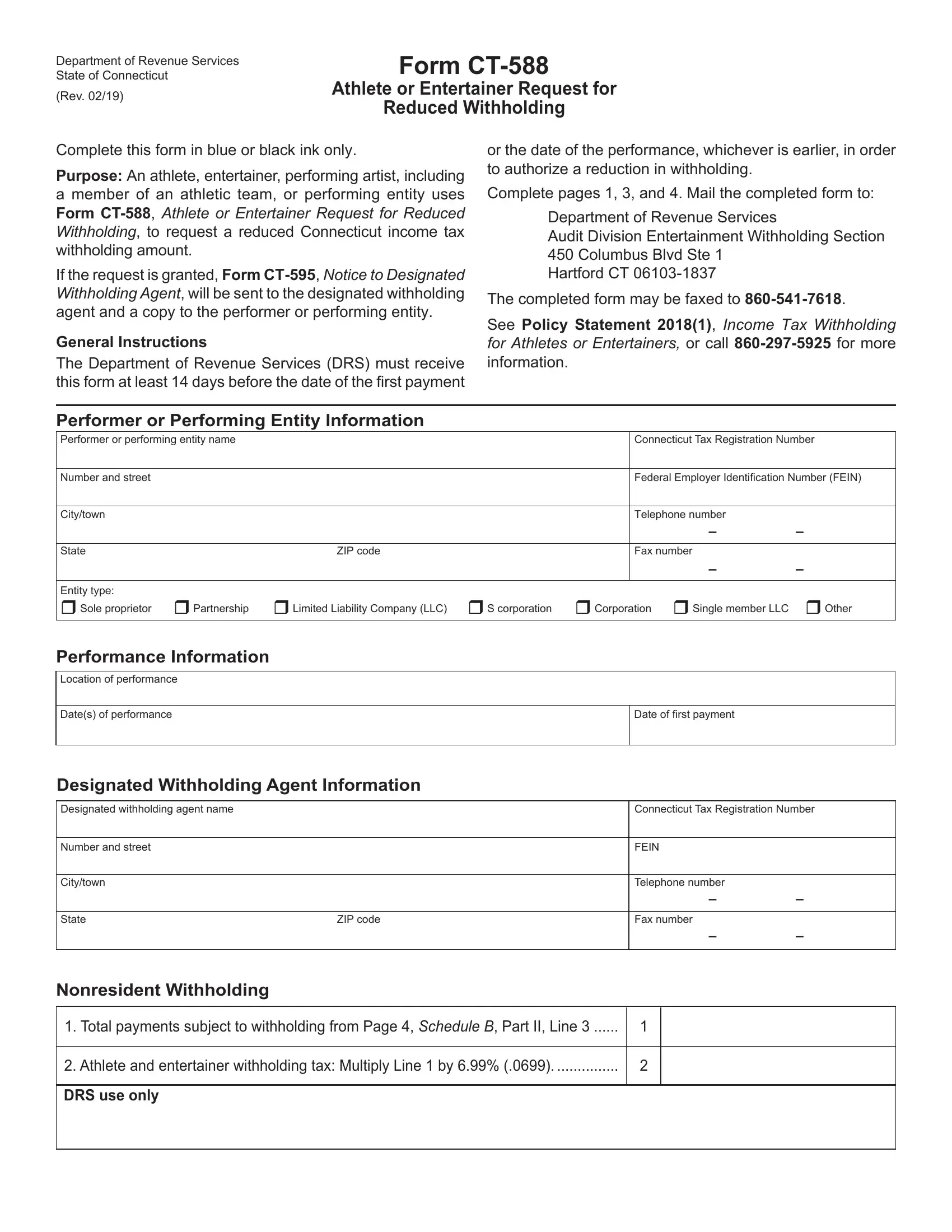

For athletes, entertainers, and performing artists including members of athletic teams or performing entities, navigating the tax landscape can be as challenging as performing itself. This is where Form CT‑588, Athlete or Entertainer Request for Reduced Withholding, comes into play, offering a beacon of clarity in the complex world of tax withholding. Issued by the State of Connecticut's Department of Revenue Services, this essential form is specifically designed to alleviate some of the tax burdens that these professionals might face. By allowing the request for a reduced rate of income tax withholding, it acknowledges the unique financial situations often encountered within these professions. The form must be submitted well in advance of the performance or payment date—14 days to be precise—to ensure timely processing and deduction adjustments. Filling out this form requires detailed information about the performer or entity, performance details, and comprehensive income and expense reports. Successful submissions lead to the issuance of Form CT‑595, signaling the adjusted withholding rate to both the payer and the receiver. This process is not just about requesting a lesser tax deduction; it’s about ensuring that the tax obligations of nonresident athletes and entertainers align more closely with their actual taxable income in Connecticut, thus providing a fairer taxation method tailored to the specifics of their profession.

| Question | Answer |

|---|---|

| Form Name | Form Ct 588 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | ct reduced, revenue entertainer withholding, form ct reduced, ct entertainer form |

Department of Revenue Services State of Connecticut

(Rev. 02/19)

Form CT‑588

Athlete or Entertainer Request for

Reduced Withholding

Complete this form in blue or black ink only.

Purpose: An athlete, entertainer, performing artist, including a member of an athletic team, or performing entity uses Form CT‑588, Athlete or Entertainer Request for Reduced Withholding, to request a reduced Connecticut income tax withholding amount.

If the request is granted, Form CT‑595, Notice to Designated Withholding Agent, will be sent to the designated withholding agent and a copy to the performer or performing entity.

General Instructions

The Department of Revenue Services (DRS) must receive this form at least 14 days before the date of the first payment

or the date of the performance, whichever is earlier, in order to authorize a reduction in withholding.

Complete pages 1, 3, and 4. Mail the completed form to:

Department of Revenue Services

Audit Division Entertainment Withholding Section

450 Columbus Blvd Ste 1

Hartford CT

The completed form may be faxed to 860‑541‑7618.

See Policy Statement 2018(1), Income Tax Withholding for Athletes or Entertainers, or call 860‑297‑5925 for more information.

Performer or Performing Entity Information

Performer or performing entity name |

|

|

|

Connecticut Tax Registration Number |

|||

|

|

|

|

|

|

||

Number and street |

|

|

|

|

Federal Employer Identification Number (FEIN) |

||

|

|

|

|

|

|

|

|

City/town |

|

|

|

|

Telephone number |

|

|

|

|

|

|

|

|

– |

– |

|

|

|

|

|

|

|

|

State |

|

ZIP code |

|

|

Fax number |

|

|

|

|

|

|

|

|

– |

– |

|

|

|

|

|

|

|

|

Entity type: |

|

|

|

|

|

|

|

Sole proprietor |

Partnership |

Limited Liability Company (LLC) |

S corporation |

Corporation |

Single member LLC |

Other |

|

Performance Information

Location of performance

Date(s) of performance

Date of first payment

Designated Withholding Agent Information

Designated withholding agent name |

|

Connecticut Tax Registration Number |

|

|

|

|

|

Number and street |

|

FEIN |

|

|

|

|

|

City/town |

|

Telephone number |

|

|

|

– |

– |

|

|

|

|

State |

ZIP code |

Fax number |

|

|

|

– |

– |

|

|

|

|

Nonresident Withholding

1. Total payments subject to withholding from Page 4, Schedule B, Part II, Line 3 |

1 |

|

|

|

|

2. Athlete and entertainer withholding tax: Multiply Line 1 by 6.99% (.0699) |

2 |

|

|

|

|

DRS use only |

|

|

|

|

|

Form CT‑588

Instructions

Schedule A Instructions

Income: List each item of income received for the

Connecticut performance. If a specific item is not listed, write a description of the item and the amount earned.

Enclose a complete copy of the contract, service agreement, or other documents describing the terms of the performance.

Line 8: Total should equal the total contract amount for the Connecticut performance(s).

Expenses

Column A ‑ Enter the amount paid for each expense related to the Connecticut performance. If a specific expense item

is not listed, write a description of the item and the amount paid. This would include expenses incurred within and without Connecticut to stage the Connecticut performance.

Column B – Enter the amounts paid for services rendered in Connecticut by performers or other service providers.

Example: An artist’s manager provides his/her services solely from a location outside of Connecticut. The amounts paid to that manager would be entered in Column A only and not Column B. If the manager was present in Connecticut for the Connecticut performance, the amount received for the services rendered in Connecticut should be entered in Column B.

Total all income and expense items. The net profit for the Connecticut performance is computed by subtracting the expenses paid for the Connecticut performance from the

income received for the Connecticut performance. The net profit or loss from a Connecticut performance must be

reported on the performing entity’s Connecticut tax return.

If the performing entity is a corporation, Form CT‑1120, Corporation Business Tax Return, must be filed. If the entity

is a

Form CT‑1065/CT‑1120SI, Connecticut Pass‑Through Entity Tax Return, must be filed.

Each expense item listed on Page 3 must correspond to the expenses listed on Page 4, Schedule B, Columns C through I.

Schedule B Instructions

Provide the name of each performer or performing entity receiving payments for a Connecticut performance. An athlete includes but is not limited to a wrestler, boxer, golfer, tennis player, or other athlete, as well as a referee or trainer. An entertainer includes but is not limited to an actor, singer, musician, dancer, circus performer, comedian, public speaker, as well as a writer, director, set designer, or member of a sound, light, or stage crew.

List the amounts received directly or indirectly by each performer or performing entity. Compensation includes all payments received directly for services rendered as well as

all payments received indirectly for such items as hotel, travel, and meals. If a specific payment type is not listed, please

enter that amount under the Other Compensation column.

The totals for each column must correspond to the amounts reported on Schedule A, Lines 9 through 15.

A performer or performing entity may request a waiver of withholding if they meet certain conditions. Refer to Form CT‑590, Athlete or Entertainer Request for Waiver of Withholding, and Policy Statement 2018(1), Income Tax Withholding for Athletes or Entertainers.

A performer or performing entity requesting a waiver of Connecticut withholding must complete Form

Theperformingentityisrequiredtodeterminehowmuchofthe

aggregate income and Connecticut income tax withholding is attributable to each participant identified on Schedule B,

Part I. The performing entity must prepare Form CT‑592, Athlete or Entertainer Withholding Tax Statement, for each participant or other service provider listed on Schedule B, Part I, reporting their allocable share of Connecticut income and Connecticut withholding tax.

Form |

Page 2 of 4 |

Schedule A ‑ Connecticut Athlete and Entertainer Withholding Tax Schedule of Income and Expenses

Date of Performance ____________________ |

|

Location __________________________________________________ |

|

Income |

|

Amount Received for |

|

|

Connecticut Performance |

||

|

|

|

|

|

|

|

|

1. |

Guarantee |

1. |

$ |

|

|

|

|

2. |

Percentage earnings |

2. |

$ |

|

|

|

|

3. |

Merchandise income |

3. |

$ |

|

|

|

|

4. |

Sponsorship income |

4. |

$ |

|

|

|

|

5. |

Venue capacity |

5. |

$ |

|

|

|

|

6. |

Estimated attendance |

6. |

$ |

|

|

|

|

7. |

Other income (list) |

7. |

$ |

a.__________________________________________

b.__________________________________________

c.__________________________________________

d.__________________________________________

e.__________________________________________

8. |

Total income: Add Lines 1 through 7 |

8. |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

B |

|

|

|

Expenses Related to |

Amounts Paid for Services |

Expenses |

|

Connecticut Performance(s) |

Rendered in Connecticut |

|

9. |

Performance fee/guarantee |

9. |

$ |

|

|

|

|

|

|

10. |

Per diems |

10. |

$ |

|

|

|

|

|

|

11. |

Salary |

11 |

$ |

|

|

|

|

|

|

12. |

Hotel and lodging |

12. |

$ |

|

|

|

|

|

|

13. |

Transportation and travel |

13. |

$ |

|

|

|

|

|

|

14. |

Commissions and management fees |

14. |

$ |

|

|

|

|

|

|

15. |

Other compensation |

15. |

$ |

|

|

|

|

|

|

16. |

Insurance |

16. |

$ |

|

|

|

|

|

|

17. |

Equipment lease or rental |

17. |

$ |

|

|

|

|

|

|

18. |

Equipment transportation |

18. |

$ |

|

|

|

|

|

|

19. |

Other expenses (list) |

19. |

$ |

|

a. |

___________________________________________ |

|

|

|

|

|

|

||

b. |

___________________________________________ |

|

|

|

c. |

___________________________________________ |

|

|

|

d. ___________________________________________ |

|

|

|

|

e. ___________________________________________ |

|

|

|

|

|

|

|

|

|

20. Total expenses: Add Lines 9 through 19 |

20. |

$ |

|

|

|

|

|

|

|

21. Net income from Connecticut performances: |

|

|

|

|

|

Subtract Line 20 from Line 8 |

21. |

$ |

|

If performing entity is a sole proprietor or single member LLC, |

|

|

||

enter also on Page 4, Schedule B, Part II, Line 2. |

|

|

|

|

|

|

|

|

|

Form |

Page 3 of 4 |

|

Schedule B ‑ Connecticut Athlete and Entertainer Withholding

Date of show(s) ______________________________ Location ______________________________________________________________________________________________________

Part I - Schedule of Compensation for Each Participant

Attach additional sheets if necessary. Enter totals from all sheets on Line 16, Columns C through J.

|

A |

B |

C |

D |

E |

F |

G |

H |

I |

J |

|

Name of Entertainer |

Social Security |

Performance |

Per Diems |

Salary |

Hotel and |

Transportation |

Commissions/ |

Other |

Total |

|

|

No. or Federal |

Fee/Guarantee |

|

|

Lodging |

and Travel |

Management |

Compensation |

Add |

|

|

Employer ID |

|

|

|

|

|

Fees |

|

Col. C thru I |

|

|

|

|

|

|

|

|

|

|

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16. |

Part I Column Totals: |

|

|

|

|

|

|

|

|

|

|

Column totals must agree with expenses on Page 3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part II - Total Payments Subject to Connecticut Withholding Tax

1. |

Enter Part I, Column J total |

1. |

$ |

|

|

|

|

2. |

Enter net income from Schedule A, Line 21 |

2. |

$ |

|

|

|

|

3. |

Total payments subject to athlete or entertainer withholding tax: Add Line 1 and Line 2. |

3. |

$ |

|

Enter here and on Page 1, Nonresident Withholding, Line 1 |

Form |

Page 4 of 4 |