloadable, emailable, and editable in your FormsPal cabinet. When you use FormsPal, you can certainly complete documents without the need to be concerned about data incidents or entries being shared. Our protected software ensures that your personal information is stored safely.