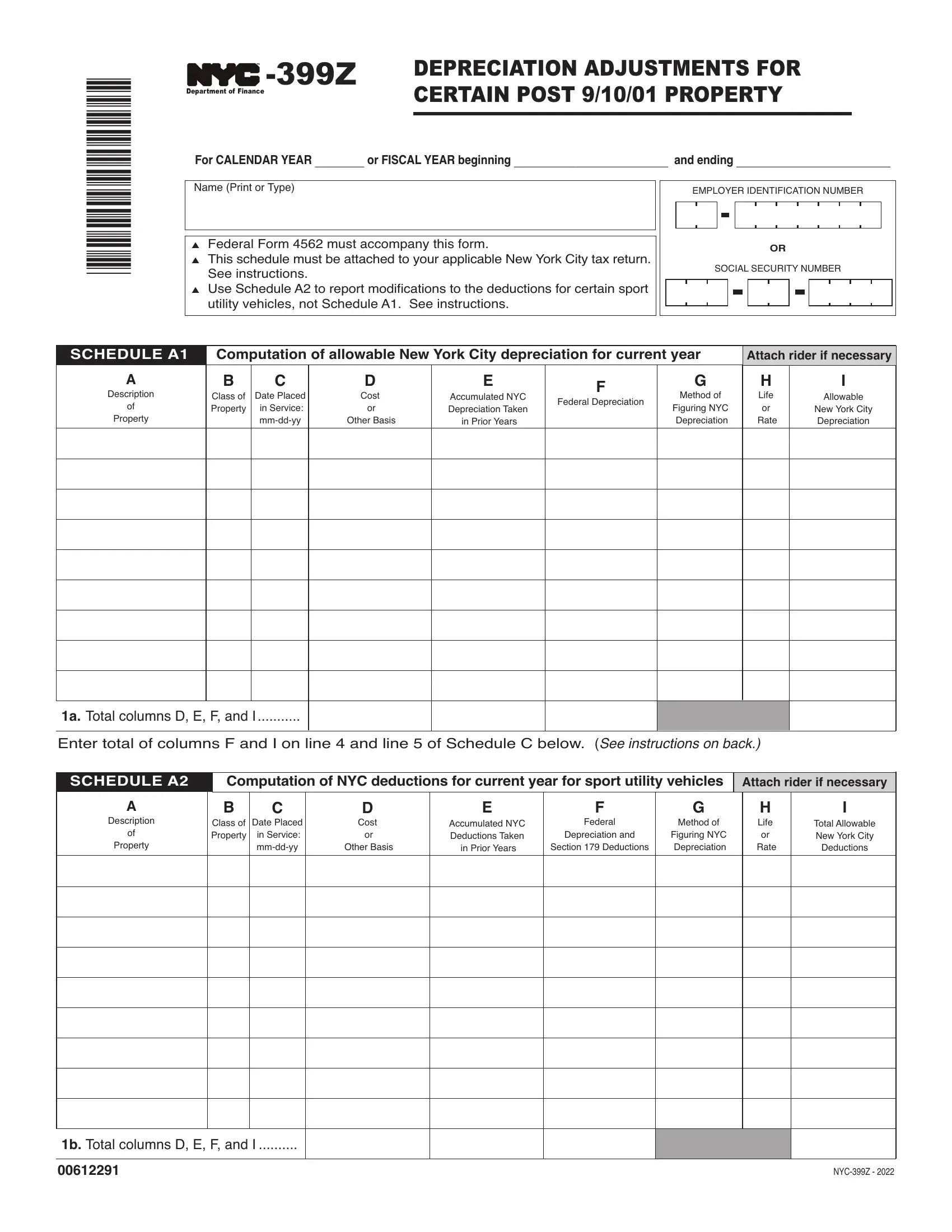

The Form NYC-399Z plays a pivotal role for corporations and unincorporated businesses operating within New York City, especially in the aftermath of changes following September 10, 2001. Tailored to address depreciation adjustments for certain property, this form intricately structures the computation of allowable New York City depreciation for qualifying properties not aligned with standard federal depreciation regulations introduced post-9/11. Specifically designed to cater to properties that would have been eligible for enhanced deductions under IRC §168(k) but are instead confined to depreciation calculations as if acquired on September 10, 2001, it covers not only the computation of allowable depreciation for the current year but also adjustments for sport utility vehicles and the disposition of properties. Form NYC-399Z requires entities to closely adhere to modifications in federal legislation regarding depreciation, including provisions from the Economic Stimulus Act of 2008 and subsequent adjustments through legislation like the 2015 PATH Act and TCJA—each altering the landscape of bonus depreciation. In conjunction with addressing depreciation computation, the form extends its relevance to adjustments required upon the disposition of property, ensuring that discrepancies between federal and New York City depreciation deductions are recalibrated for both entire net income and unincorporated business entire net income calculations. Beyond its primary function, this form encapsulates a unique provision for certain sport utility vehicles, responding to limitations imposed by IRC §280F and adjusting the allowable deduction for New York City tax purposes. Entities entangled in the specifics of qualifying property, qualified Resurgence Zone property, or the delineation of sport utility vehicles within the bounds of city and federal tax regulations, find Form NYC-399Z indispensable to comply with the nuanced tax landscape shaped significantly by post-9/11 legislative adjustments.

| Question | Answer |

|---|---|

| Form Name | Form Nyc 399Z |

| Form Length | 5 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 15 sec |

| Other names | Fillable Online 8B BANKING CORPORATION TAX CLAIM FOR ... |