In the state of South Carolina, businesses serving alcoholic beverages are acquainted with the L-2172 form, a crucial document issued by the Department of Revenue. This form, titled "Liquor by the Drink Excise Tax Report," underlines the mandatory excise tax imposition on gross proceeds from the sales of alcoholic liquor by the drink. With a comprehensive structure, the form directs establishments on how to accurately compute their taxes, incorporating a 5% tax rate on gross sales, along with detailing the penalties and interest charges applicable for late submissions. It also emphasizes the significance of submitting the return timely, even when no tax is due, to avoid severe penalties, including monetary fines and potential license suspensions or revocations for repeated violations. Designed to aid in the seamless filing of excise taxes online via MyDORWAY, the state's tax portal, the form offers a streamlined process for businesses. Additionally, it provides information on contact avenues for assistance, ensuring compliance with the law and reinforcing the state's regulations on liquor sales. The form serves not only as a reporting mechanism but as a guideline for businesses to navigate their fiscal responsibilities concerning liquor sales, highlighting the importance of accuracy, timeliness, and adherence to state tax laws.

| Question | Answer |

|---|---|

| Form Name | Form L 2172 |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | sc excise tax, faa 8130 04 form, faa form us, faa form 8130 6 pdf |

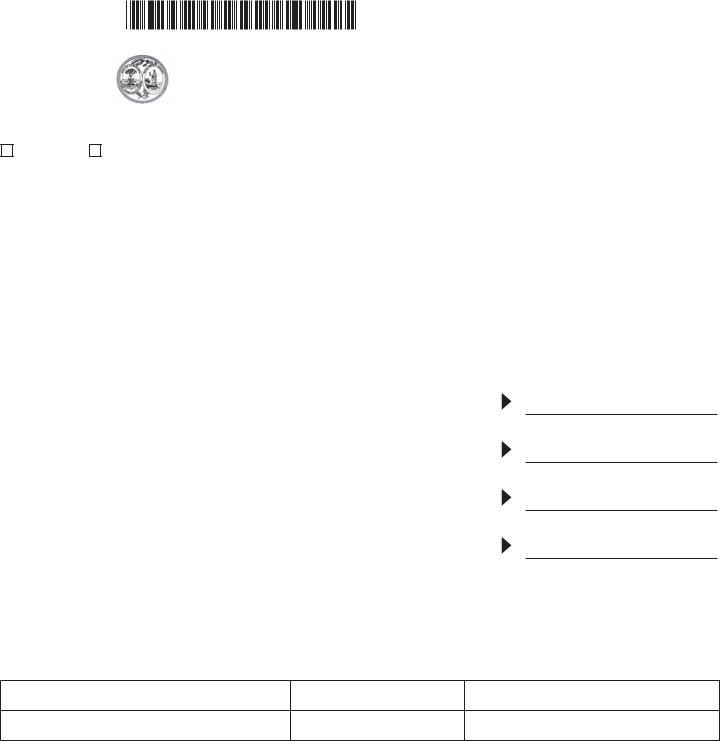

1350

|

STATE OF SOUTH CAROLINA |

|

|||

|

DEPARTMENT OF REVENUE |

|

|||

|

|

(Rev. 2/14/20) |

|||

dor.sc.gov |

LIQUOR BY THE DRINK EXCISE TAX REPORT |

|

4326 |

||

Place an X in all boxes that apply. |

|

File Number |

|||

AMENDED |

Change of Address |

|

|

|

|

(Make changes to |

|

|

|

||

Return |

|

|

|

||

address below) |

|

|

|

||

|

|

|

|

||

|

|

|

|

FEIN |

|

If the area below is blank, fill in name and address. |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

SID Number |

|

|

|

|

|

|

|

|

|

|

|

Period Ended |

|

|

|

|

|

|

|

File online at MyDORWAY.dor.sc.gov

|

|

|

PART I - COMPUTATION OF TAXES |

|

|

||

1. |

Gross proceeds from sales of alcoholic liquor by the drink |

1. |

$ |

||||

|

|

|

|

|

|

|

|

2. |

Excise Tax (multiply line 1 by 5%) |

|

|

2. |

$ |

||

|

|

|

|

|

|

|

|

3. |

Penalty |

|

+ Interest |

|

= |

3. |

$ |

|

|

||||||

4. |

Total Tax Due (add line 2 and line 3) |

|

|

4. |

$ |

||

|

|

|

|

|

|

|

|

Questions? We're here to help. Contact us at LiquorbytheDrinkTax@dor.sc.gov or call

Under penalty of law, I certify that this information is correct, true, and complete to the best of my knowledge.

Signature |

Title |

|

Name (Print) |

Date |

Daytime Phone Number |

Mail to: SCDOR, PO Box 125, Columbia, SC

Make check or money order payable to SCDOR.

43261031

INSTRUCTIONS

Line 1: Gross Proceeds from Sales of Alcoholic Liquor by the Drink

Gross proceeds of sales is the total amount received from the retail sales of a business. This tax is imposed according to Chapter 36, Title 12. Sales tax imposed under Chapter 36, Title 12 is not included in the 'gross proceeds of sales' amount. Visit dor.sc.gov/policy for the complete definition of section code explaining 'gross proceeds of sales'.

Line 2: Excise Tax

Multiply line 1 by the 5% tax rate.

Line 3: Penalty and Interest

If your return is late, enter the total penalty and interest due. Visit dor.sc.gov/calculator to calculate.

PENALTY FOR FAILURE TO FILE A RETURN: 5% of the amount of tax due (from line 2 on page 1) for each month or fraction of a month of delinquency, not to exceed 25%.

PENALTY FOR FAILURE TO PAY TAX DUE: The penalty is 0.5% of the amount of tax due (the total of line 2 on page 1) for each month or fraction of a month of delinquency, not to exceed a total of 25% in the aggregate. The penalty for failure to file and pay must be combined and entered as a total on line 3.

INTEREST: Interest on all overdue accounts will be assessed at the rate provided under Sections 6621 and 6622 of the Internal Revenue Code. Rates may change quarterly. Interest will be compounded daily.

Line 4: Total Excise Tax Due

Add line 2 and line 3.

OTHER PENALTIES MAY APPLY.

Additional Penalties - Pursuant to Code Section

In addition to other penalties and interest, failure to report and pay the full amount of the Excise Tax will result in the following additional penalties:

1.First violation: a civil penalty of $1,000

2.Second violation: a civil penalty of $1,000 and an automatic

3.Third or subsequent violation: a civil penalty of $5,000 and the revocation of your license

Due Date: This return is due by the 20th day of the month following the period covered by the return and becomes late on the 21st day of the month following the period covered.

No credits should be taken on this form.

If your business closes or stops selling liquor by the drink, contact us by mail at: SCDOR, PO Box 125, Columbia, SC

by phone at:

Social Security Privacy Act Disclosure

It is mandatory that you provide your Social Security Number on this tax form if you are an individual taxpayer. 42 U.S.C. 405(c)(2)(C)(i) permits a state to use an individual's Social Security Number as means of identification in administration of any tax. SC Regulation

The Family Privacy Protection Act

Under the Family Privacy Protection Act, the collection of personal information from citizens by the SCDOR is limited to the information necessary for the SCDOR to fulfill its statutory duties. In most instances, once this information is collected by the SCDOR, it is protected by law from public disclosure. In those situations where public disclosure is not prohibited, the Family Privacy Protection Act prevents such information from being used by third parties for commercial solicitation purposes.