The Form Rpd 41227, also known as the Fire and Explosion Incident Report, is a document used to report any fire or explosion-related incident. The form should be filled out as soon as possible after the incident occurs, and it must be submitted to the local fire department within 24 hours. The information collected on this form can help investigators determine the cause of the fire or explosion. detailed information about the incident, including what caused it and how it was extinguished. Any photos or video footage taken during or after the incident should also be included with the report.

| Question | Answer |

|---|---|

| Form Name | Form Rpd 41227 |

| Form Length | 5 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 15 sec |

| Other names | RPD-414 State of New Mexico - Taxation and Revenue ... |

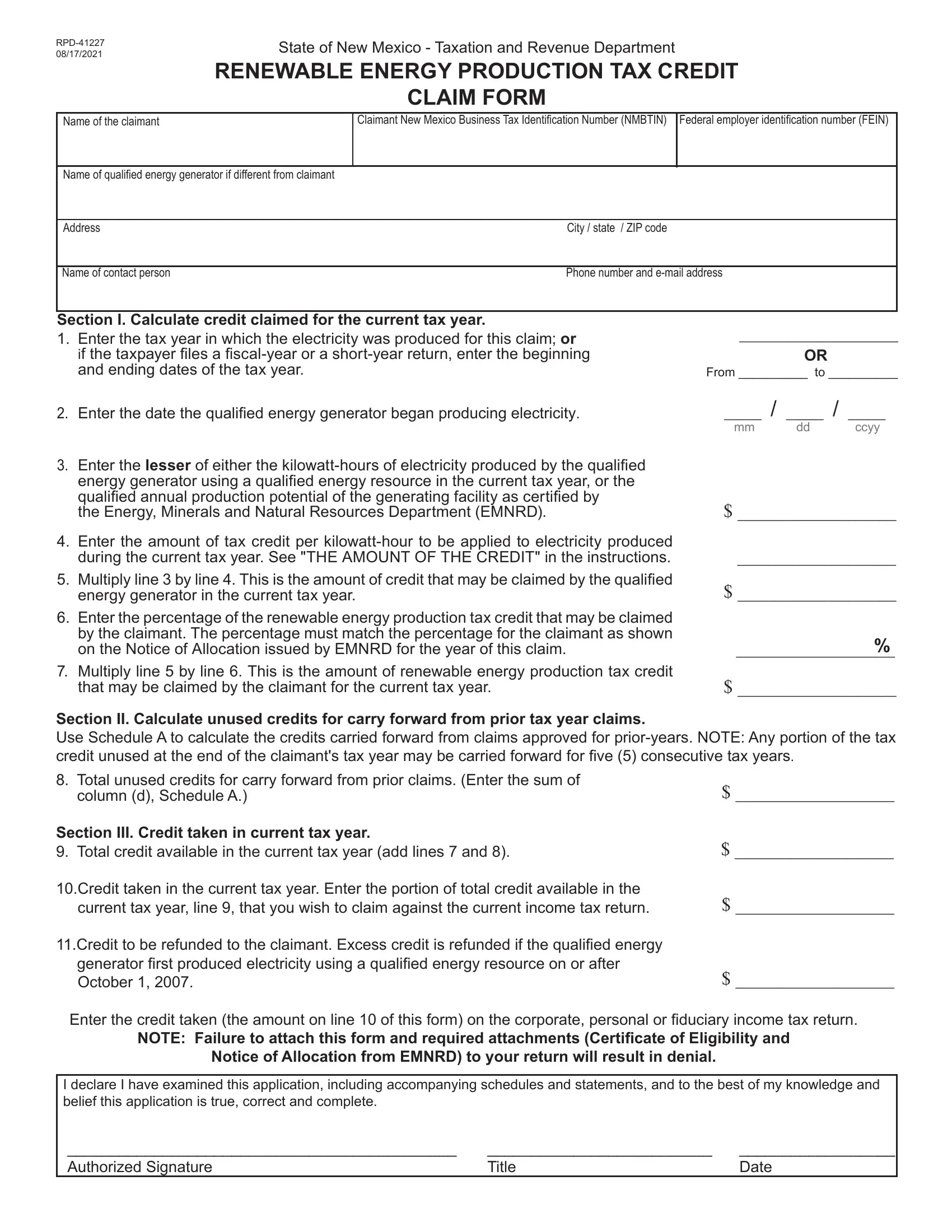

State of New Mexico - Taxation and Revenue Department

|

RENEWABLE ENERGY PRODUCTION TAX CREDIT |

|||

|

|

CLAIM FORM |

||

|

|

|

|

|

Name of the claimant |

|

Claimant New Mexico Business Tax Identification Number (NMBTIN) |

Federal employer identification number (FEIN) |

|

|

|

|

|

|

Name of qualified energy generator if different from claimant |

|

|

|

|

|

|

|

|

|

Address |

|

City / state / ZIP code |

||

|

|

|

|

|

Name of contact person |

|

Phone number and |

||

|

|

|

|

|

Section I. Calculate credit claimed for the current tax year.

1.Enter the tax year in which the electricity was produced for this claim; or

if the taxpayer files a

2.Enter the date the qualified energy generator began producing electricity.

3.Enter the lesser of either the

the Energy, Minerals and Natural Resources Department (EMNRD).

4.Enter the amount of tax credit per

5.Multiply line 3 by line 4. This is the amount of credit that may be claimed by the qualified energy generator in the current tax year.

6.Enter the percentage of the renewable energy production tax credit that may be claimed by the claimant. The percentage must match the percentage for the claimant as shown on the Notice of Allocation issued by EMNRD for the year of this claim.

7.Multiply line 5 by line 6. This is the amount of renewable energy production tax credit that may be claimed by the claimant for the current tax year.

Section II. Calculate unused credits for carry forward from prior tax year claims.

_________________

OR

From __________ to __________

____ / ____ / ____

mm dd ccyy

$ _________________

_________________

$ _________________

%

$ _________________

Use Schedule A to calculate the credits carried forward from claims approved for

8.Total unused credits for carry forward from prior claims. (Enter the sum of column (d), Schedule A.)

Section III. Credit taken in current tax year.

9. Total credit available in the current tax year (add lines 7 and 8).

10.Credit taken in the current tax year. Enter the portion of total credit available in the current tax year, line 9, that you wish to claim against the current income tax return.

11.Credit to be refunded to the claimant. Excess credit is refunded if the qualified energy generator first produced electricity using a qualified energy resource on or after October 1, 2007.

$_________________

$_________________

$_________________

$ _________________

Enter the credit taken (the amount on line 10 of this form) on the corporate, personal or fiduciary income tax return.

NOTE: Failure to attach this form and required attachments (Certificate of Eligibility and

Notice of Allocation from EMNRD) to your return will result in denial.

I declare I have examined this application, including accompanying schedules and statements, and to the best of my knowledge and belief this application is true, correct and complete.

_____________________________________________ |

__________________________ |

__________________ |

Authorized Signature |

Title |

Date |

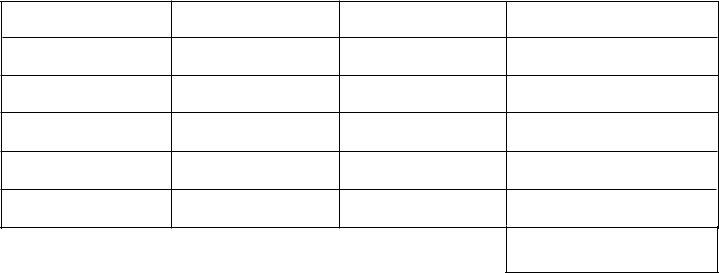

State of New Mexico - Taxation and Revenue Department

RENEWABLE ENERGY PRODUCTION TAX CREDIT

Schedule A

To complete Section II of the claim Form

(a)Tax year of previous claim. For each credit claimed in a previous tax year with unused credit available for carry forward, enter the tax year in which the credit was first claimed. Enter the

(b)Credit claimed. For each credit claimed in column (a), enter the amount of credit that was approved for that tax year.

(c)Total credit taken in previous tax years. For each credit amount listed in column (b), enter the total amount of credit applied to personal or corporate income tax liabilities in prior year returns.

(d)Unused credit available for carry forward from prior claims. Subtract column (c) from column (b) and enter the dif- ference.

Total unused credit available for carry forward. Enter the sum of all amounts in column (d). Also enter this amount on line 8 of Form

You must apply credit approved to be claimed in the tax year first. If the credit amount approved to be claimed in a tax year is less than the personal or corporate income tax liability for that year, you may apply unused credit available for carry forward next. When applying excess credits available for carry forward, apply the oldest credit first.

NOTE: Taxpayers who have received approval for tax credits for facilities that first produced electricity on, or after, October 1, 2007, can claim a refund for any credits in excess of their tax liability.

(a)Tax year of previous claim

(b) Credit claimed

(c)Total credit taken in previous tax years

(d)Unused credit for carry forward from prior claims [(b) - (c)]

Total unused credit available for carry forward. Enter the sum of all amounts in column (d). Also enter this amount on line 8 of Form

State of New Mexico - Taxation and Revenue Department

RENEWABLE ENERGY PRODUCTION TAX CREDIT

CLAIM FORM INSTRUCTIONS

Page 1 of 3

ABOUT THIS CREDIT: For tax years beginning on or after July 1, 2002, a corporate taxpayer who owns a qualified en- ergy generator is eligible for a tax credit in an amount equal to one cent ($.01) per

for more than six consecutive months in a year or until the facility's

Beginning January 1, 2008, the 2007 New Mexico Legislature

expanded the credit as follows:

•The credit is allowed only for facilities that first produce electricity before January 1, 2018.

•The credit is expanded to includetaxpayers in the Income

Tax Act.

•A variable rate of credit is added for electricity produced using solar energy.

•The definition of biomass was amended to include a variety of organic materials that are available on a renewable basis including landfill gas and municipal solid waste.

•The minimum size of an eligible facility for the credit is reduced from ten megawatts to one megawatt.

•The maximum amount of electricity that can be certified as eligible for the credit is increased for solar facilities only. An additional 500,000 megawatt hours (MWh) of solar- generated power

•Taxpayers who have received approval for tax credits for facilities that first produced electricity on, or after, October 1, 2007, can claim a refund for any credits in excess of their tax liability.

•The total amount of electricity that can qualify for the corpo- rate and individual income tax credits is two million MWh, plus an additional 500,000 MWh for solar facilities.

Beginning July 1, 2021, the 2021 New Mexico Legislature clarified that the credit is for 120 months in place of ten years. It also added an 11th taxable year credit rate for

rescource.

The remaining instructions have been modified to include

current law.

WHO MAY CLAIM THE CREDIT: A taxpayer who files a New Mexico personal income tax and who is not a dependent of another taxpayer or who files a New Mexico personal, cor- porate or fiduciary tax return and who:

(1) holds title to a qualified energy generator that first pro-

duced electricity on or before January 1, 2018; or

(2)leases such a facility from a county or municipality under

the authority of an industrial revenue bond and if the qualified energy generator first produced electricity on or before January 1, 2018,may claim all or a portion of the renewable energy production tax credit.

A taxpayer may be allocated all or a portion of the right to claim the credit without regard to proportional ownership interest if:

1.the taxpayer owns an interest in a business entity that is taxed federally as a partnership,

2.the business entity:

a.would qualify for the renewable energy production tax credit,

b.owns an interest in a business entity that is also taxed

as a partnership and that would qualify for the renewable energy production tax credit; or

c. owns, through one or more intermediate business enti- ties that are each taxed as a partnership, an interest in the business entity described in the previous paragraph (b).

3.the taxpayer and all other taxpayers allocated a right to claim the credit own collectively at least five percent inter- est in a qualified energy generator;

4.the business entity provides notice of the allocation and the taxpayer's interest to the New Mexico Energy, Minerals and Natural Resources Department (EMNRD); and

5.EMNRD certifies the allocation in writing to the taxpayer.

To allocate or apportion the right to claim all or a portion of the renewable energy production tax credit a Notice of Allo-

cation for each taxable year the credit is claimed need to be submitted to EMNRD for approval and once approved it will need to be provided to the Taxation and Revenue Department (TRD). Contact Information for EMNRD: New Mexico Energy, Minerals and Natural Resources Department, Energy Con- servation and Management Division, P.O. Box 6429, Santa Fe, NM

or email emnrd.taxcredits@state.nm.us

THE AMOUNT OF THE CREDIT: A taxpayer is eligible for the renewable energy production tax credit for 120 consecutive months beginning with the date the qualified energy genera- tor begins producing electricity. Compute the credit based on

actual electricity produced for each of the taxable years that is within the 120 months.

For a qualified energy generator using a wind- or biomass- derived qualified energy resource, the amount of tax credit is the lesser of $.01 per

For a qualified energy generator using a

State of New Mexico - Taxation and Revenue Department

RENEWABLE ENERGY PRODUCTION TAX CREDIT

CLAIM FORM INSTRUCTIONS

Page 2 of 3

the generator first produces electricity using the qualified energy resource. The chart below shows the amount of tax credit for the first 200,000

produces electricity.

or email emnrd.taxcredits@state.nm.us

Once the certificate of eligibility and the Notice of Allocation, is approved by EMNRD you may submit the approved Notice of Allocation to the New Mexico Taxation and Revenue De- partment (TRD) along with this completed form, see below

Tax Credit per kilowatt hour |

Tax year |

|

|

$.015 |

1st |

$.02 |

2nd |

$.025 |

3rd |

$.03 |

4th |

$.035 |

5th |

$.04 |

6th |

$.035 |

7th |

$.03 |

8th |

$.025 |

9th |

$.02 |

10th |

$.015 |

11th |

The total renewable energy tax credit allowed by all claimants may not exceed the limits set for the renewable energy tax credit allowed for the qualified energy generator. Credit may

not be claimed with respect to the same electricity produc- tion under both Section

A facility's credit for a tax year is limited to the qualified an- nual production potential of the generating facility as certified by EMNRD.

APPLYING FOR CERTIFICATION FROM EMNRD: EMNRD certifies the eligibility of an energy generator and the estimated annual production potential of the generating

for more information.

HOW TO CLAIM THE CREDIT:

A taxpayer may claim the renewable energy production tax credit by submitting to TRD, a completed Form

New Mexico Renewable Energy Production Tax Credit Claim Form, the Certificate of Eligibility issued by EMNRD, the No- tice of Allocation approved by EMNRD and documentation showing the amount of electricity produced by the facility in the taxable year. TRD may require additional information to verify eligibility. If the requirements have been complied with, TRD shall approve the claim and any avaliable payment for the renewable energy production tax credit as indicated on the claim form and the associated personal, corporate or fiduciary tax return Schedule CR for the taxable year.

The credit may be deducted from a taxpayer's New Mexico corporate, personal, and fiduciary income tax liability for the tax year for which the credit is claimed. If the amount of tax credit exceeds the taxpayer's personal, corporate, or fiduciary

income tax liability for the tax year:

(1)the excess may be carried forward for a period of five tax years; or

(2)if the tax credit was issued with respect to a qualified energy generator that first produced electricity using a qualified energy resource on or after October 1, 2007, the excess shall be refunded to the taxpayer.

facility. The facility's estimated annual production potential

limits the facility's energy production eligible for the tax credit

for the tax year. The total amount of electricity that may be produced annually by all qualified energy generators that are certified may not exceed a total of two million megawatt- hours plus an additional 500,000

will be considered in the order received.

Note: If allocating the right to claim all or a portion of the re- newable energy production tax credit, a Notice of Allocation will have to be approved for each taxable year the qualified energy generator produces energy and qualfies for the credit.

To obtain a certificate of eligibility and an Notice of Allocation for the right to claim all or a portion of the renewable energy production tax credit contact: New Mexico Energy, Minerals and Natural Resources Department, Energy Conservation and Management Division, P.O. Box 6429, Santa Fe, NM

Renewable energy production tax credit approved to be claimed for the current tax year must be applied first. If the

credit amount approved to be claimed in a tax year is less

than the personal or corporate income tax liability for that year, you may apply unused credit available for carry forward. When applying unused credits available for carry forward, apply the oldest credit first.

Report the credit taken on the New Mexico personal income tax return, corporate income tax return or fiduciary income tax return. Submit Form

Energy Production Tax Credit Claim Form, and attachments with your income tax return.

Once a taxpayer has been granted a renewable energy pro- duction tax credit for a given facility, that taxpayer shall be allowed to retain the facility's original date of application for tax credits for that facility until either the facility goes out of

production for more than six consecutive months in a year or

until the facility's 120 months eligibility has expired.

State of New Mexico - Taxation and Revenue Department

|

RENEWABLE ENERGY PRODUCTION TAX CREDIT |

Page 3 of 3 |

||

|

CLAIM FORM INSTRUCTIONS |

|||

|

|

|||

|

|

(f) |

landfill gas, wastewater treatment gas and biosolids, |

|

IMPORTANT DEFINITIONS: |

|

including organic waste byproducts generated during |

||

Biomass means organic material that is available on a re- |

|

the wastewater treatment process; and |

|

|

newable or recurring basis, including: |

(g) |

segregated municipal solid waste, excluding tires and |

||

(a) |

|

medical and hazardous waste. |

|

|

|

residues, forest thinnings, slash, brush, |

|

|

|

|

value materials or undesirable species, salt cedar and |

Qualified energy generator means an electric generating |

||

|

other phreatophyte or woody vegetation removed from |

facility with at least one megawatt generating capacity located |

||

|

river basins or watersheds and woody material harvested |

in New Mexico that produces electricity using a qualified |

||

|

for the purpose of forest fire fuel reduction or forest health |

energy resource and the electricity produced is sold to an |

||

|

and watershed improvement; |

unrelated person. |

|

|

(b) |

|

|

|

|

|

vineyard, grain or crop residues, including straw and |

Qualified energy resource means a resource that generates |

||

|

stover, aquatic plants and agricultural processed co- |

electrical energy by means of a fluidized bed technology or |

||

|

products and waste products including fats, oils, greases, |

similar |

||

|

whey and lactose; |

eration technology that has substantial |

||

(c) |

animal waste, including manure and slaughterhouse and |

potential and that uses only solar light, solar heat, wind, or |

||

|

other processing waste; |

biomass. |

|

|

(d) |

solid woody waste materials, including landscape or right- |

|

|

|

|

|

|

|

|

|

waste pallets, crates and manufacturing, construction |

|

|

|

|

and demolition wood wastes, excluding |

|

|

|

|

chemically treated or painted wood wastes and wood |

|

|

|

|

contaminated with plastic; |

|

|

|

(e) |

crops and trees planted for the purpose of being used to |

|

|

|

|

produce energy; |

|

|

|

POINTS OF CONTACT:

New Mexico Energy, Minerals and Natural Resources Department Energy Conservation and Management Division

P.O. Box 6429

Santa Fe, NM

or email emnrd.taxcredits@state.nm.us

New Mexico Taxation and Revenue Department Business Credit Claim Unit

P.O. Box 630

Santa Fe, NM