B240A (Form B240A) (04/10)

Check one.

’ Presumption of Undue Hardship

’ No Presumption of Undue Hardship

See Debtor’s Statement in Support of Reaffirmation,

Part II below, to determine which box to check.

UNITED STATES BANKRUPTCY COURT

__________ District of __________

In re |

, |

Case No. |

|

Debtor |

|

|

|

|

|

Chapter |

REAFFIRMATION DOCUMENTS

Name of Creditor: ______________________________________

’ Check this box if Creditor is a Credit Union

PART I. REAFFIRMATION AGREEMENT

Reaffirming a debt is a serious financial decision. Before entering into this Reaffirmation Agreement, you must review the important disclosures, instructions, and definitions found in Part V of this form.

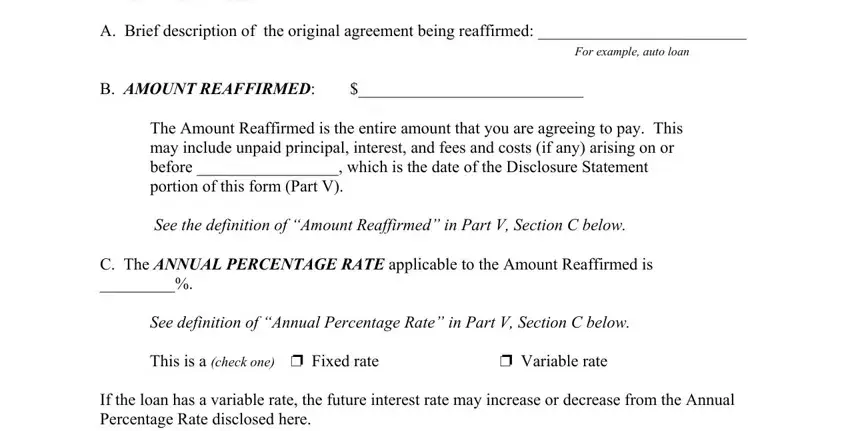

A. Brief description of the original agreement being reaffirmed: _________________________

|

For example, auto loan |

B. AMOUNT REAFFIRMED: |

$___________________________ |

The Amount Reaffirmed is the entire amount that you are agreeing to pay. This may include unpaid principal, interest, and fees and costs (if any) arising on or before _________________, which is the date of the Disclosure Statement

portion of this form (Part V).

See the definition of “Amount Reaffirmed” in Part V, Section C below.

C.The ANNUAL PERCENTAGE RATE applicable to the Amount Reaffirmed is

_________%.

See definition of “Annual Percentage Rate” in Part V, Section C below.

This is a (check one) ’ Fixed rate |

’ Variable rate |

If the loan has a variable rate, the future interest rate may increase or decrease from the Annual Percentage Rate disclosed here.

D. Reaffirmation Agreement Repayment Terms (check and complete one):

B240A, Reaffirmation Documents |

Page 2 |

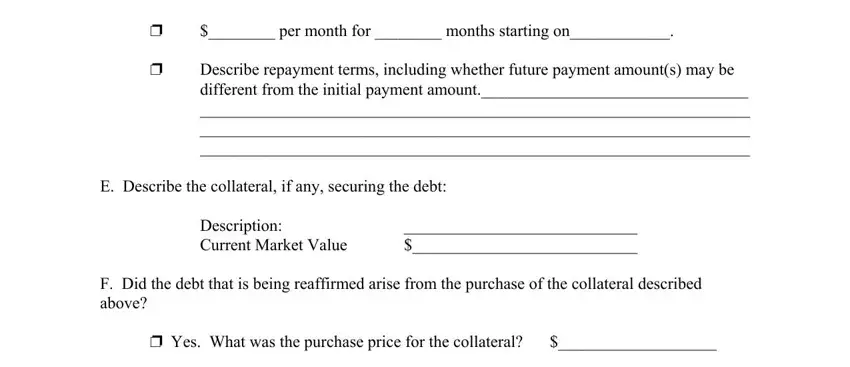

’$________ per month for ________ months starting on____________.

’Describe repayment terms, including whether future payment amount(s) may be different from the initial payment amount.________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

E.Describe the collateral, if any, securing the debt:

Description: |

____________________________ |

Current Market Value |

$___________________________ |

F.Did the debt that is being reaffirmed arise from the purchase of the collateral described above?

’ Yes. |

What was the purchase price for the collateral? |

$___________________ |

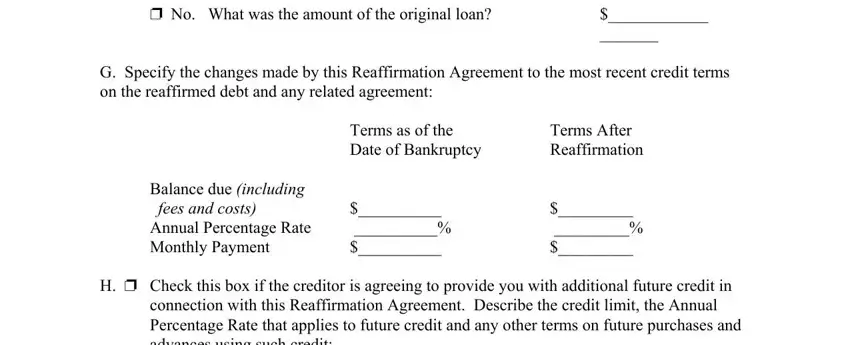

’ No. |

What was the amount of the original loan? |

$____________ |

|

|

_______ |

G.Specify the changes made by this Reaffirmation Agreement to the most recent credit terms on the reaffirmed debt and any related agreement:

|

Terms as of the |

Terms After |

|

Date of Bankruptcy |

Reaffirmation |

Balance due (including |

|

|

fees and costs) |

$__________ |

$_________ |

Annual Percentage Rate |

__________% |

_________% |

Monthly Payment |

$__________ |

$_________ |

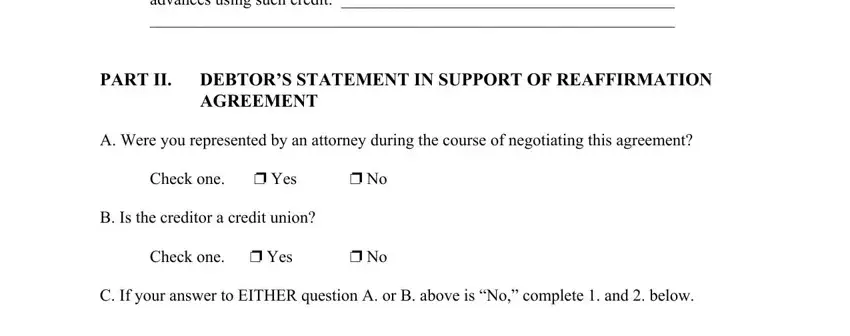

H.’ Check this box if the creditor is agreeing to provide you with additional future credit in connection with this Reaffirmation Agreement. Describe the credit limit, the Annual Percentage Rate that applies to future credit and any other terms on future purchases and advances using such credit: ________________________________________

_______________________________________________________________

PART II. DEBTOR’S STATEMENT IN SUPPORT OF REAFFIRMATION AGREEMENT

A. Were you represented by an attorney during the course of negotiating this agreement?

Check one. |

’ Yes |

’ No |

B. Is the creditor a credit union? |

|

Check one. |

’ Yes |

’ No |

C. If your answer to EITHER question A. or B. above is “No,” complete 1. and 2. below.

B240A, Reaffirmation Documents |

Page 3 |

1. Your present monthly income and expenses are: |

|

a. Monthly income from all sources after payroll deductions |

|

(take-home pay plus any other income) |

$_________ |

b. Monthly expenses (including all reaffirmed debts except |

|

this one) |

$_________ |

c. Amount available to pay this reaffirmed debt (subtract b. from a.) |

$_________ |

d. Amount of monthly payment required for this reaffirmed debt |

$_________ |

If the monthly payment on this reaffirmed debt (line d.) is greater than the amount you have available to pay this reaffirmed debt (line c.), you must check the box at the top of page one that says “Presumption of Undue Hardship.” Otherwise, you must check the box at the top of page one that says “No Presumption of Undue Hardship.”

2.You believe that this reaffirmation agreement will not impose an undue hardship on you or your dependents because:

Check one of the two statements below, if applicable:

’You can afford to make the payments on the reaffirmed debt because your monthly income is greater than your monthly expenses even after you include in your expenses the monthly payments on all debts you are reaffirming, including this one.

’You can afford to make the payments on the reaffirmed debt even though your monthly income is less than your monthly expenses after you include in your expenses the monthly payments on all debts you are reaffirming, including this one, because:

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

Use an additional page if needed for a full explanation.

D. If your answers to BOTH questions A. and B. above were “Yes,” check the following statement, if applicable:

’You believe this Reaffirmation Agreement is in your financial interest and you can afford to make the payments on the reaffirmed debt.

Also, check the box at the top of page one that says “No Presumption of Undue Hardship.”

B240A, Reaffirmation Documents |

Page 4 |

PART III. CERTIFICATION BY DEBTOR(S) AND SIGNATURES OF PARTIES

I hereby certify that:

(1)I agree to reaffirm the debt described above.

(2)Before signing this Reaffirmation Agreement, I read the terms disclosed in this Reaffirmation Agreement (Part I) and the Disclosure Statement, Instructions and Definitions included in Part V below;

(3)The Debtor’s Statement in Support of Reaffirmation Agreement (Part II above) is true and complete;

(4)I am entering into this agreement voluntarily and am fully informed of my rights and responsibilities; and

(5)I have received a copy of this completed and signed Reaffirmation Documents form.

SIGNATURE(S) (If this is a joint Reaffirmation Agreement, both debtors must sign.):

Date _____________ |

Signature ________________________________________ |

|

Debtor |

Date _____________ |

Signature ________________________________________ |

|

Joint Debtor, if any |

Reaffirmation Agreement Terms Accepted by Creditor:

Creditor

Print Name |

|

|

Address |

|

|

|

|

|

|

Print Name of Representative |

|

Signature |

|

|

Date |

PART IV. CERTIFICATION BY DEBTOR’S ATTORNEY (IF ANY)

To be filed only if the attorney represented the debtor during the course of negotiating this agreement.

I hereby certify that: (1) this agreement represents a fully informed and voluntary agreement by the debtor; (2) this agreement does not impose an undue hardship on the debtor or any dependent of the debtor; and (3) I have fully advised the debtor of the legal effect and consequences of this agreement and any default under this agreement.

’A presumption of undue hardship has been established with respect to this agreement. In my opinion, however, the debtor is able to make the required payment.

Check box, if the presumption of undue hardship box is checked on page 1 and the creditor is not a Credit Union.

Date __________ Signature of Debtor’s Attorney_______________________________

Print Name of Debtor’s Attorney _____________________________

PART V. DISCLOSURE STATEMENT AND INSTRUCTIONS TO DEBTOR(S)

B240A, Reaffirmation Documents |

Page 5 |

Before agreeing to reaffirm a debt, review the terms disclosed in the Reaffirmation Agreement (Part I above) and these additional important disclosures and instructions.

Reaffirming a debt is a serious financial decision. The law requires you to take certain steps to make sure the decision is in your best interest. If these steps, which are detailed in the Instructions provided in Part V, Section B below, are not completed, the Reaffirmation Agreement is not effective, even though you have signed it.

A.DISCLOSURE STATEMENT

1.What are your obligations if you reaffirm a debt? A reaffirmed debt remains your personal legal obligation to pay. Your reaffirmed debt is not discharged in your bankruptcy case. That means that if you default on your reaffirmed debt after your bankruptcy case is over, your creditor may be able to take your property or your wages. Your obligations will be determined by the Reaffirmation Agreement, which may have changed the terms of the original agreement. If you are reaffirming an open end credit agreement, that agreement or applicable law may permit the creditor to change the terms of that agreement in the future under certain conditions.

2.Are you required to enter into a reaffirmation agreement by any law? No, you are not required to reaffirm a debt by any law. Only agree to reaffirm a debt if it is in your best interest. Be sure you can afford the payments that you agree to make.

3.What if your creditor has a security interest or lien? Your bankruptcy discharge does not eliminate any lien on your property. A ‘‘lien’’ is often referred to as a security interest, deed of trust, mortgage, or security deed. The property subject to a lien is often referred to as collateral. Even if you do not reaffirm and your personal liability on the debt is discharged, your creditor may still have a right under the lien to take the collateral if you do not pay or default on the debt. If the collateral is personal property that is exempt or that the trustee has abandoned, you may be able to redeem the item rather than reaffirm the debt. To redeem, you make a single payment to the creditor equal to the current value of the collateral, as the parties agree or the court determines.

4.How soon do you need to enter into and file a reaffirmation agreement? If you decide to enter into a reaffirmation agreement, you must do so before you receive your discharge. After you have entered into a reaffirmation agreement and all parts of this form that require a signature have been signed, either you or the creditor should file it as soon as possible. The signed agreement must be filed with the court no later than 60 days after the first date set for the meeting of creditors, so that the court will have time to schedule a hearing to approve the agreement if approval is required. However, the court may extend the time for filing, even after the 60-day period has ended.

5.Can you cancel the agreement? You may rescind (cancel) your Reaffirmation Agreement at any time before the bankruptcy court enters your discharge, or during the 60-day period that begins on the date your Reaffirmation Agreement is filed with the court, whichever occurs later. To rescind (cancel) your Reaffirmation Agreement, you must notify the creditor that your Reaffirmation Agreement is rescinded (or canceled). Remember that you can rescind the agreement, even if the court approves it, as long as you rescind within the time allowed.

B240A, Reaffirmation Documents |

Page 6 |

6.When will this Reaffirmation Agreement be effective?

a.If you were represented by an attorney during the negotiation of your Reaffirmation Agreement and

i.if the creditor is not a Credit Union, your Reaffirmation Agreement becomes effective when it is filed with the court unless the reaffirmation is presumed to be an undue hardship. If the Reaffirmation Agreement is presumed to be an undue hardship, the court must review it and may set a hearing to determine whether you have rebutted the presumption of undue hardship.

ii.if the creditor is a Credit Union, your Reaffirmation Agreement becomes effective when it is filed with the court.

b.If you were not represented by an attorney during the negotiation of your Reaffirmation Agreement, the Reaffirmation Agreement will not be effective unless the court approves it. To have the court approve your agreement, you must file a motion. See Instruction 5, below. The court will notify you and the creditor of the hearing on your Reaffirmation Agreement. You must attend this hearing, at which time the judge will review your Reaffirmation Agreement. If the judge decides that the Reaffirmation Agreement is in your best interest, the agreement will be approved and will become effective. However, if your Reaffirmation Agreement is for a consumer debt secured by a mortgage, deed of trust, security deed, or other lien on your real property, like your home, you do not need to file a motion or get court approval of your Reaffirmation Agreement.

7.What if you have questions about what a creditor can do? If you have questions about reaffirming a debt or what the law requires, consult with the attorney who helped you negotiate this agreement. If you do not have an attorney helping you, you may ask the judge to explain the effect of this agreement to you at the hearing to approve the Reaffirmation Agreement. When this disclosure refers to what a creditor “may” do, it is not giving any creditor permission to do anything. The word “may” is used to tell you what might occur if the law permits the creditor to take the action.

B.INSTRUCTIONS

1.Review these Disclosures and carefully consider your decision to reaffirm. If you want to reaffirm, review and complete the information contained in the Reaffirmation Agreement (Part I above). If your case is a joint case, both spouses must sign the agreement if both are reaffirming the debt.

2.Complete the Debtor’s Statement in Support of Reaffirmation Agreement (Part II above). Be sure that you can afford to make the payments that you are agreeing to make and that you have received a copy of the Disclosure Statement and a completed and signed Reaffirmation Agreement.

3.If you were represented by an attorney during the negotiation of your Reaffirmation Agreement, your attorney must sign and date the Certification By Debtor’s Attorney (Part IV above).

4.You or your creditor must file with the court the original of this Reaffirmation Documents packet and a completed Reaffirmation Agreement Cover Sheet (Official Bankruptcy Form 27).

5.If you are not represented by an attorney, you must also complete and file with the court a separate document entitled “Motion for Court Approval of Reaffirmation Agreement” unless your Reaffirmation Agreement is for a consumer debt secured by a lien on your real property, such as your home. You can use Form B240B to do this.

B240A, Reaffirmation Documents |

Page 7 |

C.DEFINITIONS

1.“Amount Reaffirmed” means the total amount of debt that you are agreeing to pay (reaffirm) by entering into this agreement. The total amount of debt includes any unpaid fees and costs that you are agreeing to pay that arose on or before the date of disclosure, which is the date specified in the Reaffirmation Agreement (Part I, Section B above). Your credit agreement may obligate you to pay additional amounts that arise after the date of this disclosure. You should consult your credit agreement to determine whether you are obligated to pay additional amounts that may arise after the date of this disclosure.

2.“Annual Percentage Rate” means the interest rate on a loan expressed under the rules required by federal law. The annual percentage rate (as opposed to the “stated interest rate”) tells you the full cost of your credit including many of the creditor’s fees and charges. You will find the annual percentage rate for your original agreement on the disclosure statement that was given to you when the loan papers were signed or on the monthly statements sent to you for an open end credit account such as a credit card.

3.“Credit Union” means a financial institution as defined in 12 U.S.C. § 461(b)(1)(A)(iv). It is owned and controlled by and provides financial services to its members and typically uses words like “Credit Union” or initials like “C.U.” or “F.C.U.” in its name.