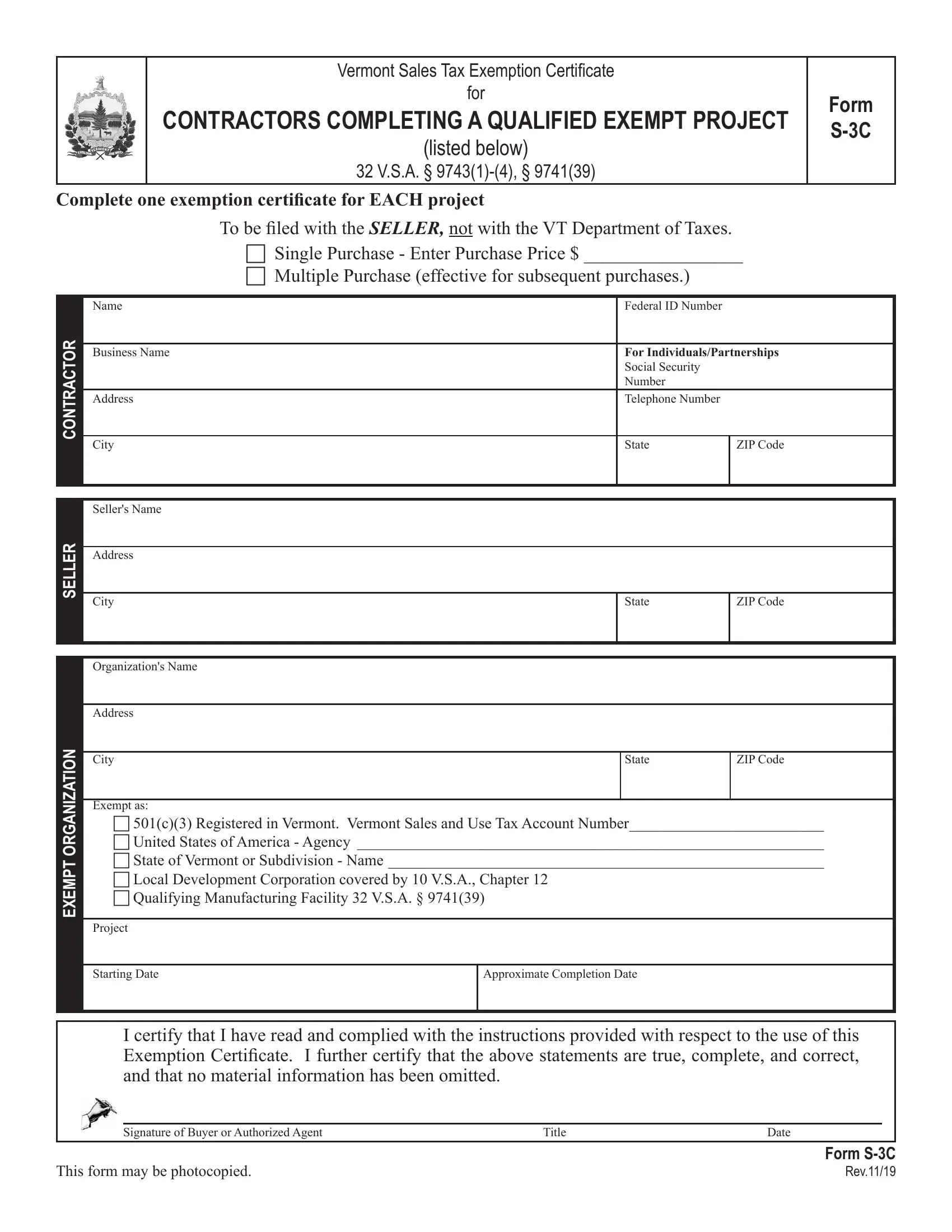

In the realm of construction and contracting within Vermont, navigating tax obligations with precision is paramount, and the S-3C Vermont form emerges as a critical tool in this endeavor for contractors working on qualified exempt projects. This form, rooted in the statutes 32 V.S.A. § 9743(1)-(4), § 9741(39), serves as a Sales Tax Exemption Certificate, enabling contractors to purchase materials and supplies without bearing the brunt of sales tax, provided these purchases are destined for specific exempt projects. It is meticulously designed to cater to a distinct category of purchases, whether they are single or multiple, and requires thorough information from the contractor, including Federal ID or Social Security Number, business details, and specifics about the seller and exempt organization benefitted by the project. Notably, the exemption only applies to tangible personal property that will be integrated into the real estate or consumed in the course of the job, with a clear directive that any deviation, such as the use of materials in a taxable project or purchases of equipment and tools, mandates the payment of use tax. The form underlines the importance of compliance and the need for contractors to furnish it to sellers, not to the Vermont Department of Taxes, embodying a safeguard for both parties through the stipulation of "good faith" acceptance. Furthermore, it delineates qualifying organizations and projects that can benefit from this exemption, highlighting the nuanced criteria that separate eligible from ineligible endeavors and ensuring that the form's misuse is curbed. Emphasized within the document is the seller's responsibility to retain these certificates as proof of tax-exempt sales, outlining a framework designed to streamline tax exemption processes for contractors, sellers, and qualifying organizations while ensuring adherence to Vermont's tax legislation.

| Question | Answer |

|---|---|

| Form Name | Form S 3C Vermont |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | vermont agricultrail tax exempt form, state of vermont tax exempt form, tax exempt form vermont, vermont sales tax exempt form |

Vermont Sales Tax Exemption Certificate

for

CONTRACTORS COMPLETING A QUALIFIED EXEMPT PROJECT

(listed below)

32 V.S.A. §

FORM

Complete one exemption certificate for EACH project

|

|

To be filed with the SELLER, not with the VT Department of Taxes. |

|

||

|

|

c Single Purchase - Enter Purchase Price $ _________________ |

|||

|

|

c Multiple Purchase (effective for subsequent purchases.) |

|

||

|

|

|

|

|

|

|

Name |

|

Federal ID Number |

|

|

CONTRACTOR |

|

|

|

||

Business Name |

|

For Individuals/Partnerships |

|||

|

|

Social Security |

|

||

|

|

Number |

|

||

Address |

|

Telephone Number |

|

||

|

|

|

|

|

|

|

City |

|

State |

|

ZIP Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

Seller's Name |

|

|

|

|

SELLER |

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

ZIP Code |

|

|

|

|

|||

|

|

|

|

|

|

ORGANIZATION

Organization's Name

Address

City

Exempt as:

State

ZIP Code

EXEMPT

c501(c)(3) Registered in Vermont. Vermont Sales and Use Tax Account Number_________________________

cUnited States of America - Agency ____________________________________________________________

cState of Vermont or Subdivision - Name ________________________________________________________

cLocal Development Corporation covered by 10 V.S.A., Chapter 12

cQualifying Manufacturing Facility 32 V.S.A. § 9741(39)

Project

Starting Date

Approximate Completion Date

I certify that I have read and complied with the instructions provided with respect to the use of this Exemption Certificate. I further certify that the above statements are true, complete, and correct, and that no material information has been omitted.

Signature of Buyer or Authorized Agent |

Title |

Date |

FORM

This form may be photocopied. |

Rev.11/19 |

Instructions for Use of the Certificate of Exemption for Contractors (Form

(For use only in completion of qualified projects for exempt organizations)

All tangible personal property purchased by a contractor is taxable as the contractor is considered to be the

•When the contractor is working with a qualifying exempt organization

•When the contractor is working on a specific qualifying exempt project

Tangible personal property exempted from tax must be incorporated into the real estate, or the supplies must be used or consumed on the job. If the contractor buys materials or supplies exempt from tax but uses them later in a taxable project, the contractor must pay use tax on those materials and supplies. Purchases of equipment and tools used by the contractor are subject to tax.

Qualifying Organizations & Projects

A qualifying organization contracts to construct, reconstruct, alter, remodel, or repair any building structure or public works project owned by the Federal government, State of Vermont (and its agencies and subdivisions), or a 501(c)(3) as designated by the Internal Revenue Service and registered with the Vermont Department of Taxes. Please note that many nonprofit organizations, such as civic, social, and fraternal organizations, are not 501(c)(3)s and not all 501(c)(3)s projects qualify for exemption. To qualify, the project must be used exclusively for public purposes, and the project contract must be granted by an exempt organization. Turnkey projects are not exempt, even if the ultimate owner may be an exempt organization.

Qualifying Manufacturing Facility

Under 32 V.S.A. § 9741(39), Sales of building materials within any three consecutive years in excess of $1,000,000.00 in purchase value used in the construction, renovation, or expansion of facilities which are used exclusively, except for isolated or occasional uses, for the manufacture of tangible personal property for sale.

Acceptance in “Good Faith”

A seller who accepts an exemption certificate in “good faith” is relieved of liability for collection or payment of

the Vermont Sales and Use Tax otherwise due on tangible personal property covered by the certificate. Good faith depends upon a consideration of all the conditions surrounding the transaction. To receive an exemption in good faith, a seller is presumed to be familiar with the law and the regulations pertinent to the business in which the seller deals. In order for good faith to be established, all of the following conditions must be met:

a.The buyer must present the certificate prior to or at the time of the purchase of the property.

b.The certificate must contain no statement or entry which the seller knows, or has reason to know, is false or misleading.

c.The certificate is on an exemption form issued by the Vermont Department of Taxes or a form with substantially identical language.

d.The certificate must be dated and complete and in accordance with published instructions.

e.The Vermont Sales and Use Tax account number is provided on the certificate where applicable

f.The property to be purchased is of a type ordinarily used by the buyer for the purpose described on the certificate.

Improper Certificate/Lack of Certificate

Sales of tangible personal property subject to tax which are not supported by properly executed exemption certificates are taxable retail sales. The burden of proof that the tax was not required to be collected is upon the SELLER.

Retention of Certificates by the Seller

Sellers must retain exemption certificates for at least three years from the date of the last sale covered by the certificate to document why tax was not collected from the buyer.

Multiple Purchase Exemption Certificates

If the buyer presents a “Multiple Purchase” exemption certificate to the seller, it may be used only when purchasing tangible personal property for use on the qualified exempt project as noted on this exemption certificate. For each purchase covered by the exemption certificate, the sales slip or invoice must show the buyer’s name and address sufficient to link the purchase to the exemption certificate on file.

Other types of exemption certificates that may be applicable are available on our website at: www.tax.vermont.gov. For questions regarding how these exemption certificates may be properly applied, please contact the Vermont Department of Taxes at (802)

FORM

Page 1 of 1 Rev. 11/19