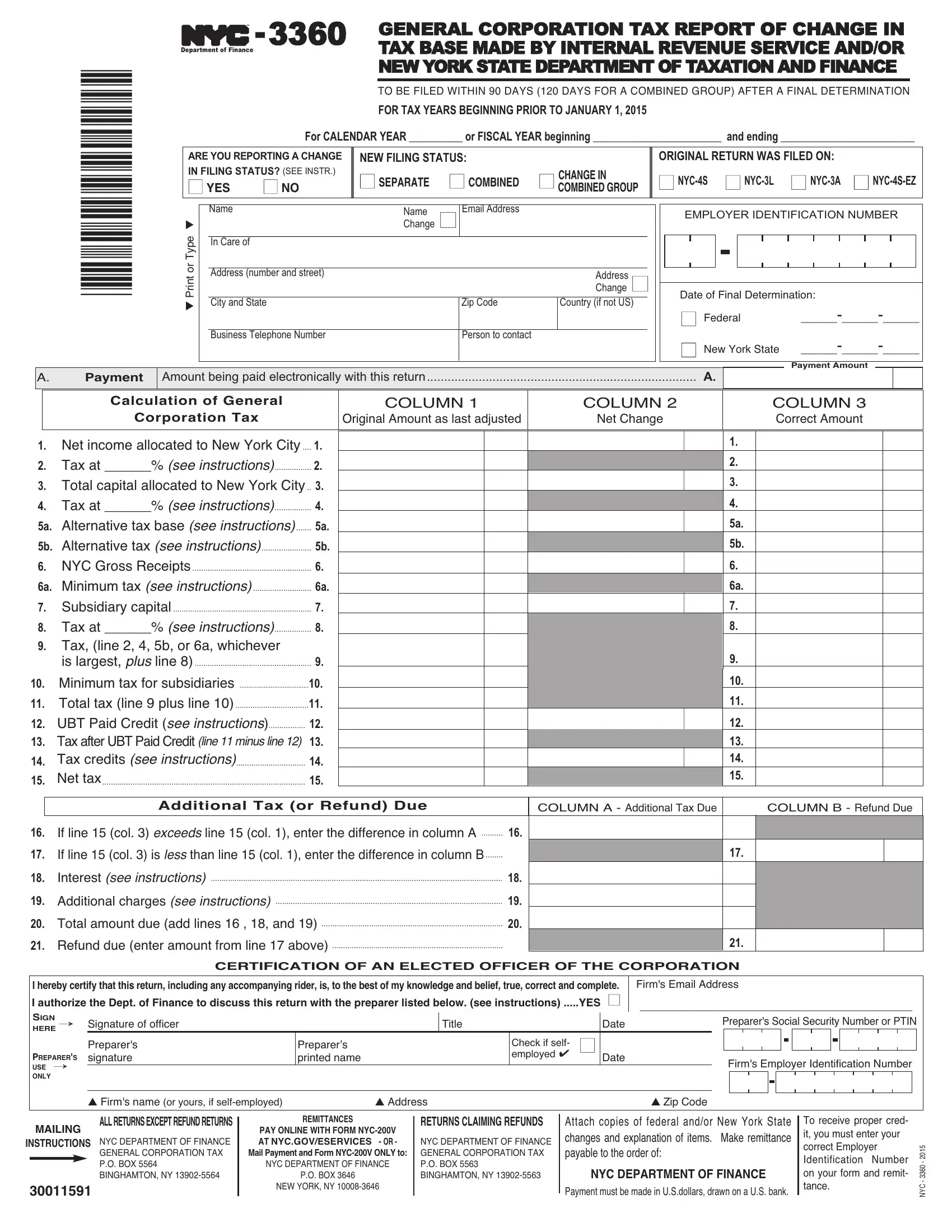

The NYC 3360 form, officially titled "General Corporation Tax Report of Change in Tax Base Made by Internal Revenue Service and/or New York State Department of Taxation and Finance," serves as a crucial document for corporations operating within New York City. It is designed to report adjustments made to a corporation's tax base by the IRS or the New York State Department of Taxation and Finance. This form must be filed within a specified deadline—90 days for most taxpayers, and 120 days for those filing a combined group report, following the final determination for tax years beginning before January 1, 2015. It encompasses various elements, including payment information, changes in filing status, and detailed tax calculation sections ranging from net income allocated to New York City, alternative tax base calculations, and any additional taxes or refunds due. Furthermore, it necessitates the submission of supporting documents, such as copies of federal or state changes, and it outlines the procedure for electronic or check payments. With its comprehensive instructions and significant implications for corporate taxes in New York City, mastery of the NYC 3360 is essential for businesses striving for compliance and accuracy in their financial reporting.

| Question | Answer |

|---|---|

| Form Name | Form Nyc 3360 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | ny base internal revenue online, 3360 tax, ny general base internal revenue, 2015 nyc tax change |