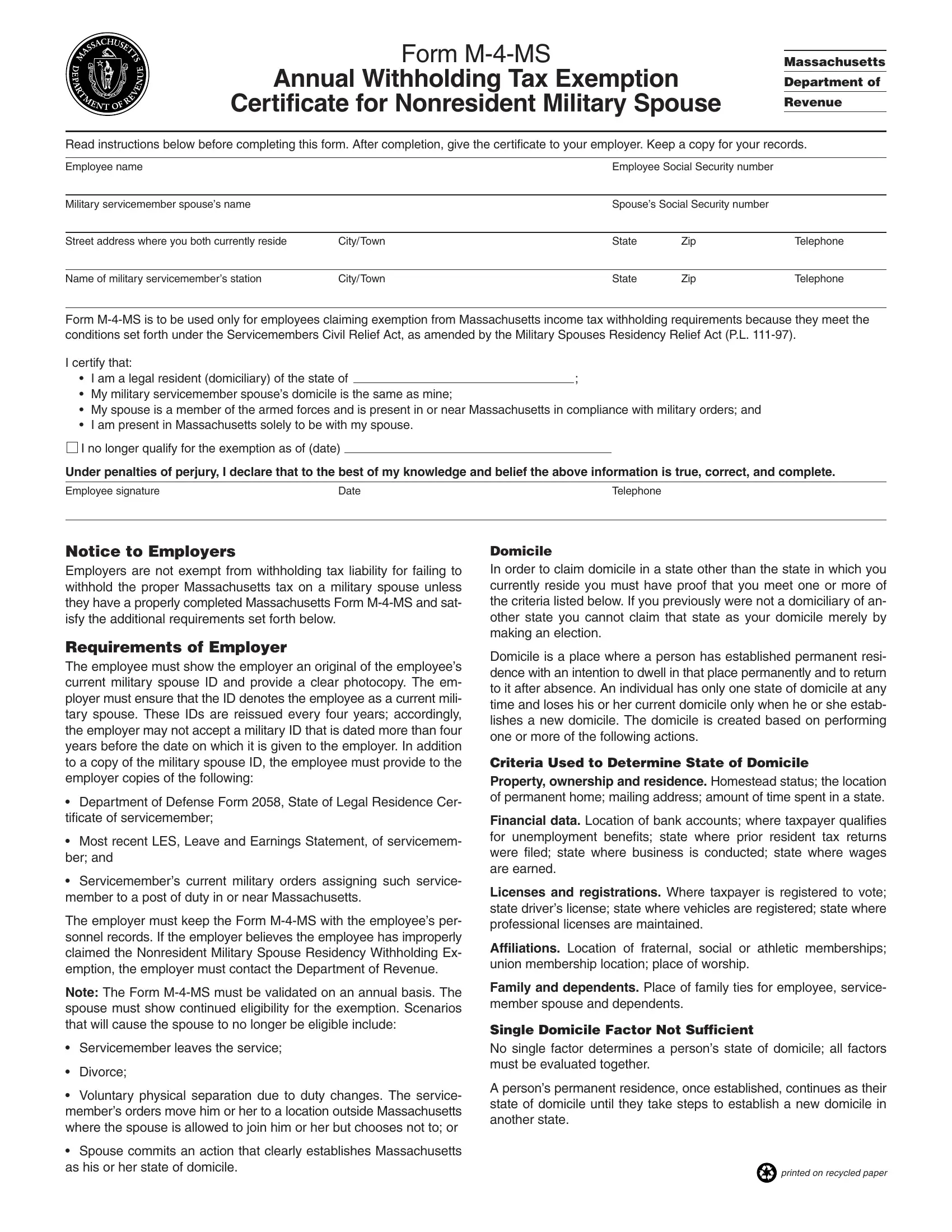

The Form M-4-MS is an essential document for nonresident military spouses in Massachusetts, providing a means to claim exemption from state income tax withholding. This annual Withholding Tax Exemption Certificate is specifically designed to adhere to the regulations under the Servicemembers Civil Relief Act, enhanced by the Military Spouses Residency Relief Act. The form requires detailed information, including personal identification details of both the employee and their military service member spouse, as well as their shared residence and the location of the military service member’s station. The eligibility to use this form hinges on several conditions: the claimant must be a legal resident of the same state as their military spouse, who must be stationed in or near Massachusetts pursuant to military orders, with the spouse living in Massachusetts solely to be with their partner. Employers, on receiving this form, are obligated to verify its completeness and the continued eligibility of the employee by requiring documentation such as a valid military spouse ID, the Service member’s Department of Defense Form 2058, their most recent Leave and Earnings Statement, and current military orders. The document outlines specific scenarios that would disqualify an individual from this exemption, emphasizing the necessity for annual validation of the nonresident spouse's eligibility status. Additionally, the form delves into the definition of domicile and the criteria for establishing one's official state of residency, which is critical for understanding the eligibility for the exemption provided by this form. Massachusetts Department of Revenue mandates employers to retain the form within the employee's personnel records, highlighting the significance of accurate record-keeping in adherence to state tax laws. Overall, the Form M-4-MS serves as a crucial tool for nonresident military spouses, facilitating their financial obligations while acknowledging the unique circumstances of their residency status.

| Question | Answer |

|---|---|

| Form Name | Form M 4 Ms |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | m 4 ms m4ms holiday form |

Form

Annual Withholding Tax Exemption

Certificate for Nonresident Military Spouse

Massachusetts

Department of

Revenue

Read instructions below before completing this form. After completion, give the certificate to your employer. Keep a copy for your records.

Employee name |

|

Employee Social Security number |

|

|

|

|

|

|

|

Military servicemember spouse’s name |

|

Spouse’s Social Security number |

|

|

|

|

|

|

|

Street address where you both currently reside |

City/Town |

State |

Zip |

Telephone |

|

|

|

|

|

Name of military servicemember’s station |

City/Town |

State |

Zip |

Telephone |

Form

I certify that: |

|

• I am a legal resident (domiciliary) of the state of |

; |

•My military servicemember spouse’s domicile is the same as mine;

•My spouse is a member of the armed forces and is present in or near Massachusetts in compliance with military orders; and

•I am present in Massachusetts solely to be with my spouse.

I no longer qualify for the exemption as of (date)

Under penalties of perjury, I declare that to the best of my knowledge and belief the above information is true, correct, and complete.

Employee signature |

Date |

Telephone |

|

|

|

Notice to Employers

Employers are not exempt from withholding tax liability for failing to withhold the proper Massachusetts tax on a military spouse unless they have a properly completed Massachusetts Form

Requirements of Employer

The employee must show the employer an original of the employee’s current military spouse ID and provide a clear photocopy. The em- ployer must ensure that the ID denotes the employee as a current mili- tary spouse. These IDs are reissued every four years; accordingly, the employer may not accept a military ID that is dated more than four years before the date on which it is given to the employer. In addition to a copy of the military spouse ID, the employee must provide to the employer copies of the following:

•Department of Defense Form 2058, State of Legal Residence Cer- tificate of servicemember;

•Most recent LES, Leave and Earnings Statement, of servicemem- ber; and

•Servicemember’s current military orders assigning such service- member to a post of duty in or near Massachusetts.

The employer must keep the Form

Note: The Form

•Servicemember leaves the service;

•Divorce;

•Voluntary physical separation due to duty changes. The service- member’s orders move him or her to a location outside Massachusetts where the spouse is allowed to join him or her but chooses not to; or

•Spouse commits an action that clearly establishes Massachusetts as his or her state of domicile.

Domicile

In order to claim domicile in a state other than the state in which you currently reside you must have proof that you meet one or more of the criteria listed below. If you previously were not a domiciliary of an- other state you cannot claim that state as your domicile merely by making an election.

Domicile is a place where a person has established permanent resi- dence with an intention to dwell in that place permanently and to return to it after absence. An individual has only one state of domicile at any time and loses his or her current domicile only when he or she estab- lishes a new domicile. The domicile is created based on performing one or more of the following actions.

Criteria Used to Determine State of Domicile

Property,ownershipandresidence.Homestead status; the location of permanent home; mailing address; amount of time spent in a state.

Financial data. Location of bank accounts; where taxpayer qualifies for unemployment benefits; state where prior resident tax returns were filed; state where business is conducted; state where wages are earned.

Licenses and registrations. Where taxpayer is registered to vote; state driver’s license; state where vehicles are registered; state where professional licenses are maintained.

Affiliations. Location of fraternal, social or athletic memberships; union membership location; place of worship.

Family and dependents. Place of family ties for employee, service- member spouse and dependents.

Single Domicile Factor Not Sufficient

No single factor determines a person’s state of domicile; all factors must be evaluated together.

A person’s permanent residence, once established, continues as their state of domicile until they take steps to establish a new domicile in another state.

printed on recycled paper