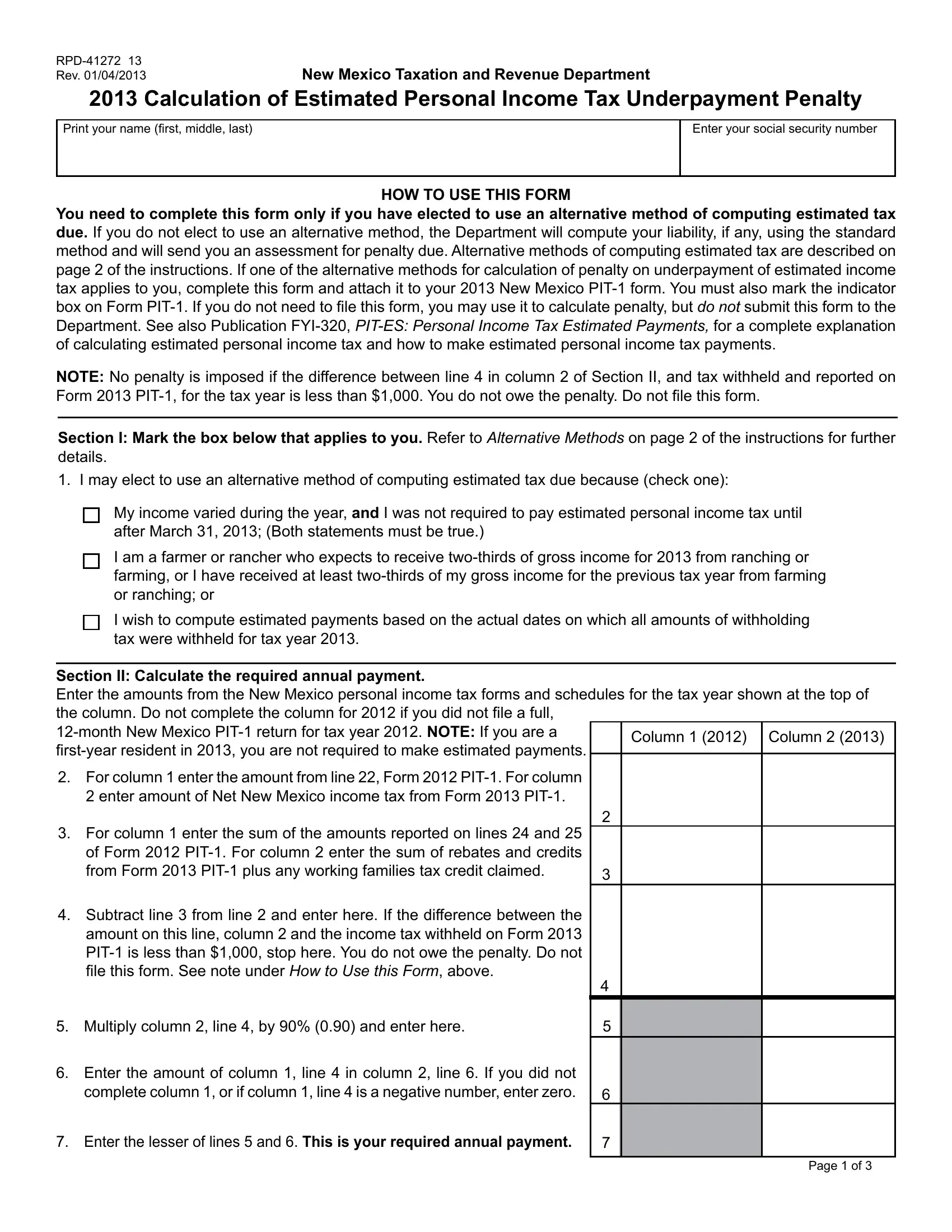

The RPD-41272 13 form, introduced by the New Mexico Taxation and Revenue Department as of January 4, 2013, is an essential document for individuals who choose to calculate their estimated personal income tax underpayment penalty using an alternative method. Designed to offer options for those whose financial circumstances do not align with the standard computation method, the form requires individuals to detail their estimated tax due, explaining various options for calculation on the second page of the instructions. Particularly beneficial for taxpayers with uneven income throughout the year, farmers, ranchers, or those who base their estimated payments on the actual dates of withholding tax, this form, when attached to the New Mexico PIT-1 form, serves as a declaration of opting for an alternative calculation method. It is critical to mark the corresponding indicator box on the PIT-1 form to alert the Department of this choice. Moreover, the form stipulates conditions under which no penalty is imposed, chiefly if the difference between the calculated tax and the amount withheld is less than $1,000, simplifying compliance for taxpayers. The document thoroughly guides through calculating required annual payments and installment amounts, culminating in the penalty computation for those who underpay or delay their estimated tax payments. With clear instructions for each section, including detailed formulae for penalty calculation, the RPD-41272 13 form is instrumental for taxpayers seeking to navigate their estimated tax payments effectively.

| Question | Answer |

|---|---|

| Form Name | Form Rpd 41272 13 |

| Form Length | 5 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 15 sec |

| Other names | Underpayment, 41272, IRC, New_Mexico |