This form is available electronically.

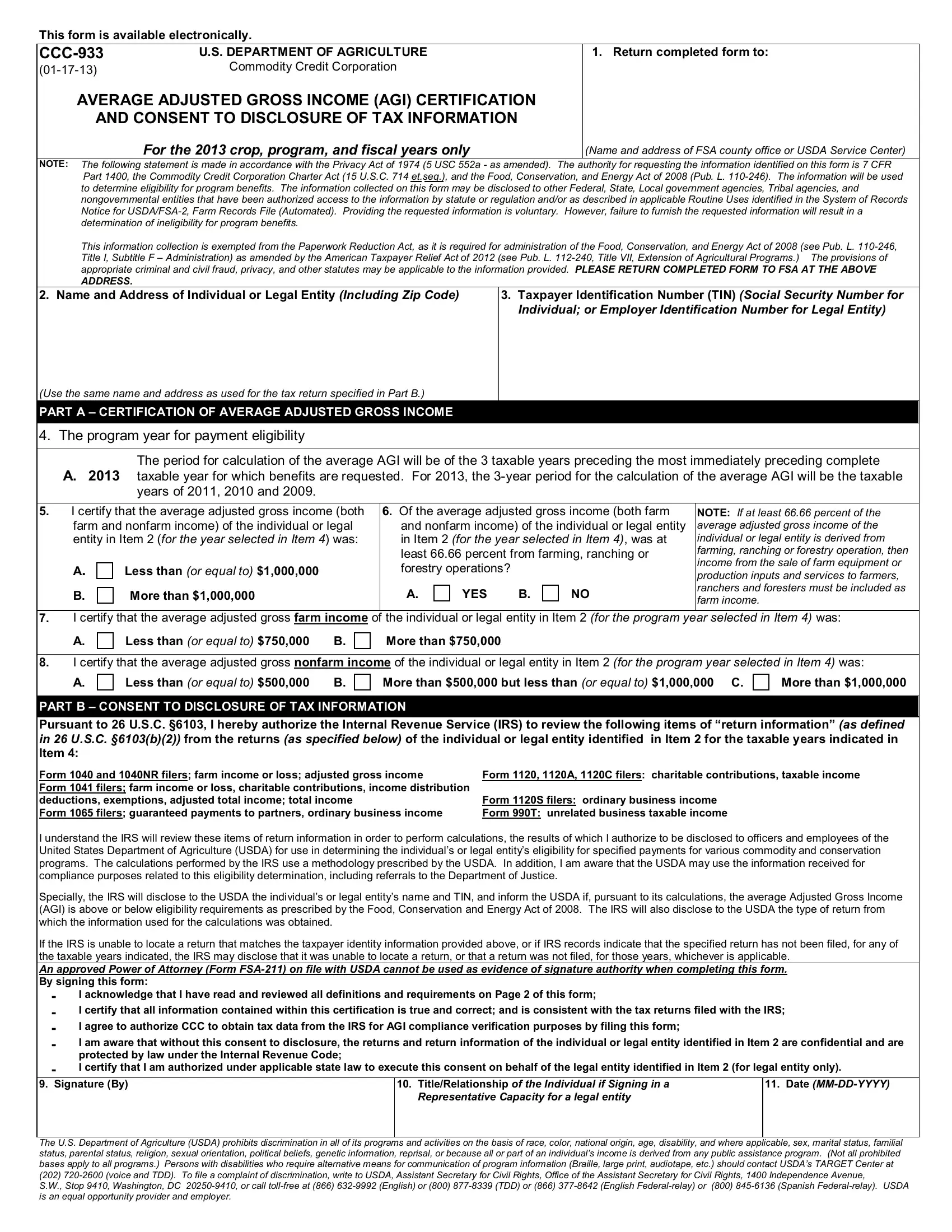

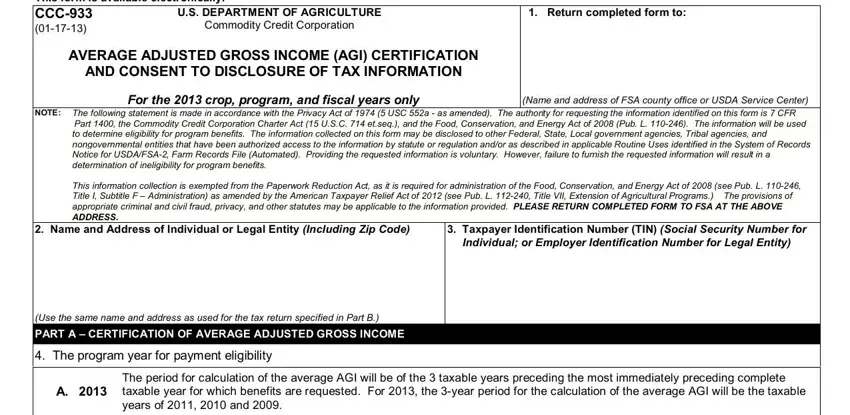

CCC-933 |

U.S. DEPARTMENT OF AGRICULTURE |

1. Return completed form to: |

(01-17-13) |

Commodity Credit Corporation |

|

|

|

AVERAGE ADJUSTED GROSS INCOME (AGI) CERTIFICATION |

|

AND CONSENT TO DISCLOSURE OF TAX INFORMATION |

|

|

For the 2013 crop, program, and fiscal years only |

(Name and address of FSA county office or USDA Service Center) |

NOTE: The following statement is made in accordance with the Privacy Act of 1974 (5 USC 552a - as amended). The authority for requesting the information identified on this form is 7 CFR Part 1400, the Commodity Credit Corporation Charter Act (15 U.S.C. 714 et.seq.), and the Food, Conservation, and Energy Act of 2008 (Pub. L. 110-246). The information will be used to determine eligibility for program benefits. The information collected on this form may be disclosed to other Federal, State, Local government agencies, Tribal agencies, and nongovernmental entities that have been authorized access to the information by statute or regulation and/or as described in applicable Routine Uses identified in the System of Records Notice for USDA/FSA-2, Farm Records File (Automated). Providing the requested information is voluntary. However, failure to furnish the requested information will result in a determination of ineligibility for program benefits.

This information collection is exempted from the Paperwork Reduction Act, as it is required for administration of the Food, Conservation, and Energy Act of 2008 (see Pub. L. 110-246, Title I, Subtitle F – Administration) as amended by the American Taxpayer Relief Act of 2012 (see Pub. L. 112-240, Title VII, Extension of Agricultural Programs.) The provisions of appropriate criminal and civil fraud, privacy, and other statutes may be applicable to the information provided. PLEASE RETURN COMPLETED FORM TO FSA AT THE ABOVE

ADDRESS.

2. |

Name and Address of Individual or Legal Entity (Including Zip Code) |

|

3. Taxpayer Identification Number (TIN) (Social Security Number for |

|

|

|

|

|

|

|

Individual; or Employer Identification Number for Legal Entity) |

|

(Use the same name and address as used for the tax return specified in Part B.) |

|

|

|

|

|

|

PART A – CERTIFICATION OF AVERAGE ADJUSTED GROSS INCOME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. The program year for payment eligibility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The period for calculation of the average AGI will be of the 3 taxable years preceding the most immediately preceding complete |

|

|

A. 2013 taxable year for which benefits are requested. For 2013, the 3-year period for the calculation of the average AGI will be the taxable |

|

|

|

years of 2011, 2010 and 2009. |

|

|

|

|

|

|

|

|

|

|

|

5. |

I certify that the average adjusted gross income (both |

6. Of the average adjusted gross income (both farm |

NOTE: If at least 66.66 percent of the |

|

|

farm and nonfarm income) of the individual or legal |

and nonfarm income) of the individual or legal entity |

average adjusted gross income of the |

|

|

entity in Item 2 (for the year selected in Item 4) was: |

in Item 2 (for the year selected in Item 4), was at |

individual or legal entity is derived from |

|

|

|

|

|

least 66.66 percent from farming, ranching or |

farming, ranching or forestry operation, then |

|

|

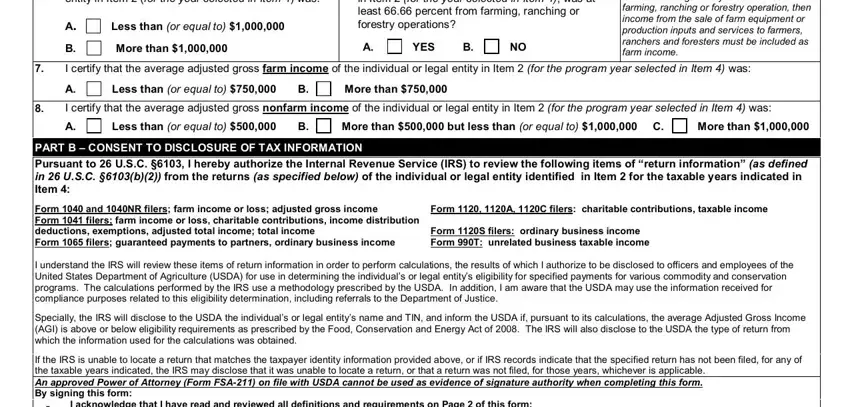

A. |

Less than (or equal to) $1,000,000 |

|

forestry operations? |

|

income from the sale of farm equipment or |

|

|

|

|

production inputs and services to farmers, |

|

|

|

|

|

|

|

|

|

|

|

B. |

More than $1,000,000 |

|

A. |

YES |

B. |

NO |

ranchers and foresters must be included as |

|

|

|

farm income. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

I certify that the average adjusted gross farm income of the individual or legal entity in Item 2 (for the program year selected in Item 4) was: |

|

|

A. |

Less than (or equal to) $750,000 |

B. |

More than $750,000 |

|

|

|

|

|

|

8. |

I certify that the average adjusted gross nonfarm income of the individual or legal entity in Item 2 (for the program year selected in Item 4) was: |

|

|

A. |

Less than (or equal to) $500,000 |

B. |

More than $500,000 but less than (or equal to) $1,000,000 C. |

More than $1,000,000 |

PART B – CONSENT TO DISCLOSURE OF TAX INFORMATION

Pursuant to 26 U.S.C. §6103, I hereby authorize the Internal Revenue Service (IRS) to review the following items of “return information” (as defined in 26 U.S.C. §6103(b)(2)) from the returns (as specified below) of the individual or legal entity identified in Item 2 for the taxable years indicated in Item 4:

Form 1040 and 1040NR filers; farm income or loss; adjusted gross income |

Form 1120, 1120A, 1120C filers: charitable contributions, taxable income |

Form 1041 filers; farm income or loss, charitable contributions, income distribution |

|

deductions, exemptions, adjusted total income; total income |

Form 1120S filers: ordinary business income |

Form 1065 filers; guaranteed payments to partners, ordinary business income |

Form 990T: unrelated business taxable income |

I understand the IRS will review these items of return information in order to perform calculations, the results of which I authorize to be disclosed to officers and employees of the United States Department of Agriculture (USDA) for use in determining the individual’s or legal entity’s eligibility for specified payments for various commodity and conservation programs. The calculations performed by the IRS use a methodology prescribed by the USDA. In addition, I am aware that the USDA may use the information received for compliance purposes related to this eligibility determination, including referrals to the Department of Justice.

Specially, the IRS will disclose to the USDA the individual’s or legal entity’s name and TIN, and inform the USDA if, pursuant to its calculations, the average Adjusted Gross Income (AGI) is above or below eligibility requirements as prescribed by the Food, Conservation and Energy Act of 2008. The IRS will also disclose to the USDA the type of return from which the information used for the calculations was obtained.

If the IRS is unable to locate a return that matches the taxpayer identity information provided above, or if IRS records indicate that the specified return has not been filed, for any of the taxable years indicated, the IRS may disclose that it was unable to locate a return, or that a return was not filed, for those years, whichever is applicable.

An approved Power of Attorney (Form FSA-211) on file with USDA cannot be used as evidence of signature authority when completing this form. By signing this form:

- |

I acknowledge that I have read and reviewed all definitions and requirements on Page 2 of this form; |

|

- |

I certify that all information contained within this certification is true and correct; and is consistent with the tax returns filed with the IRS; |

- |

I agree to authorize CCC to obtain tax data from the IRS for AGI compliance verification purposes by filing this form; |

|

- |

I am aware that without this consent to disclosure, the returns and return information of the individual or legal entity identified in Item 2 are confidential and are |

|

protected by law under the Internal Revenue Code; |

|

|

- |

I certify that I am authorized under applicable state law to execute this consent on behalf of the legal entity identified in Item 2 (for legal entity only). |

9. Signature (By) |

10. Title/Relationship of the Individual if Signing in a |

11. Date (MM-DD-YYYY) |

|

|

Representative Capacity for a legal entity |

|

|

|

|

|

The U.S. Department of Agriculture (USDA) prohibits discrimination in all of its programs and activities on the basis of race, color, national origin, age, disability, and where applicable, sex, marital status, familial status, parental status, religion, sexual orientation, political beliefs, genetic information, reprisal, or because all or part of an individual’s income is derived from any public assistance program. (Not all prohibited bases apply to all programs.) Persons with disabilities who require alternative means for communication of program information (Braille, large print, audiotape, etc.) should contact USDA’s TARGET Center at (202) 720-2600 (voice and TDD). To file a complaint of discrimination, write to USDA, Assistant Secretary for Civil Rights, Office of the Assistant Secretary for Civil Rights, 1400 Independence Avenue,

S.W., Stop 9410, Washington, DC 20250-9410, or call toll-free at (866) 632-9992 (English) or (800) 877-8339 (TDD) or (866) 377-8642 (English Federal-relay) or (800) 845-6136 (Spanish Federal-relay). USDA is an equal opportunity provider and employer.

CCC-933 (01-17-13) |

Page 2 of 2 |

GENERAL INFORMATION ON AVERAGE ADJUSTED GROSS INCOME – PART A

Individuals or legal entities that receive benefits under most commodity and conservation programs administered by CCC cannot have incomes that exceed certain limits set by law. For entities, both the entity itself, and its members cannot exceed the income limitations. If a member, whether an individual or an entity, of an entity exceeds the limitations, payments to that entity will be commensurately reduced according to that member’s direct or indirect ownership share in the entity. (All members of the entity must also submit this form to verify income limitations are met.)

Adjusted Gross Income is the individual’s or legal entity’s IRS-reported adjusted gross income consisting of both farm and nonfarm income. A three year average of that income will be computed for the three years of the relevant base period identified on the first page of this form to determine eligibility for the applicable program year. Individuals or legal entities with average adjusted gross income greater than $1 million shall be ineligible for direct payments under the Direct and Counter-cyclical Program

Adjusted Gross Farm Income is the part of the yearly adjusted gross income that is farm income. The amount is computed separately for each year and then averaged. Farm income means income related to the following: production of crops, livestock, fish and aquaculture for food; the feeding and rearing of livestock; products produced or derived from livestock; production of specialty crops and unfinished raw forestry products; processing packing, storing and transporting farm, ranch and forestry commodities including renewable energy; production of farm-based renewable energy; the sale of land used for agriculture; sale of land or sale of easements and development rights to agricultural land, water and hunting rights, and environmental benefits; rental or lease of land or equipment used in farming, ranching, forestry operation; payments and benefits from risk management practices, crop insurance indemnities, catastrophic risk protection plans, conservation program and government farm program payments. Individuals or legal entities with average adjusted gross farm income greater than $750,000 shall be ineligible for direct payments under the Direct and Counter-cyclical Program

Adjusted Gross Nonfarm Income is the difference for the year between the filer’s adjusted gross income and the filer’s adjusted gross farm income. The difference is computed separately for each year and then averaged. Individuals or legal entities with average adjusted gross nonfarm income that exceeds $500,000 shall be ineligible for commodity program payments, price support benefits, disaster assistance programs, and for the Milk Income Loss Compensation Program. Additionally, individuals or legal entities with average adjusted gross nonfarm income exceeding $1 million will be ineligible for new contracts or participation in conservation programs after October 1, 2008, unless at least 66.66% of their total average adjusted gross income (sum of farm and nonfarm income) is generated from activities related to farming.

HOW TO DETERMINE ADJUSTED GROSS INCOME

Individual – Internal Revenue Service (IRS) Form 1040 filers, specific lines on that form represent the adjusted gross income and the income from farming, ranching, or forestry operations.

Trust or Estate – the adjusted gross income is the total income and charitable contributions reported to IRS.

Corporation – the adjusted gross income is the total of the final taxable income and any charitable contributions reported to IRS.

Limited Partnership (LP), Limited Liability Company (LLC), Limited Liability Partnership (LLP) or Similar Entity – the adjusted gross income is the total income from trade or business activities plus guaranteed payments to the members as reported to the IRS.

Tax-exempt Organization – the adjusted gross income is the unrelated business taxable income excluding any income from non-commercial activities as reported to the IRS.

GENERAL INFORMATION ON CONSENT TO DISCLOSURE OF TAX INFORMATION – PART B

This consent allows IRS’s access to, and use of, certain items of return information to perform calculations, using a methodology prescribed by the USDA, that will assist USDA in its verification of a program participant’s compliance with the adjusted gross income (AGI) limitations necessary for participation in, and receipt of, commodity, conservation, price support or disaster program benefits. This consent also permits the USDA to receive certain items of return information for its eligibility determination.

This consent authorizes the disclosure of these items of return information for only the time period specified. Each item of information requested on this form is needed for the IRS to (1) locate, and verify, your tax information; (2) perform the requisite Average AGI calculations; and (3) provide the USDA with the legal entity’s name and Taxpayer Identification Number (TIN), the type of return from which the specified items were located for use in the calculation, and whether or not the average AGI is above or below eligibility requirements. The IRS will not provide the USDA with any of the items specified on this consent form that it uses to perform the calculations or the average AGI figure.

This form can only be signed by the person authorized under state law to sign this consent for the legal entity identified in Item 2. An approved Power of Attorney (Form FSA-211) on file with USDA cannot be used as evidence of signature authority when completing this form.

|

|

|

INSTRUCTIONS FOR COMPLETION OF CCC-933 |

|

|

|

|

|

Item No./Field name |

|

Instruction |

|

|

|

|

1. |

Return Completed Form To |

|

Enter the name and address of the FSA county office or USDA service center where the completed CCC-933 will be submitted. |

|

|

|

|

2. |

Person or Legal Entity’s |

|

Enter the person’s or legal entity’s name and address for commodity, conservation, price support, or disaster program benefits. |

|

Name and Address |

|

Enter the name and address as it appeared on the IRS tax returns filed for the taxable years specified in Item 4. |

|

|

|

|

3. |

Taxpayer Identification |

|

In the format provided, enter the complete taxpayer identification number of the person or legal entity identified in Item 2. This will |

|

Number |

|

be either a Social Security Number or Taxpayer Identification Number. |

|

|

|

|

|

|

|

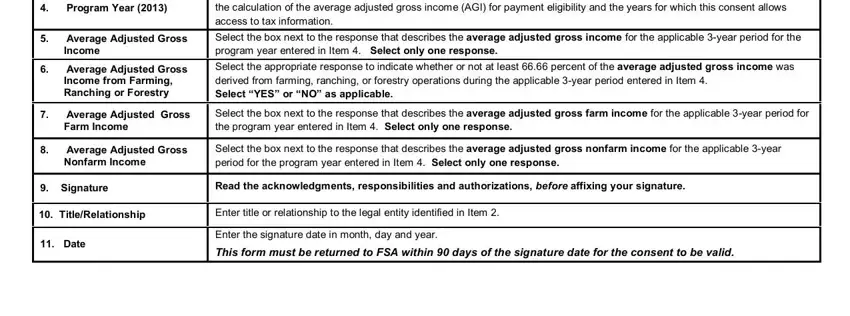

The year for which program benefits are being requested is 2013 only. The program year determines the 3-year period used for |

4. |

Program Year (2013) |

|

the calculation of the average adjusted gross income (AGI) for payment eligibility and the years for which this consent allows |

|

|

|

access to tax information. |

|

|

|

|

5. |

Average Adjusted Gross |

|

Select the box next to the response that describes the average adjusted gross income for the applicable 3-year period for the |

|

Income |

|

program year entered in Item 4. Select only one response. |

|

|

|

|

6. |

Average Adjusted Gross |

|

Select the appropriate response to indicate whether or not at least 66.66 percent of the average adjusted gross income was |

|

|

|

Income from Farming, |

|

derived from farming, ranching, or forestry operations during the applicable 3-year period entered in Item 4. |

|

Ranching or Forestry |

|

Select “YES” or “NO” as applicable. |

7. |

Average Adjusted Gross |

|

Select the box next to the response that describes the average adjusted gross farm income for the applicable 3-year period for |

|

Farm Income |

|

the program year entered in Item 4. Select only one response. |

|

|

|

|

8. |

Average Adjusted Gross |

|

Select the box next to the response that describes the average adjusted gross nonfarm income for the applicable 3-year |

|

Nonfarm Income |

|

period for the program year entered in Item 4. Select only one response. |

|

|

|

|

9. |

Signature |

|

Read the acknowledgments, responsibilities and authorizations, before affixing your signature. |

|

|

|

|

10. |

Title/Relationship |

|

Enter title or relationship to the legal entity identified in Item 2. |

|

|

|

|

11. |

Date |

|

Enter the signature date in month, day and year. |

|

This form must be returned to FSA within 90 days of the signature date for the consent to be valid. |

|

|

|

|

|

|

|