You can fill in Form Ftb 3540 easily in our PDF editor online. FormsPal professional team is always endeavoring to enhance the editor and insure that it is even better for clients with its extensive features. Enjoy an ever-evolving experience today! If you're looking to begin, here is what it takes:

Step 1: Just click on the "Get Form Button" in the top section of this site to see our pdf file editing tool. Here you will find everything that is necessary to fill out your document.

Step 2: After you start the PDF editor, you will get the document made ready to be completed. Other than filling in various blanks, you might also perform several other actions with the file, including writing custom text, changing the original text, adding illustrations or photos, affixing your signature to the PDF, and a lot more.

It will be straightforward to complete the document using out practical guide! Here's what you need to do:

1. While completing the Form Ftb 3540, ensure to incorporate all of the essential blanks in their associated area. It will help to facilitate the work, allowing your details to be processed efficiently and properly.

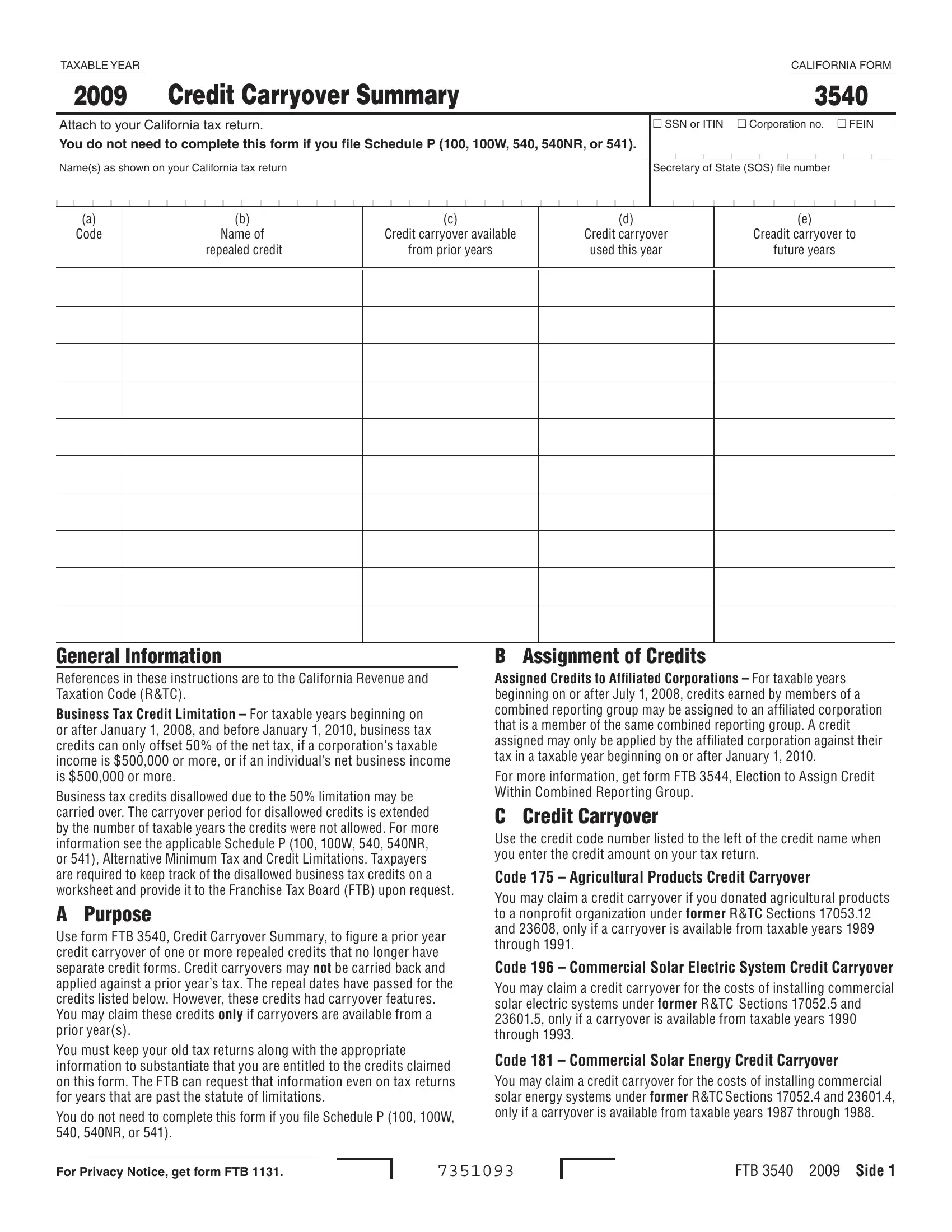

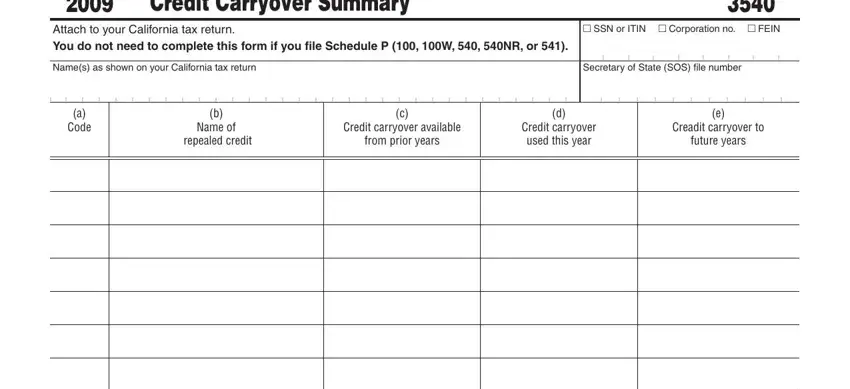

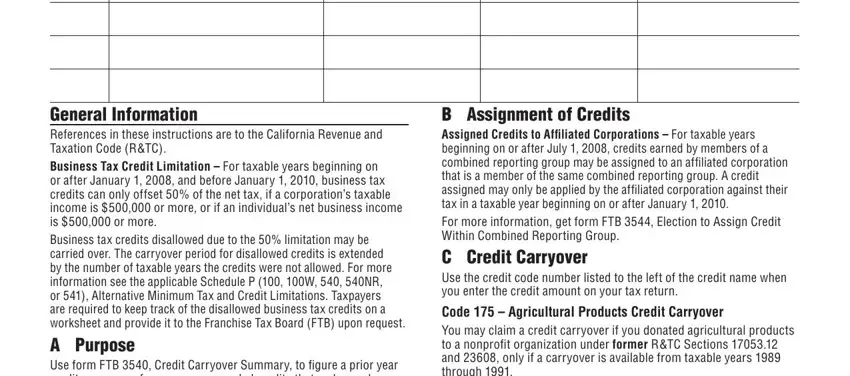

2. Your next step is usually to fill in these particular fields: General Information References in, B Assignment of Credits Assigned, and Code Agricultural Products.

People often make mistakes when filling in General Information References in in this section. Be sure to revise whatever you type in here.

Step 3: Prior to moving forward, ensure that blanks were filled out properly. Once you’re satisfied with it, press “Done." Sign up with us right now and easily use Form Ftb 3540, all set for downloading. All adjustments you make are preserved , allowing you to edit the document later when required. We don't share or sell the information you type in while filling out documents at FormsPal.