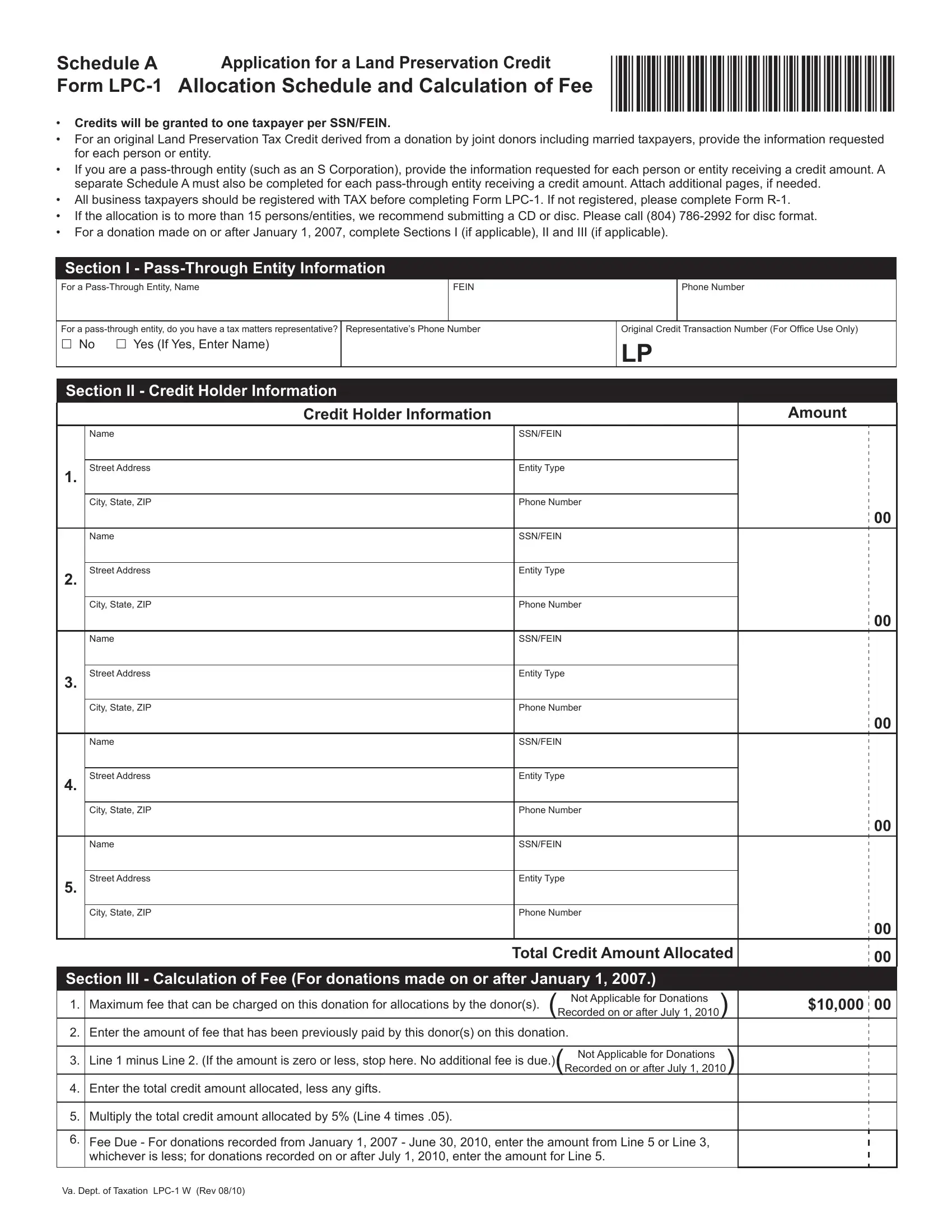

The Schedule A Application for a Land Preservation Credit Form LPC-1 Allocation Schedule and Calculation of Fee embodies a structured approach to facilitate the allocation of land preservation tax credits to eligible taxpayers in Virginia. These credits, pivotal for encouraging land conservation, require detailed documentation for each taxpayer, whether an individual or entity, to ensure compliance and proper allocation. Joint donors, including married taxpayers, and pass-through entities such as S corporations must meticulously provide information for each credit recipient, necessitating a separate Schedule A for each. The form also stipulates registration with the Virginia Department of Taxation prior to completion and suggests using electronic means for submissions involving more than 15 allocates. Significantly, the form addresses the calculation of fees for donations made post-January 1, 2007, marking a shift in policy with the introduction of a fee based on 5% of the total credit amount allocated. This system, refined over the years, highlights the state's commitment to maintaining accountability in tax incentive programs, ensuring that the benefits of land conservation are realized efficiently and equitably among participating taxpayers. Moreover, it includes scenarios and provisions for pass-through entities, illuminating the specifics of credit allocation and the corresponding fee calculation, in line with Virginia's tax code. The anticipation of issues such as the need for additional documentation and the method of fee calculation underlines the form's comprehensive nature in guiding taxpayers through the credit allocation process.

| Question | Answer |

|---|---|

| Form Name | Form Lpc 1 Schedule A |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | lpc hours log template virginia, allocations, 2010, R-1 |

Schedule A Application for a Land Preservation Credit

Form

•Credits will be granted to one taxpayer per SSN/FEIN.

•For an original Land Preservation Tax Credit derived from a donation by joint donors including married taxpayers, provide the information requested for each person or entity.

•If you are a

•All business taxpayers should be registered with TAX before completing Form

•If the allocation is to more than 15 persons/entities, we recommend submitting a CD or disc. Please call (804)

•For a donation made on or after January 1, 2007, complete Sections I (if applicable), II and III (if applicable).

Section I -

For a

FEIN

Phone Number

For a

No Yes (If Yes, Enter Name)

Original Credit Transaction Number (For Ofice Use Only)

LP

Section II - Credit Holder Information

|

Credit Holder Information |

|

|

Amount |

||

|

|

|

|

|

|

|

|

Name |

|

SSN/FEIN |

|

|

|

|

|

|

|

|

|

|

1. |

Street Address |

|

Entity Type |

|

|

|

|

|

|

|

|

|

|

|

City, State, ZIP |

|

Phone Number |

|

|

|

|

|

|

|

00 |

||

|

Name |

|

SSN/FEIN |

|

|

|

|

|

|

|

|

|

|

2. |

Street Address |

|

Entity Type |

|

|

|

|

|

|

|

|

|

|

|

City, State, ZIP |

|

Phone Number |

|

|

|

|

|

|

|

00 |

||

|

Name |

|

SSN/FEIN |

|

|

|

|

|

|

|

|

|

|

3. |

Street Address |

|

Entity Type |

|

|

|

|

|

|

|

|

|

|

|

City, State, ZIP |

|

Phone Number |

|

|

|

|

|

|

|

00 |

||

|

Name |

|

SSN/FEIN |

|

|

|

|

|

|

|

|

|

|

4. |

Street Address |

|

Entity Type |

|

|

|

|

|

|

|

|

|

|

|

City, State, ZIP |

|

Phone Number |

|

|

|

|

|

|

|

00 |

||

|

Name |

|

SSN/FEIN |

|

|

|

|

|

|

|

|

|

|

5. |

Street Address |

|

Entity Type |

|

|

|

|

|

|

|

|

|

|

|

City, State, ZIP |

|

Phone Number |

|

|

|

|

|

|

|

00 |

||

|

|

Total Credit Amount Allocated |

00 |

|||

Section III - Calculation of Fee (For donations made on or after January 1, 2007.)

Not Applicable for Donations |

|

1. Maximum fee that can be charged on this donation for allocations by the donor(s). (Recorded on or after July 1, 2010) |

$10,000 00 |

2. Enter the amount of fee that has been previously paid by this donor(s) on this donation.

3. Line 1 minus Line 2. (If the amount is zero or less, stop here. No additional fee is due.)( Not Applicable for Donations ) Recorded on or after July 1, 2010

4. Enter the total credit amount allocated, less any gifts.

5. Multiply the total credit amount allocated by 5% (Line 4 times .05).

6.Fee Due - For donations recorded from January 1, 2007 - June 30, 2010, enter the amount from Line 5 or Line 3, whichever is less; for donations recorded on or after July 1, 2010, enter the amount for Line 5.

Va. Dept. of Taxation

How to Complete

Lines not mentioned below are

This Schedule should be used by multiple donors (including married spouses when both are on the deed) and

the statute relates the 2% fee to the donated interest and the credit is 40% of that igure, when calculating the fee at the credit level it equates to 5% of the credit

amount being transferred or allocated. An example of the calculation is as follows:

A

Scenario Presented in VA. CODE §

$10,000 (donated interest being transferred/allocated)

x . 02 (fee multiplier imposed by statute)

$200 (fee dollars collected

by statute)

and enter the representative’s name and phone number in the appropriate boxes.

• If you are a |

Corporation), provide the information requested for |

each person or pass through entity receiving a credit. |

A separate Schedule A must be completed for each |

Calculation

of Credit

Value

$10,000 (donated interest being transferred/allocated)

x.40 (credit multiplier

imposed by statute) $4,000 (credit value of the

donated interest)

additional entity receiving a credit. |

• Attach additional pages, if needed. |

• All business taxpayers should be registered with TAX |

before completing Form |

please complete Form |

• For a donation made on or before December 31, 2006, |

complete Section I (if applicable) and II. |

• For a donation made on or after January 1, 2007, |

complete Sections I (if applicable), II and III. Please |

note multiple owners who are listed separately on the |

deed do not owe a fee. |

• If the allocation is to more than 15 persons/entities, |

we recommend submitting a CD or disc. Please call |

Section III – Calculation of Fee

General Information

This section must be completed for an allocation made by

a

A 2% fee of the appraised value of the donated interest

shall be imposed on all transfers arising from the sale of credits and on all

If $200 is the amount of fee collected at the donated

interest level, what percentage of the credit value generates the same fee amount?

Same |

$4,000 (x) = $200 |

|

scenario |

||

x = $200/$4000 |

||

based on |

||

x = .05 or 5% |

||

credit value |

||

|

||

|

|

For donations recorded from January 1, 2007 - June 30,

2010, the fee is capped at $10,000 per credit holder per donation. For donations recorded on or after July 1, 2010, the cap has been removed. If you are transferring/

allocating credits derived from more than one donation,

you must ile a separate

derived from each donation and your fees may exceed $10,000. This fee does not apply to transfers/allocations made in 2007 and beyond on donations made prior to January 1, 2007.

TAX recommends that you pay with a certiied check or money order. Personal checks may delay the

processing of your transfers/allocations.

Va. Dept. of Taxation