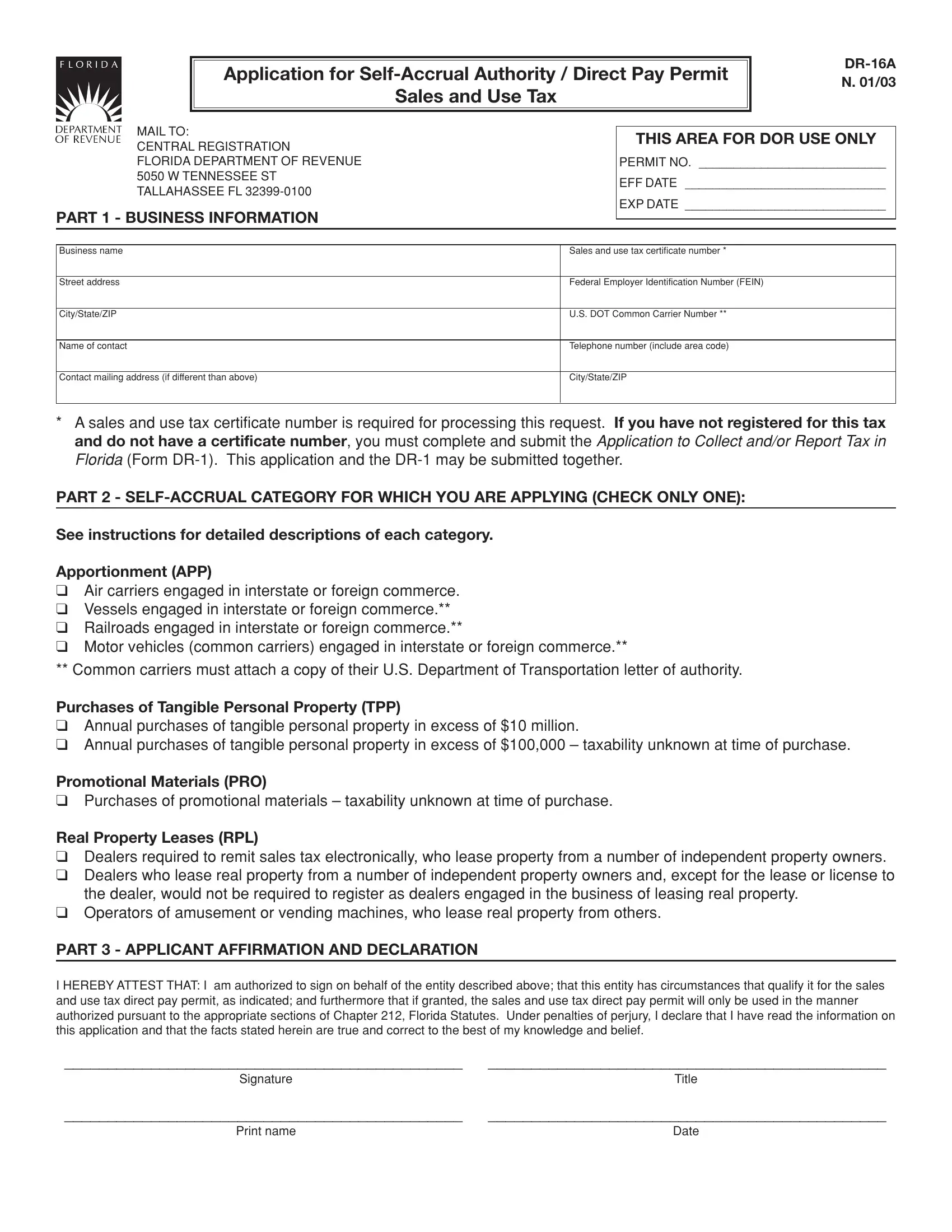

The Application for Self-Accrual Authority / Direct Pay Permit Sales and Use Tax, known as the DR-16A form, plays a critical role for businesses operating within Florida. This document is designed for entities seeking permission to self-accrue sales and use taxes, a process that allows them to directly remit tax payments to the state rather than through vendors at the point of sale. Required by the Florida Department of Revenue, the form requests detailed business information, including the business's name, Federal Employer Identification Number (FEIN), and sales and use tax certificate number, which is pivotal for the processing of this request. The form delineates multiple self-accrual categories, such as Apportionment for various carriers in interstate or foreign commerce, Purchases of Tangible Personal Property by entities with substantial annual purchases, and others, accommodating a range of business activities. Additionally, promotional materials and real property leases are specific categories that address the unique situations of dealers and operators. Applicants must affirm their eligibility and declare their knowledge of the facts under penalties of perjury, ensuring that only qualified entities receive this authority. Completing the DR-16A form accurately is essential for businesses aiming to leverage the direct pay permit, emphasizing the importance of understanding the form’s intricacies and the statutory requirements it entails.

| Question | Answer |

|---|---|

| Form Name | Form Dr 16A |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | tax5 texas direct pay permit form |