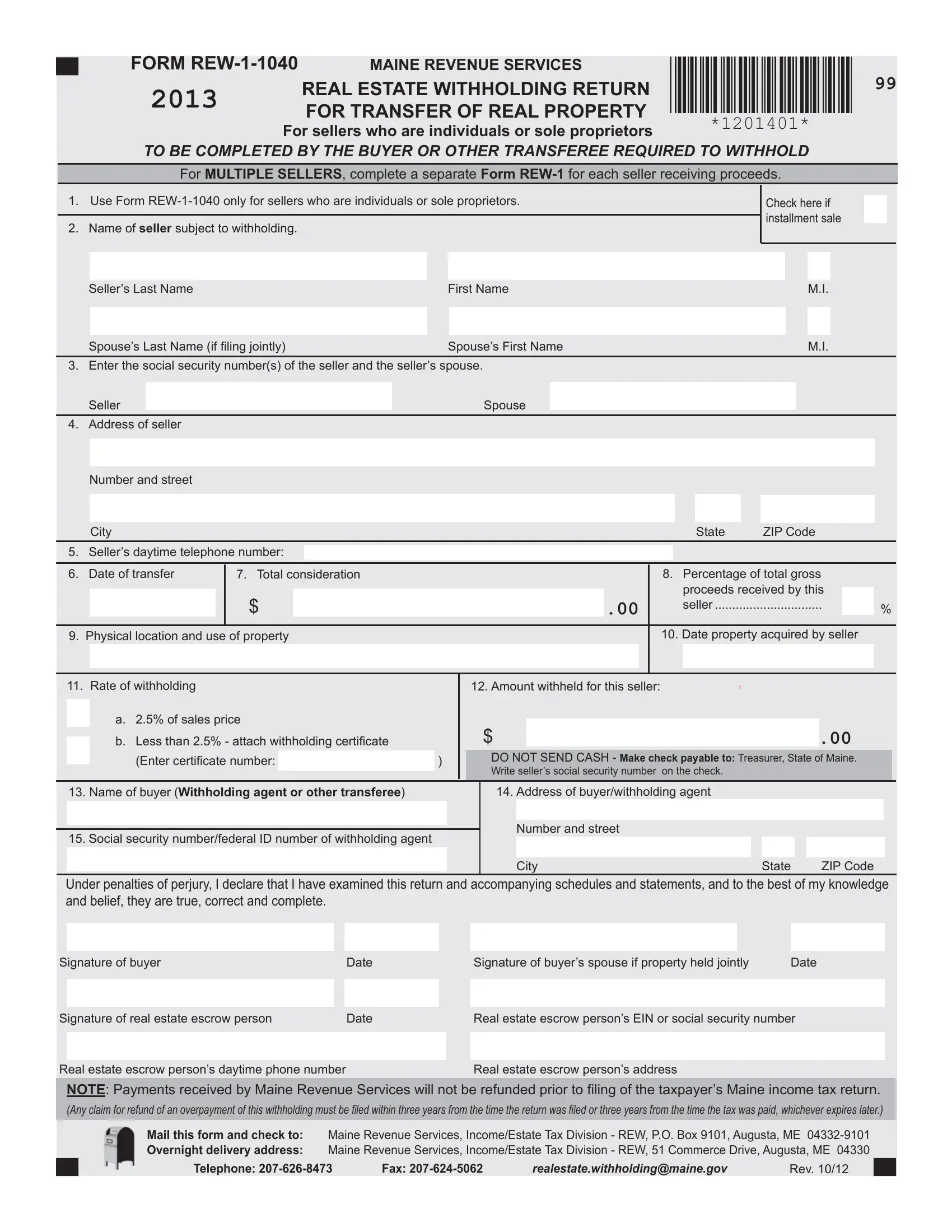

The Form REW-1-1040, issued by Maine Revenue Services, is a crucial document for the transfer of real property, especially involving sellers who are individuals or sole proprietors. This form plays a key role in the process by ensuring the proper withholding and remittance of state income tax when a nonresident of Maine sells real property within the state. Specifically designed to be filled out by the buyer or other transferee mandated to withhold, this form requires detailed information including the seller's name, social security number, and the details of the property transfer such as the date, total consideration, and the amount withheld. It's significant not only for its role in tax collection but also for its impact on both buyers and sellers in such transactions. Multiple sellers necessitate individual forms for each party receiving proceeds, highlighting the need for meticulous documentation in transactions involving real estate. Moreover, the form includes provisions for exceptions and the possibility of obtaining a withholding certificate to adjust the withholding rate, which demonstrates the tailored approach to handling diverse transaction scenarios. This form must be submitted promptly within 30 days of the property transfer, underscoring the importance of timeliness in fulfilling tax obligations. Additionally, it serves as a prerequisite for nonresident sellers to file a Maine income tax return, potentially to claim a refund for any overpayment of the real estate withholding amount. Its comprehensive structure not only facilitates tax compliance but also provides clear guidance to ensure the correct execution of real estate transactions under Maine law.

| Question | Answer |

|---|---|

| Form Name | Form Rew 1 1040 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | maine rew forms, MAINE, rew 1040 form, REW-1-1120 |