The it 370 pdf 2020 filling out course of action is very simple. Our editor allows you to use any PDF form.

Step 1: Search for the button "Get Form Here" on the webpage and click it.

Step 2: You're now free to manage it 370 pdf 2020. You've got lots of options with our multifunctional toolbar - you can add, remove, or modify the information, highlight its certain parts, and perform various other commands.

These particular sections will create the PDF document that you will be filling out:

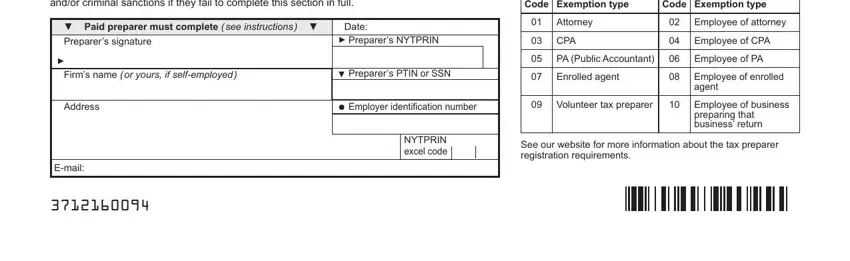

Put the requested particulars in the Paid preparers Under the law all, Code Exemption type, Code Exemption type, Paid preparer must complete see, Date Preparers NYTPRIN, Firms name or yours if, Preparers PTIN or SSN, Attorney, CPA, PA Public Accountant, Enrolled agent, Employee of attorney, Employee of CPA, Employee of PA, and Employee of enrolled agent segment.

Step 3: Hit "Done". You can now upload your PDF form.

Step 4: You can create duplicates of the file tostay clear of all future troubles. Don't worry, we cannot publish or watch your data.