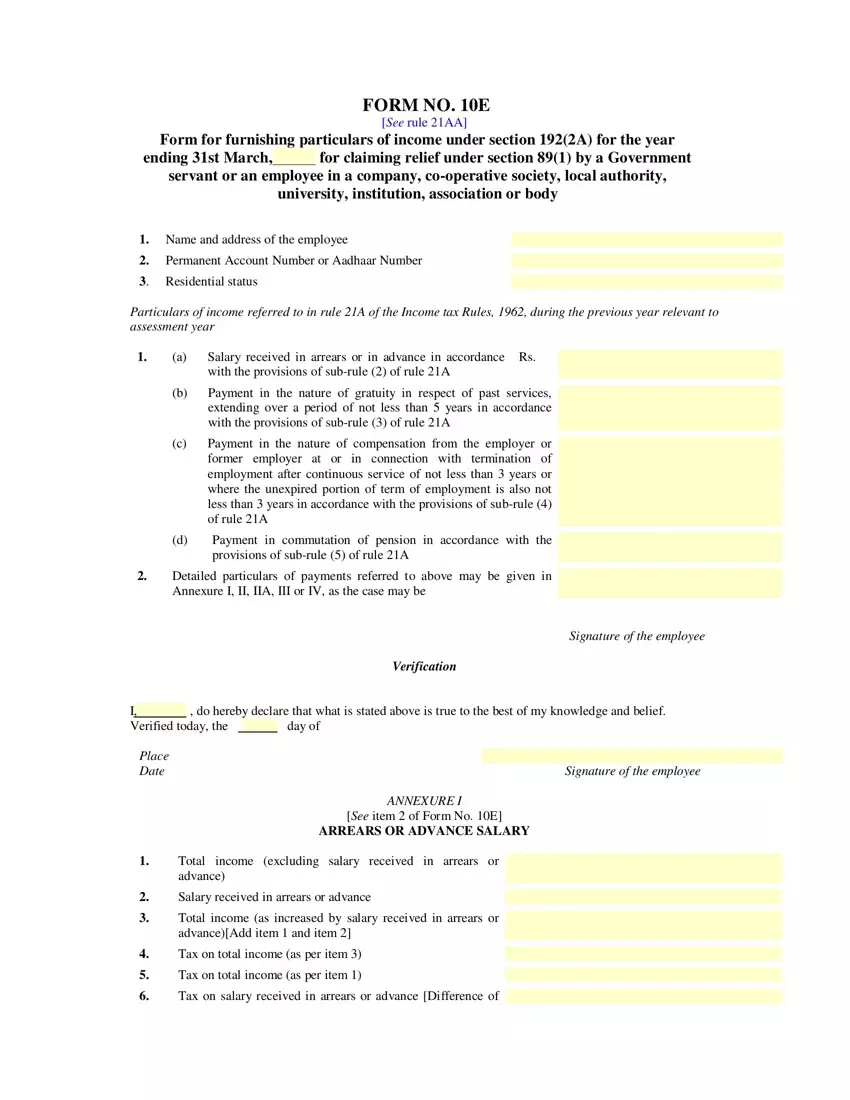

The No 10E form plays a crucial role for employees looking to claim relief under section 89(1) due to income received in arrears or advance, gratuity for past services, compensation for termination of employment, or pension commutation. Required for a government servant or an employee in varied sectors, including companies and universities, this form details pertinent personal information along with financial specifics needed for tax calculations. It provides a structured way to furnish particulars of income that differ from the regular earnings, ensuring accurate tax relief calculation for the assessment year. The annexures attached to the form guide individuals through the complex process of reporting additional earnings, tax on total income, and the tax payable after adjusting for arrears or advances, gratuity, compensation, and pension commutation, making it an essential document for those eligible for tax relief under the specified conditions.

| Question | Answer |

|---|---|

| Form Name | Form No 10E |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | 10e excel sheet download, 10e form in excel format ay 2020 21, form 10e calculator, form 10e in excel |