Have you ever had to fill out Form N-288C? If so, you know just how important this form is. This form is used by the United States Citizenship and Immigration Services (USCIS) to determine an individual's eligibility for naturalization. In order to complete this form, you will need to provide a number of details about your background and your current status in the United States. The good news is that USCIS has made it easy to complete this form by providing detailed instructions on their website. Make sure that you take the time to read these instructions carefully before completing the form.

| Question | Answer |

|---|---|

| Form Name | Form N 288C |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | N-35, n288c, N-20, N-40 |

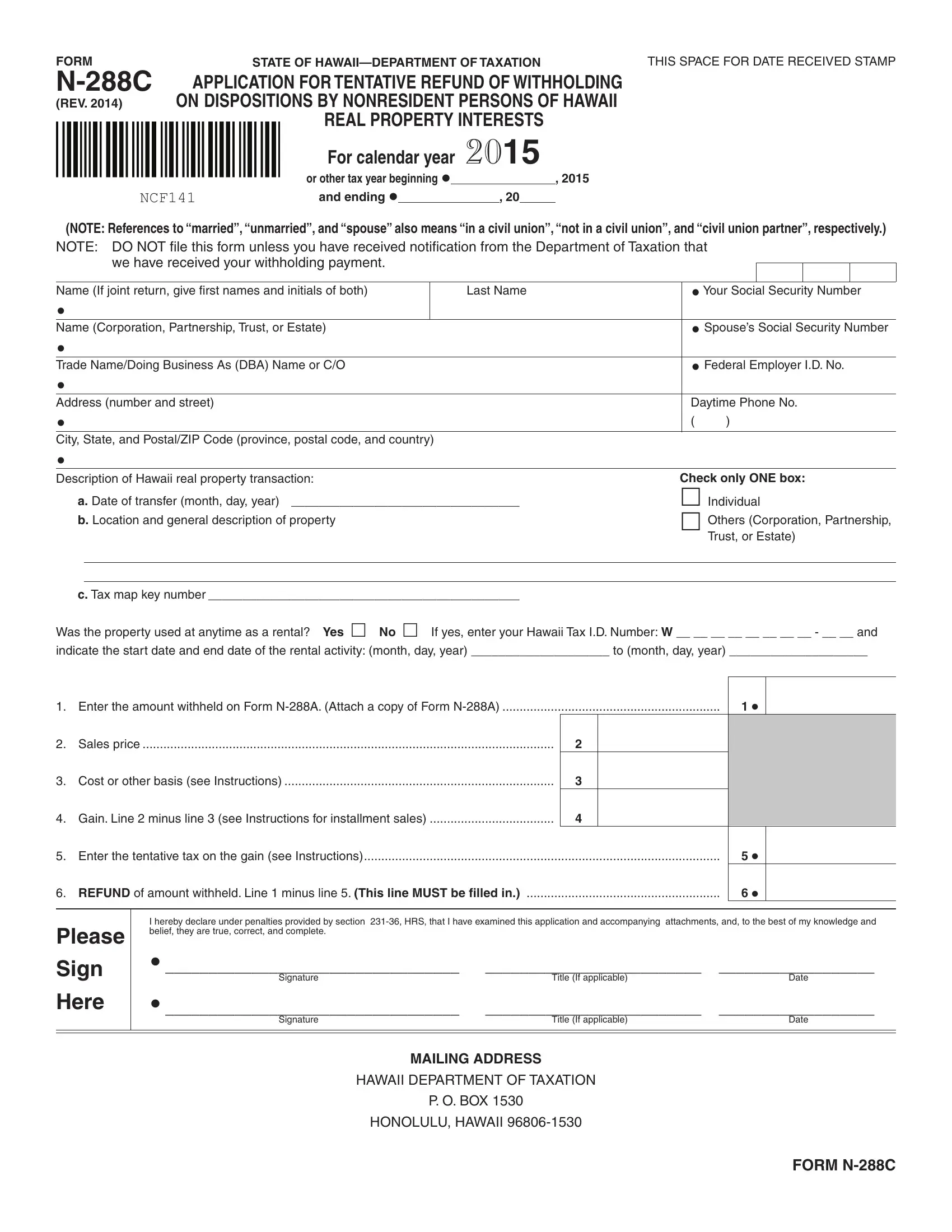

FORM |

|

STATE OF |

THIS SPACE FOR DATE RECEIVED STAMP |

||||

APPLICATION FOR TENTATIVE REFUND OF WITHHOLDING |

|||||||

(REV. 2014) |

ON DISPOSITIONS BY NONRESIDENT PERSONS OF HAWAII |

||||||

|

|

REAL PROPERTY INTERESTS |

|

||||

|

|

For calendar year 2015 |

|

||||

|

|

or other tax year beginning λ |

|

|

|

, 2015 |

|

NCF141 |

and ending λ |

|

|

, 20 |

|

|

|

(NOTE: References to “married”, “unmarried”, and “spouse” also means “in a civil union”, “not in a civil union”, and “civil union partner”, respectively.)

NOTE: DO NOT file this form unless you have received notification from the Department of Taxation that we have received your withholding payment.

Name (If joint return, give first names and initials of both) |

|

Last Name |

Your Social Security Number |

||

|

|

|

|

|

|

Name (Corporation, Partnership, Trust, or Estate) |

|

Spouse’s Social Security Number |

|||

|

|

|

|

|

|

Trade Name/Doing Business As (DBA) Name or C/O |

|

Federal Employer I.D. No. |

|||

|

|

|

|

|

|

Address (number and street) |

|

Daytime Phone No. |

|||

|

|

|

|

( |

) |

City, State, and Postal/ZIP Code (province, postal code, and country) |

|

|

|

||

|

|

|

|

|

|

Description of Hawaii real property transaction: |

|

Check only ONE box: |

|||

a. Date of transfer (month, day, year) _________________________________ |

£ Individual |

||||

b. Location and general description of property |

|

£ Others (Corporation, Partnership, |

|||

|

|

|

|

|

Trust, or Estate) |

|

|

|

|

|

|

|

|

|

|

|

|

c. Tax map key number _____________________________________________

Was the property used at anytime as a rental? Yes £ No £ If yes, enter your Hawaii Tax I.D. Number: W __ __ __ __ __ __ __ __ - __ __ and

indicate the start date and end date of the rental activity: (month, day, year) ____________________ to (month, day, year) ____________________

1. |

Enter the amount withheld on Form |

|

|

1 • |

|

|

2. |

Sales price |

2 |

|

|

|

|

3. |

Cost or other basis (see Instructions) |

3 |

|

|

|

|

4. |

Gain. Line 2 minus line 3 (see Instructions for installment sales) |

|

4 |

|

|

|

5. |

Enter the tentative tax on the gain (see Instructions) |

|

|

5 • |

|

|

6. |

REFUND of amount withheld. Line 1 minus line 5. (This line MUST be filled in.) |

|

|

6 • |

|

|

Please

Sign

Here

I hereby declare under penalties provided by section

__________________________________ |

_________________________ |

__________________ |

Signature |

Title (If applicable) |

Date |

__________________________________ |

_________________________ |

__________________ |

Signature |

Title (If applicable) |

Date |

MAILING ADDRESS

HAWAII DEPARTMENT OF TAXATION

P. O. BOX 1530

HONOLULU, HAWAII

FORM

FORM

General Instructions

Purpose of Form

Use Form

IMPORTANT: If Form

Who May File an Application

The transferor/seller may file Form

NOTE: Under Section

return, or within two years from the time the tax was paid, whichever is later.

Where to Send Form

File Form

Specific Instructions

NOTE: Before you begin to fill in Form N- 288C, you should review the notification you received from the Department of Taxation that we have received your withholding pay- ment to make sure that the information con- tained in it is correct. If any information is not correct, please return a copy of the notifica- tion to the Department of Taxation with the corrected information.

At the top of Form

Also, enter the name, address, and identification number (social security number or federal employer I.D. number), if any, of the transferor/seller applying for a refund of the amount withheld. The name and identification number entered MUST be the same as the name and identification number entered for the transferor/seller on Form

PAGE 2

issued an individual taxpayer identification number (ITIN) by the IRS, enter the ITIN. If the individual has applied for an ITIN but the IRS has not yet issued the ITIN, write “Applied For”.

Also, enter the information describing the Hawaii real property transaction. In b, enter the address and description of the property. In c, enter the tax map key number.

Line 2. Enter the gross sales price from the sale. Attach a copy of your closing escrow statement from your sale of this property.

Line 3. In general, the cost or adjusted basis is the cost of the property plus purchase commis- sions and improvements, minus depreciation (if applicable). Increase the cost or other basis by any expense of sale, such as commissions and state transfer taxes. Complete the Computation of cost or other basis worksheet below and enter the amount from line 4 onto the front of Form N- 288C, line 3.

Line 4. Line 2 minus line 3. However, if you are reporting the gain under the installment method, attach a separate sheet showing the principal payments received during the taxable year and the gross profit percentage. Multiply the amount of the principal payments by the gross profit per- centage and enter the result onto the front of Form

Line 5. If you are a C corporation, multiply line 4 by 4% and enter the result on line 5. If you are a

2015 Tax Rate Schedules

Schedule I

SINGLE INDIVIDUALS AND MARRIED INDIVIDUALS FILING SEPARATE RETURNS

If the taxable income is: |

The tax shall be: |

Not over $2,400 |

1.40% of taxable income |

Over $2,400 but not over $4,800 |

$34.00 plus 3.20% over $2,400 |

Over $4,800 but not over $9,600 |

$110.00 plus 5.50% over $4,800 |

Over $9,600 but not over $14,400 |

$374.00 plus 6.40% over $9,600 |

Over $14,400 but not over $19,200 |

$682.00 plus 6.80% over $14,400 |

Over $19,200 but not over $24,000 |

$1,008.00 plus 7.20% over $19,200 |

Over $24,000 |

$1,354.00 plus 7.25% over $24,000 |

Schedule II

MARRIED INDIVIDUALS FILING JOINT RETURNS AND CERTAIN WIDOWS AND WIDOWERS

If the taxable income is: |

The tax shall be: |

Not over $4,800 |

1.40% of taxable income |

Over $4,800 but not over $9,600 |

$67.00 plus 3.20% over $4,800 |

Over $9,600 but not over $19,200 |

$221.00 plus 5.50% over $9,600 |

Over $19,200 but not over $28,800 |

$749.00 plus 6.40% over $19,200 |

Over $28,800 but not over $38,400 |

$1,363.00 plus 6.80% over $28,800 |

Over $38,400 but not over $48,000 |

$2,016.00 plus 7.20% over $38,400 |

Over $48,000 |

$2,707.00 plus 7.25% over $48,000 |

|

Schedule III |

|

HEAD OF HOUSEHOLD |

If the taxable income is: |

The tax shall be: |

Not over $3,600 |

1.40% of taxable income |

Over $3,600 but not over $7,200 |

$50.00 plus 3.20% over $3,600 |

Over $7,200 but not over $14,400 |

$166.00 plus 5.50% over $7,200 |

Over $14,400 but not over $21,600 |

$562.00 plus 6.40% over $14,400 |

Over $21,600 but not over $28,800 |

$1,022.00 plus 6.80% over $21,600 |

Over $28,800 but not over $36,000 |

$1,512.00 plus 7.20% over $28,800 |

Over $36,000 |

$2,030.00 plus 7.25% over $36,000 |

person other than a C corporation, you must use the tax rate schedules to the left to determine the amount to enter on line 5.

Note: These tax rates apply to

For partnerships, S corporations, trusts, or estates, the gain on line 4 must be allocated among each partner or member, S corporation shareholder, or beneficiary of the trust or estate. Calculate the tax liability for each partner or member, S corporation shareholder, or beneficiary of the trust or estate. Enter the total tax liability of all partners or members, S corporation shareholders, or beneficiaries of the trust or estate on line 5. Attach a schedule showing the name, identification number, and the amount of gain and tax liability allocated to each partner or member, S corporation shareholder, or beneficiary of the trust or estate. Also, show the computation of the tax liability for each partner or member, S corporation shareholder, or beneficiary of the trust or estate.

Signature

Form

NOTE: Incomplete forms will be returned to the transferor/seller. Please fill out all items.

Computation of cost or other basis

1. |

Purchase price of property |

|

$ |

______________________ |

||

2. |

Add: |

Improvements |

$ |

_____________________ |

|

|

|

|

Selling expenses |

|

_____________________ |

|

|

|

|

Other (list) |

_________________________________ |

|

_____________________ |

______________________ |

3. |

Less: |

Depreciation |

|

|

_____________________ |

|

|

|

Other (list) |

_________________________________ |

|

_____________________ |

______________________ |

4. |

Adjusted basis of property. (Line 1 plus line 2, minus line 3) |

|

$ |

______________________ |

||

|

|

|

|

|

|

|