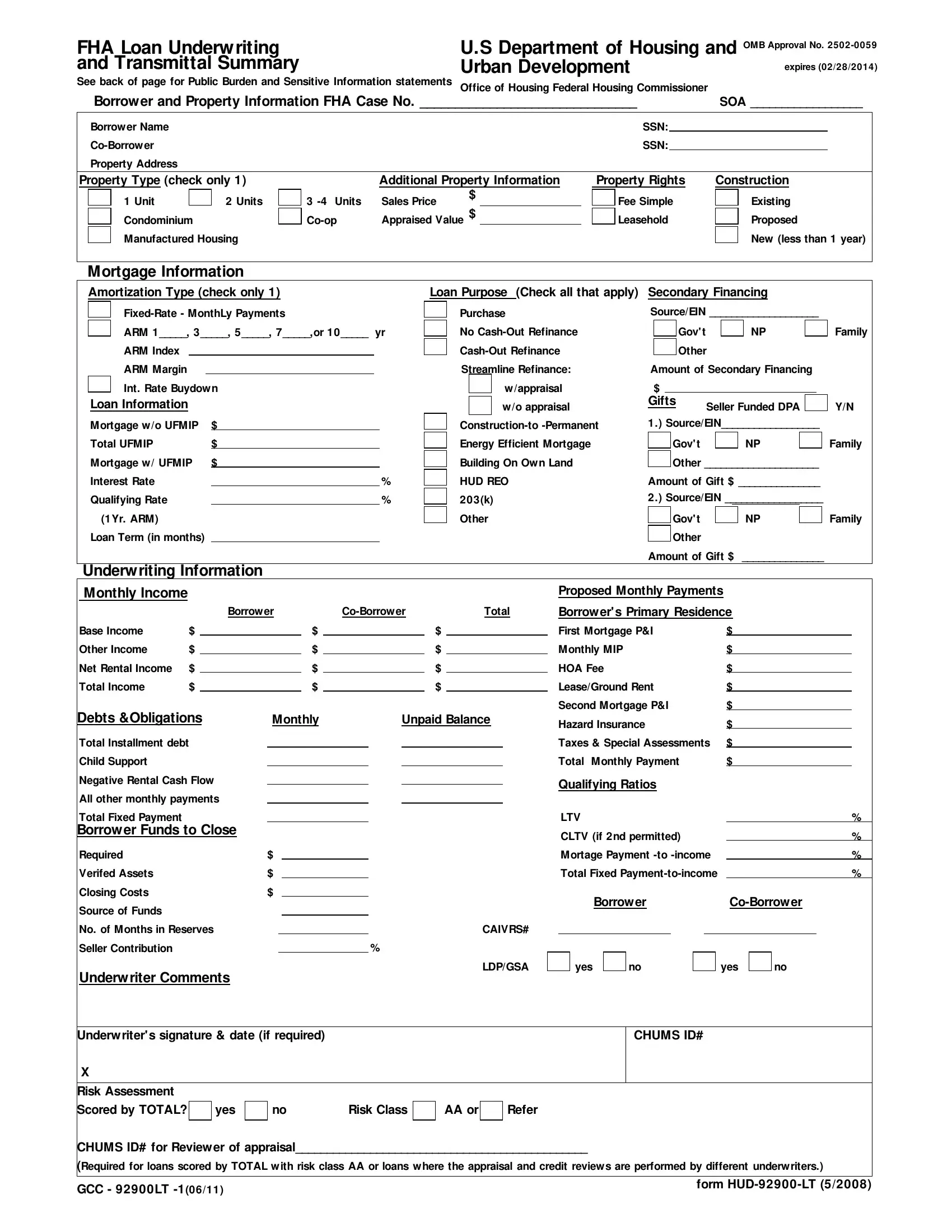

Navigating the complexities of securing a Federal Housing Administration (FHA) loan can be daunting for both borrowers and lenders. At the heart of this process lies the HUD 92900-LT form, a crucial document required by the U.S. Department of Housing and Urban Development (HUD) for FHA loan underwriting and transmittal summary. This form encompasses a wide array of information, including borrower and property specifics, mortgage details like amortization type and loan purpose, as well as underwriting information which assesses the borrower's financial stability and the property's value. It requires meticulous input on the part of the lender, from indicating the property type and rights, detailing the loan's purpose—be it a purchase or various types of refinancing—to calculating the borrower's income and the proposed monthly expenses, and even verifying the borrower's required funds at closing and their sources. Furthermore, it integrates considerations for secondary financing, gifts, and seller contributions, while ensuring compliance with federal guidelines on privacy and data security. Designed to facilitate a comprehensive evaluation of the loan application, the HUD 92900-LT form serves as a foundational element in determining the eligibility for FHA mortgage insurance, streamlining the approval process for lenders and safeguarding the interests of borrowers.

| Question | Answer |

|---|---|

| Form Name | Form Hud 92900Lt |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | fha 92900 lt, form 92900, form 92900 form, mi gcc loan hud 92900 |