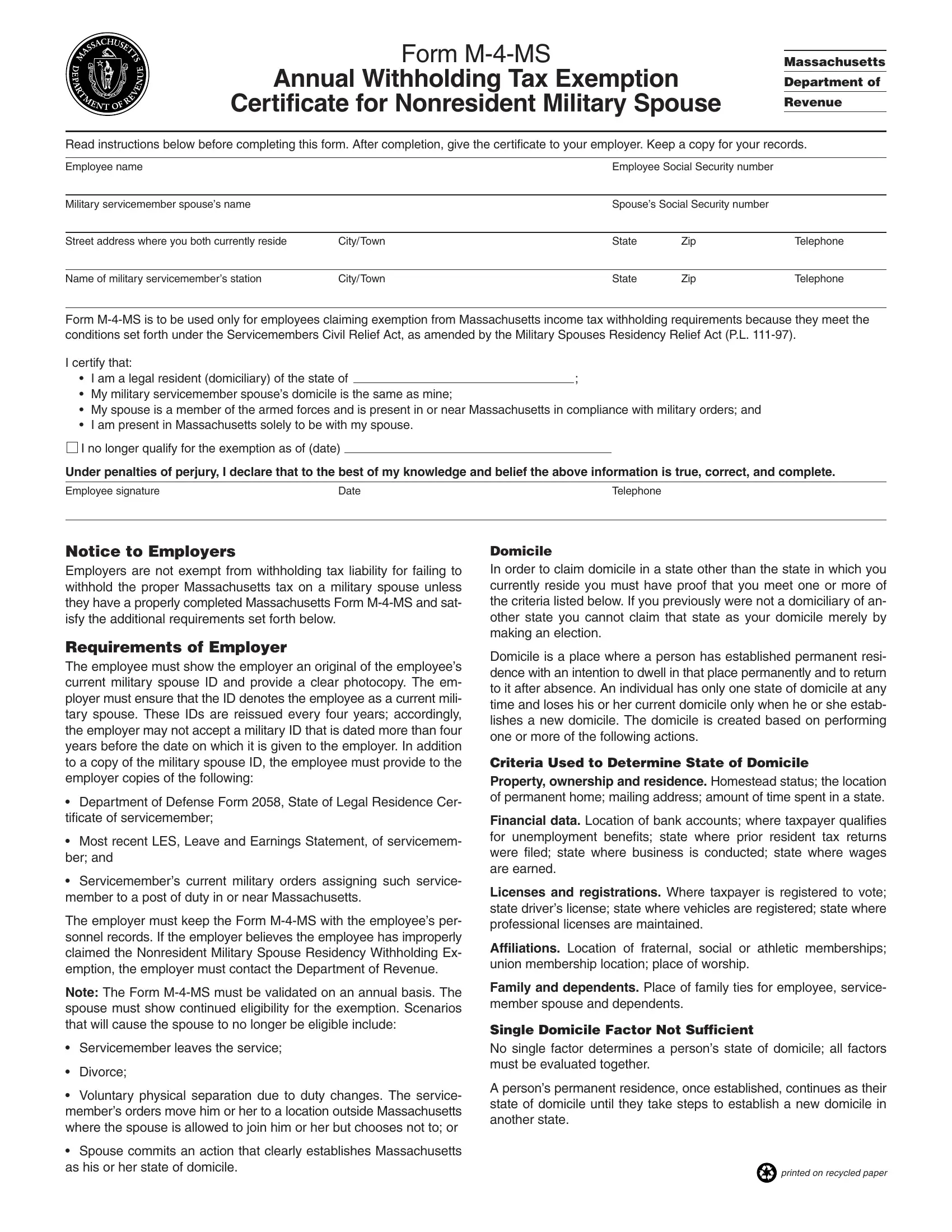

The Form M-4-MS is an essential document for nonresident military spouses in Massachusetts, providing a means to claim exemption from state income tax withholding. This annual Withholding Tax Exemption Certificate is specifically designed to adhere to the regulations under the Servicemembers Civil Relief Act, enhanced by the Military Spouses Residency Relief Act. The form requires detailed information, including personal identification details of both the employee and their military service member spouse, as well as their shared residence and the location of the military service member’s station. The eligibility to use this form hinges on several conditions: the claimant must be a legal resident of the same state as their military spouse, who must be stationed in or near Massachusetts pursuant to military orders, with the spouse living in Massachusetts solely to be with their partner. Employers, on receiving this form, are obligated to verify its completeness and the continued eligibility of the employee by requiring documentation such as a valid military spouse ID, the Service member’s Department of Defense Form 2058, their most recent Leave and Earnings Statement, and current military orders. The document outlines specific scenarios that would disqualify an individual from this exemption, emphasizing the necessity for annual validation of the nonresident spouse's eligibility status. Additionally, the form delves into the definition of domicile and the criteria for establishing one's official state of residency, which is critical for understanding the eligibility for the exemption provided by this form. Massachusetts Department of Revenue mandates employers to retain the form within the employee's personnel records, highlighting the significance of accurate record-keeping in adherence to state tax laws. Overall, the Form M-4-MS serves as a crucial tool for nonresident military spouses, facilitating their financial obligations while acknowledging the unique circumstances of their residency status.

| Question | Answer |

|---|---|

| Form Name | Form M 4 Ms |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | m 4 ms m4ms holiday form |