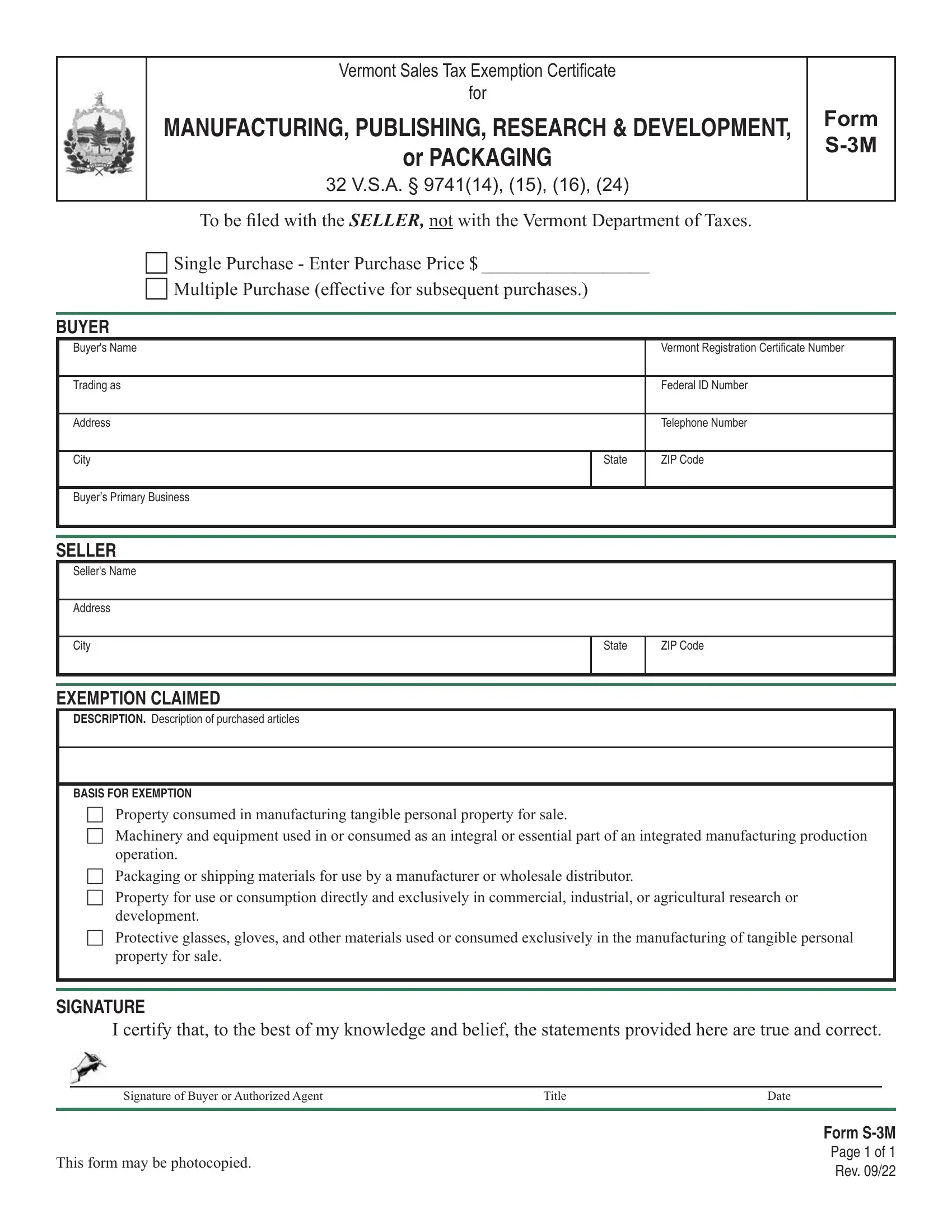

Navigating the intricacies of tax exemptions in Vermont, particularly for businesses involved in manufacturing, publishing, research and development, or packaging, requires a comprehensive understanding of the Vermont Sales Tax Exemption Certificate, otherwise known as Form S-3M. This critical document serves as a cornerstone for entities looking to benefit from tax exemptions on purchases that are integral to their operational processes. By meticulously outlining the conditions under which tangible personal property and certain services are exempt from sales tax, the form facilitates transactions that are essential for the manufacturing, printing, publishing, and packaging sectors. Designed to be filed with the seller rather than the Vermont Department of Taxes, the form caters to both single and multiple purchase agreements, demanding details like the buyer's name, primary business, and federal ID number, alongside specifying the exemption claims which range from machinery used directly in manufacturing to packaging materials for wholesale distributors. With provisions that delve into the nitty-gritty of what constitutes a legitimate claim for exemption, the form underscores the importance of good faith between buyer and seller, ensuring that all transactions are conducted with the utmost integrity and in full compliance with Vermont's tax laws. Furthermore, it sheds light on the prerequisite of retaining certificates and the protocol for additional purchases, painting a comprehensive picture of the legislative landscape surrounding tax-exempt purchases in Vermont.

| Question | Answer |

|---|---|

| Form Name | Form S 3M Vermont |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | vt tax exemption certificate, vermont tax exemption certificate, vt s 3m fillable, s 3m |

|

Vermont Sales Tax Exemption Certificate |

|

|

for |

FORM |

|

MANUFACTURING, PUBLISHING, RESEARCH & DEVELOPMENT, |

|

|

||

|

OR PACKAGING |

|

|

|

|

|

32 V.S.A. §9741(14), (15), (16), (24) |

|

|

|

|

TobefiledwiththeSELLER,notwiththeVTDepartmentofTaxes.

χ

χMultiplePurchase(effectiveforsubsequentpurchases.)

BUYER

Buyer’s

Name

Tradingas

Address

City

Buyer’sPrimary Business

VT Registration Certificate Number

Federal ID

Number

State |

Zip |

|

|

|

Seller’s |

|

|

|

SELLER |

Name |

|

|

|

Address |

|

|

||

City |

State |

Zip |

||

|

||||

|

|

|

|

Exemptionclaimed

CLAIMED |

χ Property consumed in manufacturing tangible |

χ Packaging or shipping materials for use by a |

|

personalpropertyforsale. |

manufacturerorwholesaledistributor. |

||

EXEMPTION |

|||

χ Machineryandequipmentuseddirectlyandex- |

χ Propertyforuseorconsumptiondirectlyandex- |

||

clusively in the manufacture, printing, or pub- |

clusively in commercial, industrial, or agricul- |

||

lishingoftangiblepersonalpropertyforsale. |

turalresearchordevelopment. |

||

|

|

I certify that, to the best of my knowledge and belief, the statements provided here are true and correct.

SignatureofBuyerorAuthorizedAgent |

Title |

Date |

|

|

|

|

|

FORM |

Thisformmaybephotocopied. |

|

Rev. 5/03 |

INSTRUCTIONSFORMANUFACTURING,PUBLISHING,RESEARCH&DEVELOPMENT,

1.Tangiblepersonalpropertyispropertywhichcanbeseen,touched,andmeasured.

2.Theterm“distributor”doesnotincluderetailerssellingdirectlytotheultimateconsumer. Retailstoresofall kindsandrestaurantsarenotincludedinthetermsmanufacturerordistributor.

3.WherethemanufacturingprocessbeginsandendsisdescribedinRegulation1.9741(14),whichisavailableon ourwebsiteatwww.state.vt.us/taxorcanbeobtaineddirectlyfromtheVermontDepartmentofTaxes,POBox 547,Montpelier,VT

4.

5.GOODFAITH Ingeneral,asellerwhoacceptsanexemptioncertificatein“goodfaith”isrelievedofliability forcollectionorpaymentoftaxupontransactionscoveredbythecertificate. Thequestionof“goodfaith”is one of fact and depends upon a consideration of all the conditions surrounding the transaction. A seller is presumedtobefamiliarwiththelawandtheregulationspertinenttothebusinessinwhichhedeals.

Inorderfor“goodfaith”tobeestablished,thefollowingconditionsmustbemet:

a.Thecertificatemustcontainnostatementorentrywhichthesellerknows,orhasreasontoknow,is falseormisleading.

b.Thecertificatemustbesubstantiallyliketheformontheotherside.

c.Thecertificatemustbedatedandexecutedinaccordancewiththepublishedinstructions,andmust becompleteandregularineveryrespect.

d.The property to be purchased is of a type ordinarily used in the buyer’s business for the purpose describedinthecertificate.

e.Thecertificatehasbeenreceivedpriortooratthetimeofthesale.

6.IMPROPERCERTIFICATE/LACKOFCERTIFICATE Salestransactionswhicharenotsupportedbyprop- erlyexecutedexemptioncertificatesshallbedeemedtobetaxableretailsales. Theburdenofproofthatthetax wasnotrequiredtobecollectedisupontheSELLER.

7.RETENTION OF CERTIFICATES Certificates must be retained by the seller for a period of not less than three(3)yearsfromthedateofthelastsalecoveredbythecertificate.

8.ADDITIONALPURCHASESBYSAMEBUYER IfthebuyerhasthisasaMultiplePurchasecertificate,the certificatecoversadditionalpurchasesofthesametypeofproperty. Foreachsubsequentpurchase,theseller mustshowsufficientidentifyinginformationonthesalessliptotracethepurchasetotheexemptioncertificate onfile.