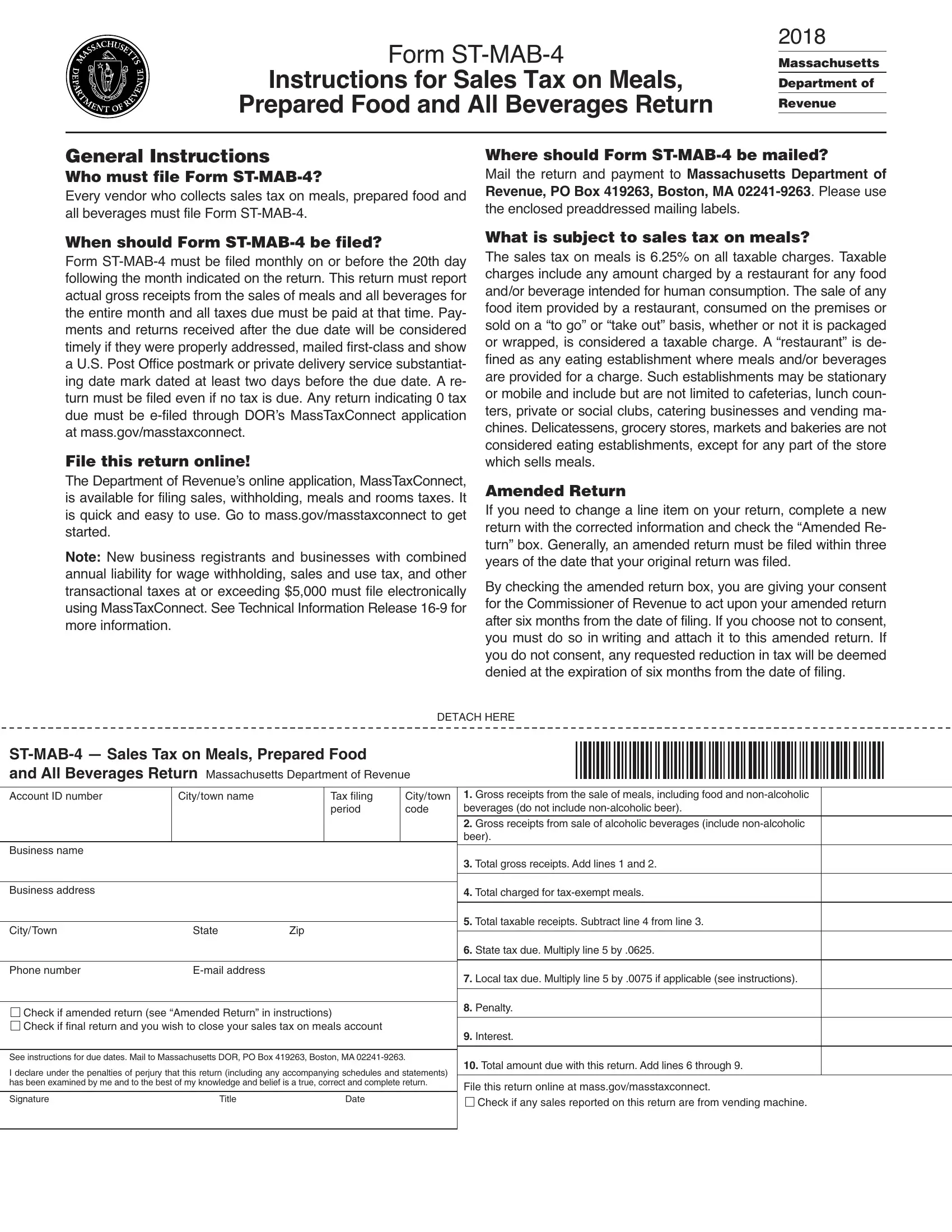

In today’s fast-paced business environment, vendors in Massachusetts dealing with meals, prepared food, and beverages must navigate through the intricacies of tax filing, including the submission of Form ST-MAB-4. This form, updated by the Massachusetts Department of Revenue in April 2018, is indispensable for every vendor who collects sales tax on meals and beverages. It outlines who must file, how to submit payments, the deadlines for submission, and detailed instructions on calculating taxes due. Vendors must file this form monthly, ensuring it reaches the Department of Revenue by the 20th day following the month in review. Those who miss the deadline can still be considered compliant if the submission is postmarked at least two days before the due date. Additionally, the form directs users to the department's MassTaxConnect online platform, making filing quicker and requiring electronic submission for businesses with a certain threshold of annual tax liability. This tool simplifies the reporting of gross receipts from sales of meals and all beverages, whether alcoholic or non-alcoholic, and provides a straightforward method to amend returns or close accounts. The guidance on what qualifies as taxable under the meals tax is clear, emphasizing the 6.25% tax on all charges by establishments deemed as restaurants for both dine-in and take-out services. The risks of penalties for late filings or errors in payment are also outlined, serving as a cautionary reminder to businesses about the importance of accuracy and timeliness in their tax affairs. Furthermore, this form plays a crucial role in amending previously submitted returns, detailing the process for businesses that discover discrepancies in their filings. In essence, Form ST-MAB-4 encapsulates a critical component of tax compliance for vendors in the food and beverage sector in Massachusetts, providing a structured approach to fulfilling their sales tax obligations.

| Question | Answer |

|---|---|

| Form Name | Form St Mab 4 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | st mab 4, mass gov st mab 4 form, stmab 4 tax meals, massachusetts stmab 4 |