The Form NYC-399Z plays a pivotal role for corporations and unincorporated businesses operating within New York City, especially in the aftermath of changes following September 10, 2001. Tailored to address depreciation adjustments for certain property, this form intricately structures the computation of allowable New York City depreciation for qualifying properties not aligned with standard federal depreciation regulations introduced post-9/11. Specifically designed to cater to properties that would have been eligible for enhanced deductions under IRC §168(k) but are instead confined to depreciation calculations as if acquired on September 10, 2001, it covers not only the computation of allowable depreciation for the current year but also adjustments for sport utility vehicles and the disposition of properties. Form NYC-399Z requires entities to closely adhere to modifications in federal legislation regarding depreciation, including provisions from the Economic Stimulus Act of 2008 and subsequent adjustments through legislation like the 2015 PATH Act and TCJA—each altering the landscape of bonus depreciation. In conjunction with addressing depreciation computation, the form extends its relevance to adjustments required upon the disposition of property, ensuring that discrepancies between federal and New York City depreciation deductions are recalibrated for both entire net income and unincorporated business entire net income calculations. Beyond its primary function, this form encapsulates a unique provision for certain sport utility vehicles, responding to limitations imposed by IRC §280F and adjusting the allowable deduction for New York City tax purposes. Entities entangled in the specifics of qualifying property, qualified Resurgence Zone property, or the delineation of sport utility vehicles within the bounds of city and federal tax regulations, find Form NYC-399Z indispensable to comply with the nuanced tax landscape shaped significantly by post-9/11 legislative adjustments.

| Question | Answer |

|---|---|

| Form Name | Form Nyc 399Z |

| Form Length | 5 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 15 sec |

| Other names | Fillable Online 8B BANKING CORPORATION TAX CLAIM FOR ... |

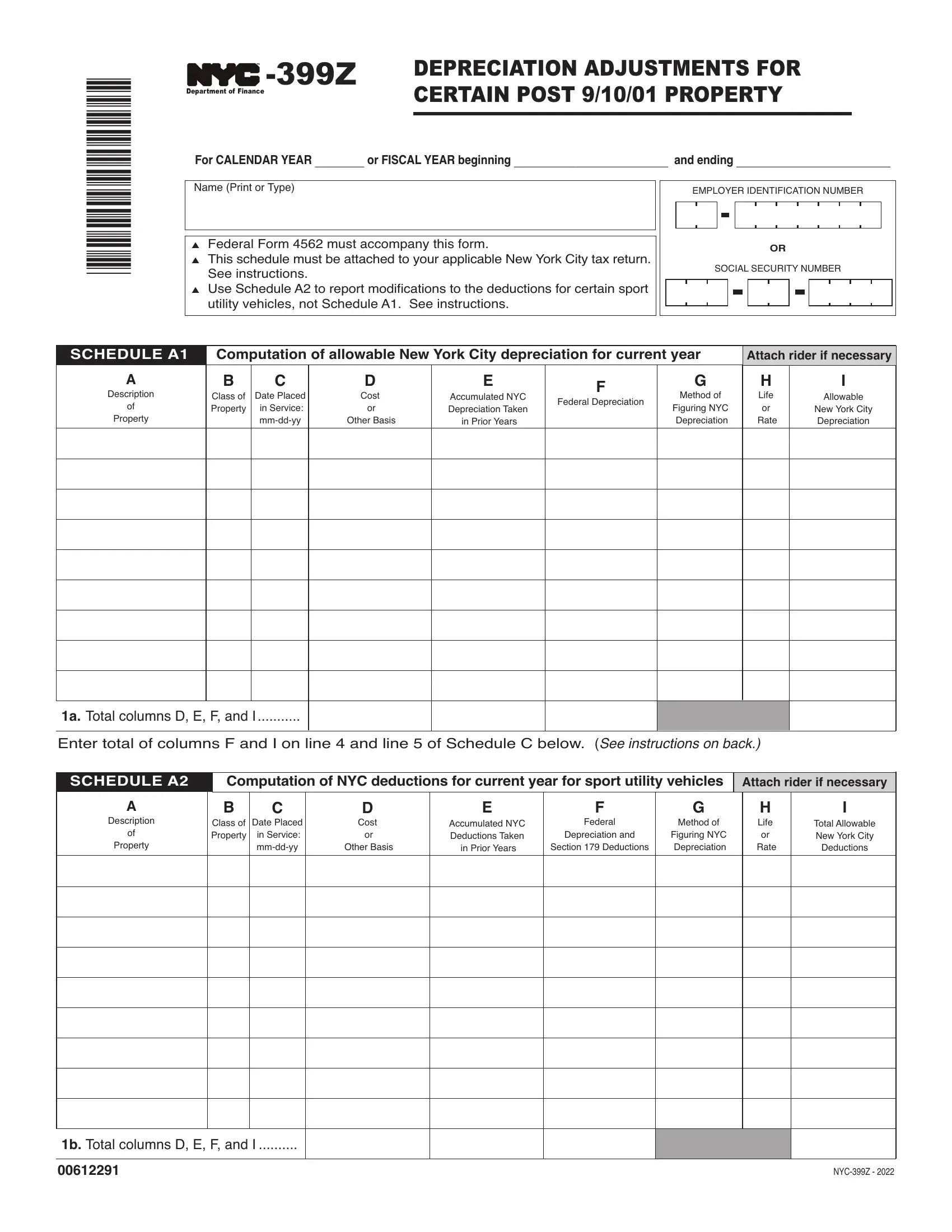

*00612191*

DEPRECIATION ADJUSTMENTS FOR |

|

|

CERTAIN POST 9/10/01 PROPERTY |

|

|

ForCALENDARYEAR________orFISCALYEARbeginning_________________________ andending_________________________

mentore)

▲ ederlormmustmpnthisorm |

|

|

▲ |

hissedulemustettedtourpplileeworit |

txreturn |

|

Seeinstruions |

|

▲ |

seSeduletoreportmodiitionstothededuionsor |

rtinsport |

|

utilitvehiesnotSeduleSeeinstruions |

|

|

|

|

OR

SS

SCHEDULE A1 |

Computation of allowable New York City depreciation for current year |

Attach rider if necessary |

|

|

|

A |

B |

C |

D |

E |

|

F |

G |

|

H |

|

I |

esption |

lsso |

ted |

ost |

multed |

|

thodo |

|

ie |

|

lowle |

|

|

ederlepretion |

|

|

||||||||

o |

pert |

inServi |

or |

epretionn |

|

iurin |

|

or |

|

eworit |

|

|

|

|

|

||||||||

pert |

|

mmd |

thersis |

inorers |

|

|

epretion |

|

te |

|

epretion |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a.otllumnsnd |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

tertotlolumnsndonlinendlineoS |

|

eduleelow |

See instructions on back.) |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE A2 |

Computation of NYC deductions for current year for sport utility vehicles |

Attach rider if necessary |

|||||||||

A |

B |

C |

D |

E |

|

F |

G |

|

H |

|

I |

esption |

lsso |

ted |

ost |

multed |

|

ederl |

thodo |

|

ie |

|

otllowle |

o |

pert |

inServi |

or |

eduionsn |

|

epretionnd |

iurin |

|

or |

|

eworit |

pert |

|

mmd |

thersis |

inorers |

Seioneduions |

epretion |

|

te |

|

eduions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b.otllumnsnd |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00612191 |

|

|

|

|

|

|

|

|

|

|

|

Form |

Page 2 |

|

|

SCHEDULE B

Disposition adjustment

Attach rider if necessary

oreitemopropertlistedelowdeterminethediere |

netweenederlndeworitdeduionsusedint |

hemputtionoederl |

|

ndeworittxleinmeinpriorrs |

|

|

|

▲ |

ederldeduionexedseworitdeduionsutr |

lumnromlumnndenterinlumn |

|

▲ |

eworitdeduionexedsederlsutrlumnro |

mlumnndenterinlumn |

|

A |

B |

C |

D |

E |

F |

G |

|

esption |

lsso |

ted |

otlederl |

otl |

justment |

justment |

|

|

pert |

inServi |

|||||

opert |

epretionn |

epretionn |

minus |

minus) |

|||

S) |

mmd |

||||||

|

|||||||

|

|

|

|

|

2. |

otlexssederldeduionsover deduions |

(see instructions) |

|

|

|

||||

3. |

otl exss deduionsoverederldeduions |

(see instructions) |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

SCHEDULE C |

Computation of adjustments to New York City income |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. ederl |

|

B. eworit |

|

|

|

|

|

|

|

|

|

|

|

4. |

termountromSedulelinelumn |

|

4. |

|

|

|

|

||

5. |

termountromSedulelinelumn |

|

5. |

|

|

|

|

||

6a. termountromSedulelineolumn |

|

6a. |

|

|

|

|

|||

6b.termountromSedulelineolumn |

|

6b. |

|

|

|

|

|||

7a. termountromSeduleline |

|

7a. |

|

|

|

|

|||

7b.termountromSeduleline |

|

7b. |

|

|

|

|

|||

8. |

otls lumnlinesndlumnlines |

nd |

8. |

|

|

|

|

||

terthemountonlinelumnsndditionndt |

hemountonlinelumnsdeduionontheppl |

ileeworitreturneinstr) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*00622191*

00622191

GENERAL INFORMATION

The NewYork CityAdministrative Code, as amended pursuant to the authority granted under Part G of Chapter 93 of the Laws of 2002, limits the depreciation deduction for "qualified prop- erty," other than "qualified Resurgence Zone property," to the deduction that would have been allowed for such property under IRC §167 had the property been acquired by the tax- payer on September 10, 2001, and therefore, not been eligible for the enhanced deductions allowed by the IRC §168(k). "Qualified Resurgence Zone property" is "qualified property" used substantially in the Resurgence Zone in connection with the active conduct of a trade or business where the original use began with the taxpayer in the Resurgence Zone after Sep- tember 10, 2001. The Resurgence Zone (defined in sections

gain or loss included in entire net income or unincorporated business entire net income upon the disposition of any property for which the federal and New York City depreciation deduc- tions differ.

NOTE

Deductions for "qualified Resurgence Zone property," are not affected by the above decoupling provisions other than for cer- tain sport utility vehicles. The additional

NOTE

Any exceptions to the decoupling provisions provided in the Administrative Code for Qualified New York Liberty Zone property or Qualified New York Liberty Zone leasehold im- provements as defined in IRC §1400L have expired.

Form |

Page 3 |

|

|

Economic StimulusAct of 2008 and

Other Federal Legislation Effecting Depre-

ciation.

Section 102 of the Economic Stimulus Act of 2008, Pub.L. No.

In 2015, Section 143 of the Protecting Ameri- cans from Tax Hikes Act of 2015, Pub. L. No.

Most recently, section 13201(b) of theTax Cuts and Jobs Act of 2017 (“TCJA”) extended the bonus depreciation deduction to cover property placedinservicebeforeJanuary1,2027(except for aircraft and

Under the TCJA, the first year depreciation limit increase of $8,000 for passenger automo- biles under §280(F)(a)(1)(A) is extended to in- clude automobiles placed in service on or before December 31, 2026. Prior to that, in order to qualify for the $8,000 increase in bonus depreciation, the passenger automobile would have had to been placed into service on or before December 31, 2019. This extension of the placed in service deadline only applies

to automobiles acquired on or after September 28, 2017. However, if the passenger automo- biles was acquired before September 28, 2018, the first year additional depreciation is phased down to $6,400 in the case of an automobile placed in service during 2018 and to $4,800 in the case of automobile placed in service during 2019.

However, as discussed above the Administra- tive Code limits the depreciation for “qualified property” other than “Qualified Resurgence Zone property” to the deduction that would have been allowed for such property had the property been acquired by the taxpayer on Sep- tember 10, 2001, and therefore, except for Qualified Resurgence Zone property, as de- fined in the Administrative Code, the City has decoupled from the federal bonus depreciation provision. The Administrative Code also re- quires appropriate adjustments to the amount of any gain or loss included in entire net in- come or unincorporated business entire net in- come upon the disposition of any property for which the federal and New York City depreci- ation deductions differ.

Special Provisions for Certain Sport Utility

Vehicles for Tax Periods Beginning on or

AfterJanuary 1, 2004

Under Section 280F of the Internal Revenue Code, the federal depreciation deduction under sections 167 and 168 of the Internal Revenue Code and the expense in lieu of depreciation deduction under section 179 of the Internal Revenue Code for certain passenger automo- biles are generally limited to the amounts pro- vided in section 280F(a)(1) of the Internal Revenue Code. Congress passed legislation that limits the amount deductible for certain sport utility vehicles. That legislation does not affect the modifications required for City tax purposes described below. For tax years begin- ning on or after January 1, 2004, in determining ENI of taxpayers, other than eligible farmers (for purposes of the New York State farmers' school tax credit), the amount allowed as a de- duction for NewYork City purposes (for either depreciation or expense in lieu of depreciation) with respect to a sport utility vehicle (SUV) that is NOT a passenger automobile for pur- poses of section 280F(d)(5) of the Internal Rev- enue Code is limited to the amount that would be allowed under section 280F(a)(1) of the In- ternal Revenue Code if the vehicle were a pas- senger automobile as defined in section 280F(d)(5). For all SUVs subject to these spe- cial provisions, the amount allowed as a de- duction is calculated as of the date the SUV was actually placed in service and not as of September 10, 2001. (The date that is applica- ble to qualified property, other than qualified Resurgence Zone property and New York Lib- erty Zone property, under the general post- 9/11/01 decoupling provisions).

On the disposition of an SUV subject to this limitation, the amount of any gain or loss in- cluded in ENI must be adjusted to reflect the limited deductions allowed for City purposes under this provision. See Finance Memoran- dum

Coordination of Federal depreciation and City decoupling provisions with respect to SUVs

As discussed above, the Economic Stimulus Act of 2008 amended IRC section 168(k) to provide bonus depreciation for certain property acquired in 2008. The Act also amended §168(k)(2)(F)(i) to increase the first year de- preciation allowed under §280F(a)(1)(A) by $8,000 for passenger automobiles to which the

WHO MUSTUSETHIS FORM

A corporation or unincorporated business that files or is included in a

●

●

●

●

Form |

Page 4 |

|

|

must use Form

1)it claims for federal purposes a deprecia- tion deduction for "qualified property" pursuant to the Economic StimulusAct of 2008, or subsequent federal legislation including the 2015 PATH Act or TCJA other than “Qualified Resurgence Zone property.”

2)it is not an eligible farmer (for purposes of the NewYork State farmers' school tax credit) and it claims for federal purposes a depreciation deduction or an expense deduction in lieu of depreciation deduc- tion under section 179 of the Internal Revenue Code for an SUV that is NOT a passenger automobile for purposes of sec- tion 280F(d)(5) of the Internal Revenue Code (regardless of whether the SUV is “qualified property” under IRC §168(k).

NOTE

Corporations and unincorporated businesses meeting the criteria set forth in #1 or #2 above are not permitted to file on Form

SPECIFIC INSTRUCTIONS

SCHEDULE A1

The purpose of this schedule is to compute the allowableNewYorkCitydepreciationdeduction. This form has been designed to be used with the federal depreciation schedule, Form 4562 (Rev. March2002orlater). Acopyofthefederalform must accompany this Form

Column A

Enter a brief description of each item of “qual- ified property,” other than “qualified Resur- gence Zone property,” included in part II or III of federal Form 4562.

Column B

For each item of property listed in column A, indicate the property class type used in com- puting the federal deduction. Use “UPM” for property which is depreciated under the unit of production method provided in IRC §168(f)(1).

ColumnD

The cost or other basis entered in this column must be the same amount used for federal pur- poses prior to any reduction for the special de- preciation allowance for qualified property.

ColumnG |

total amount that may be deducted for New |

||||

Indicate the depreciation method selected for |

York City purposes in the current tax year for |

||||

the computation of the New York City allow- |

an SUV subject to the special provisions. See |

||||

able depreciation deduction.Any method used |

Finance Memorandum |

||||

to compute depreciation that would have been |

IRC §280F Limits to Sport Utility Vehicles”. |

||||

allowed under IRC §167, had the property been |

|

|

|

|

|

acquired on September 10, 2001, will be ac- |

SCHEDULE B |

||||

ceptable. This includes such methods as |

|

|

|

|

|

Column A |

|

||||

depreciation, |

Enter each item of property disposed of during |

||||

or any other consistent method. |

the taxable year separately.Attach a rider if ad- |

||||

|

ditional room is needed. |

||||

Column I |

|

|

|

|

|

Enter depreciation computed by the method in- |

Column D |

|

|||

dicated in column G computed as IRC §167 |

Enter for each item of property the total amount |

||||

would have applied had the property been ac- |

of federal deductions used in the computation |

||||

quired on September 10, 2001. Total of this |

of prior years’ federal taxable income. For an |

||||

column will be the amount allowable as a de- |

SUV subject to the special provisions, the |

||||

duction for New York City. |

amount entered in Column D should include |

||||

any amount deducted under section 179 of the |

|||||

|

|||||

LINE 1a |

Internal Revenue Code. |

||||

|

|

|

|

||

Enter total of columns F and I on lines 4 and 5 |

Column E |

|

|||

of Schedule C, as indicated. |

|

||||

Enter for each item of property the total amount |

|||||

|

|||||

If you have disposed of “qualified property” |

of New York City deductions used in the com- |

||||

other than “qualified Resurgence Zone prop- |

putation of prior years’ New York City entire |

||||

erty,” in any year after the year of acquisition, |

net income. |

|

|||

you must complete Schedule B. |

Column F |

|

|||

|

|

||||

SCHEDULEA2 |

For any item of property, if column D exceeds |

||||

column E, subtract column E from column D |

|||||

|

|||||

ColumnA |

and enter the excess in this column. |

||||

|

|

|

|

||

Enter the year, make and model for each SUV. |

Column G |

|

|||

ColumnB |

For any item of property, if column E exceeds |

||||

column D, subtract column D from column E |

|||||

Indicate the property class type used or that |

|||||

and enter the excess in this column. |

|||||

would be used in computing federal deprecia- |

|

|

|

|

|

tion for each SUV. |

LINE 2 |

|

|

|

|

|

|

|

|

||

ColumnD |

Add the amounts in column F and enter the |

||||

total on line 2 and on Schedule C, line 7a. |

|||||

The amount entered in this column must be |

|||||

|

|

|

|

||

equal to the cost or other basis used for federal |

LINE 3 |

|

|

|

|

purposes prior to any special depreciation al- |

Add the amounts in column G and enter the |

||||

lowances for qualified property and prior to the |

total on line 3 and on Schedule C, line 7b. |

||||

expense in lieu of depreciation deduction al- |

|

|

|

|

|

lowed under section 179 of the Internal Rev- |

SCHEDULE C |

||||

enue Code. |

|

|

|

|

|

|

LINE 8 |

|

|

|

|

ColumnE |

Enter the amount on line 8A as an addition on |

||||

Enter the total New York City depreciation |

the applicable New York City tax return. Use |

||||

taken in prior years including, for years prior |

the following lines. Attach an explanation. |

||||

to 2018, the amount of any deduction taken |

|

|

|

|

|

under section 179 of the Internal Revenue |

|||||

Code for New York City purposes. |

Schedule B, line 6c |

||||

|

|||||

ColumnF |

- |

Schedule B, line 4 |

|||

For each SUV, enter the sum of the amount of |

- |

Schedule B, line 10c |

|||

the federal depreciation deduction taken and |

|||||

amount of any federal expense in lieu of de- |

|||||

preciation deduction taken under section 179 |

- |

Schedule B, line 14c |

|||

of the Internal Revenue Code for the current |

- |

Schedule B, line 8 |

|||

tax period. |

- |

Schedule B, line 11 |

|||

|

|||||

ColumnI |

|||||

The amount entered in column I should be the |

- |

Schedule B, Line 6 |

|||

Form |

Page 5 |

|

|

Enter the amount on line 8B as a deduction on the applicable New York City tax return. Use the following lines. Attach an explanation.

*If this form is for the reporting corporation, enter amounts on the appropriate lines in Col- umnA. For any other member of the combined group, enter amounts on the appropriate lines on Form

**If this form is for the designated agent, enter amounts in the appropriate column. For any other member of the combined group, enter amounts on the appropriate lines on Form