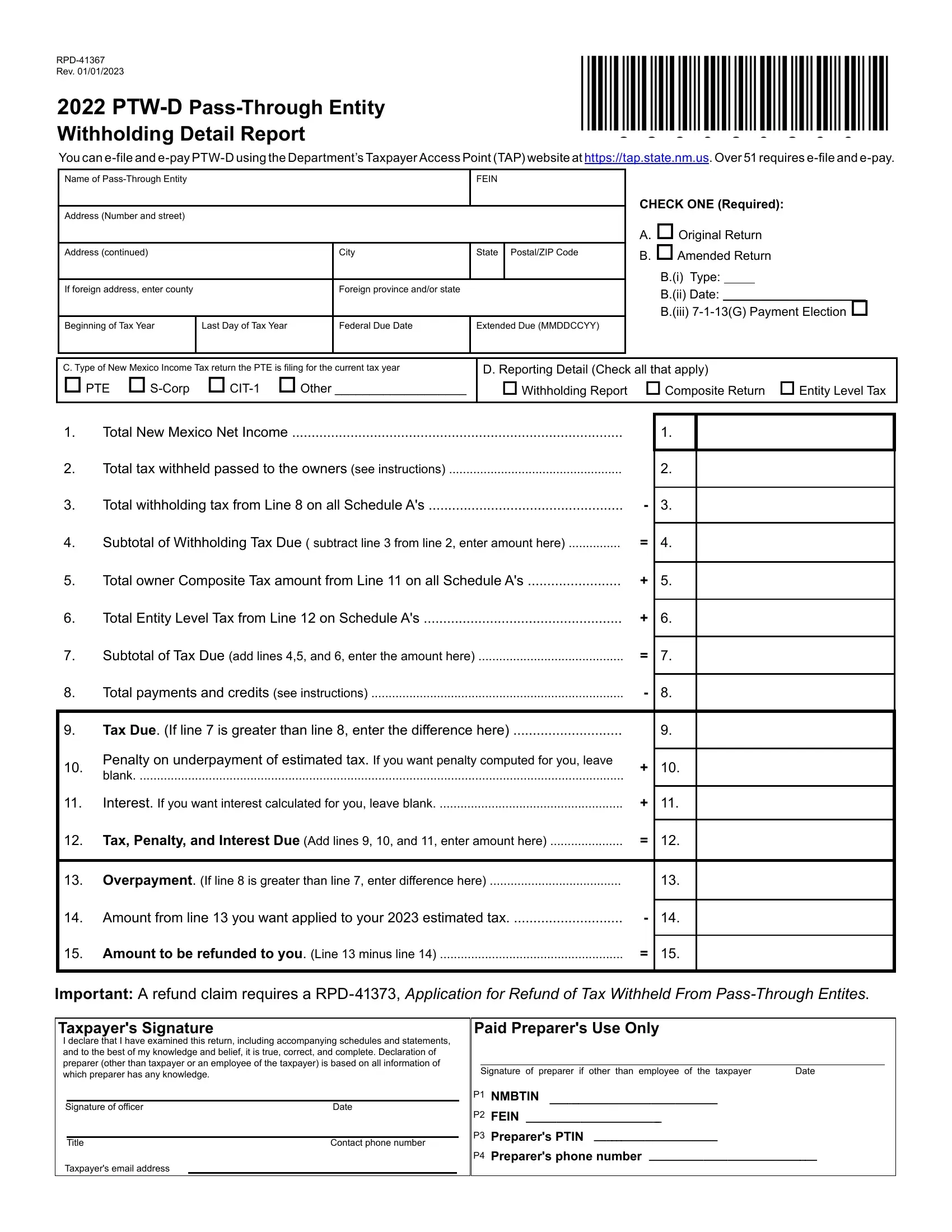

In the sprawling landscape of tax documentation and compliance, the RPD-41367 form emerges as a vital instrument for pass-through entities (PTEs) in New Mexico, navigating the specifics of withholding detail and tax reporting. The essence of this form can be distilled into its core purpose: to furnish a detailed account of withholding from the allocable net income of owners, partners, or members, thereby ensuring the accurate and timely remittance of taxes to the New Mexico Taxation and Revenue Department. Revised on August 19, 2019, it underscores state tax obligations for both resident and non-resident owners, embedding stipulations for electronic and paper filing predicated on the number of New Mexico payees a PTE reports. Furthermore, the form delineates the operational aspects of tax payments, adjustments for amended returns, penalties, and interest alongside directions for claiming refunds through the RPD-41373 form. Instructions integrated within or accompanying the RPD-41367 detail the procedural mechanics of filing, from the online submission nuances via the Taxpayer Access Point (TAP) website to specific directions for paper filers, encapsulating a comprehensive guide for PTEs to navigate their fiscal responsibilities. This form, therefore, not only acts as a submission vehicle but also as a blueprint for compliance, reflecting the broader regulatory framework governing pass-through entity taxation in New Mexico.

| Question | Answer |

|---|---|

| Form Name | Form Rpd 41367 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | nm rpd 41367, new mexico form rpd 41367 instructions 2020, new mexico form rpd 41367, nm form rpd 41367 |