Navigating tax obligations can often feel like a maze, with various forms and deadlines to manage. Among these, the RPD-41096 form stands out for individuals, firms, or organizations within New Mexico seeking an extension of time to file their tax returns. As of its latest revision on June 23, 2016, by the State of New Mexico's Taxation and Revenue Department, this application becomes a critical tool in managing one's tax responsibilities effectively. The form's instructions highlight the process for applying for an extension, which must be done on or before the original or the extended due date of the return. Interestingly, if a federal automatic extension has already been obtained, New Mexico taxpayers might find relief in knowing that submitting Form RPD-41096 is not required. However, the waiver of penalties for late filing—as long as the return is filed and the tax due is paid by the extended due date—does not prevent the accumulation of interest on the tax due, which is assessed daily. This includes detailed instructions on the form's submission, reflecting a commitment to accommodating taxpayers who find themselves unable to meet the original filing deadline due to circumstances beyond their control. Despite these provisions, an inability to pay does not qualify as a valid reason for an extension, and tax professionals can't leverage workload as a justification either. The form makes provision for various tax return types and requires detailed reasoning for the extension request, alongside personal or organizational identification information, underscoring the state's tailored approach to tax administration.

| Question | Answer |

|---|---|

| Form Name | Form Rpd 41096 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | new mexico rpd 41096 filing instructions, 2018 nm tax forms, form 41096, nm form rpd 41096 |

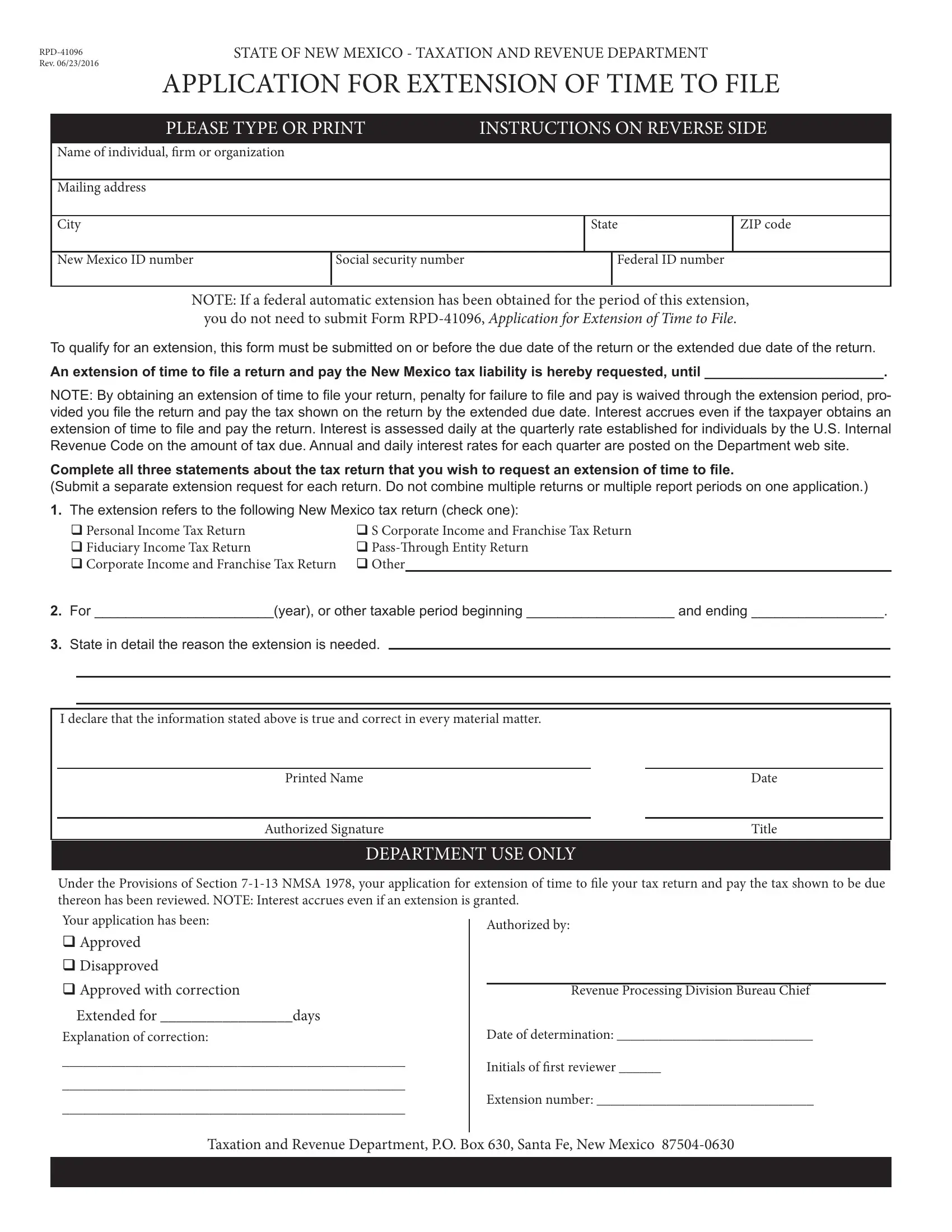

STATE OF NEW MEXICO - TAXATION AND REVENUE DEPARTMENT

APPLICATION FOR EXTENSION OF TIME TO FILE

PLEASE TYPE OR PRINT |

INSTRUCTIONS ON REVERSE SIDE |

||||

|

|

|

|

|

|

Name of individual, irm or organization |

|

|

|

|

|

|

|

|

|

|

|

Mailing address |

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

State |

ZIP code |

|

|

|

|

|

|

|

New Mexico ID number |

Social security number |

|

|

Federal ID number |

|

|

|

|

|

|

|

NOTE: If a federal automatic extension has been obtained for the period of this extension, you do not need to submit Form

To qualify for an extension, this form must be submitted on or before the due date of the return or the extended due date of the return.

An extension of time to ile a return and pay the New Mexico tax liability is hereby requested, until _______________________.

NOTE: By obtaining an extension of time to ile your return, penalty for failure to ile and pay is waived through the extension period, pro- vided you ile the return and pay the tax shown on the return by the extended due date. Interest accrues even if the taxpayer obtains an extension of time to ile and pay the return. Interest is assessed daily at the quarterly rate established for individuals by the U.S. Internal Revenue Code on the amount of tax due. Annual and daily interest rates for each quarter are posted on the Department web site.

Complete all three statements about the tax return that you wish to request an extension of time to ile.

(Submit a separate extension request for each return. Do not combine multiple returns or multiple report periods on one application.)

1.The extension refers to the following New Mexico tax return (check one):

Personal Income Tax Return |

S Corporate Income and Franchise Tax Return |

|

Fiduciary Income Tax Return |

|

|

Corporate Income and Franchise Tax Return |

Other |

|

2.For _______________________(year), or other taxable period beginning ___________________ and ending _________________.

3.State in detail the reason the extension is needed.

|

I declare that the information stated above is true and correct in every material matter. |

|

|

|

|

|

|

|

|

|

Printed Name |

|

Date |

|

|

|

|

|

|

|

Authorized Signature |

|

Title |

|

DEPARTMENT USE ONLY

Under the Provisions of Section

Your application has been:

Approved

Disapproved

Approved with correction

Extended for _________________days

Explanation of correction:

_________________________________________________

_________________________________________________

_________________________________________________

Authorized by:

Revenue Processing Division Bureau Chief

Date of determination: ____________________________

Initials of irst reviewer ______

Extension number: _______________________________

Taxation and Revenue Department, P.O. Box 630, Santa Fe, New Mexico

STATE OF NEW MEXICO - TAXATION AND REVENUE DEPARTMENT

EXTENSION OF TIME TO FILE

INSTRUCTIONS FOR

Form

By obtaining an extension of time to ile your return, penalty for failure to ile and pay is waived through the extension period, provided you ile the return and pay the tax shown on the return by the extended due date. However, interest accrues even if the taxpayer obtains an extension of time to ile and pay the return. To avoid interest, make a payment of the tax to be due by the original return due date. Interest is assessed daily at the quarterly rate established for individuals by the U.S. Internal Revenue Code on the amount of tax due. Annual and daily interest rates for each quarter are posted on the Department web site.

WHEN TO FILE: An application for extension of time to ile must be postmarked on or before the due date for iling the return or the extended due date of the return if a federal automatic extension or a New Mexico extension has been obtained. If a federal automatic extension is obtained, and you ile and pay the return by the extended due date allowed by the IRS, Form

HOW AND WHERE TO FILE: Complete this form and send it to the Taxation and Revenue Department, P.O. Box 630, Santa Fe, NM

REASONS FOR EXTENSIONS: The Taxation and Revenue Department will grant a reasonable extension of time for iling a return if the taxpayer iles a timely application which establishes that he is unable to ile the return by the due date because of circumstances beyond his control. Inability to pay the tax due is not suficient reason for issuance of an extension. Also, extensions will not be granted to tax practitioners because of excessive work load.

PERIOD FOR EXTENSIONS: Generally, a timely initial application for extension of time to ile will be automatically granted for a period not to exceed 60 days. Longer periods of time will not be granted unless suficient need for the extended period is clearly shown. Form

The secretary or delegate may, for good cause, extend in favor of an individual taxpayer or a class of taxpayers, for no more than a total of twelve (12) months, the date on which payment of any tax is required or on which any return required by provision of the Tax Administration Act, Sections

SIGNATURE: The application must be signed by the taxpayer or a duly authorized agent. If the taxpayer is unable to sign the application because of illness, absence, or other good cause, any person standing in close personal or business rela- tionship to him may sign the application. However, the signer must state the reasons for his signature and his relationship to the taxpayer.