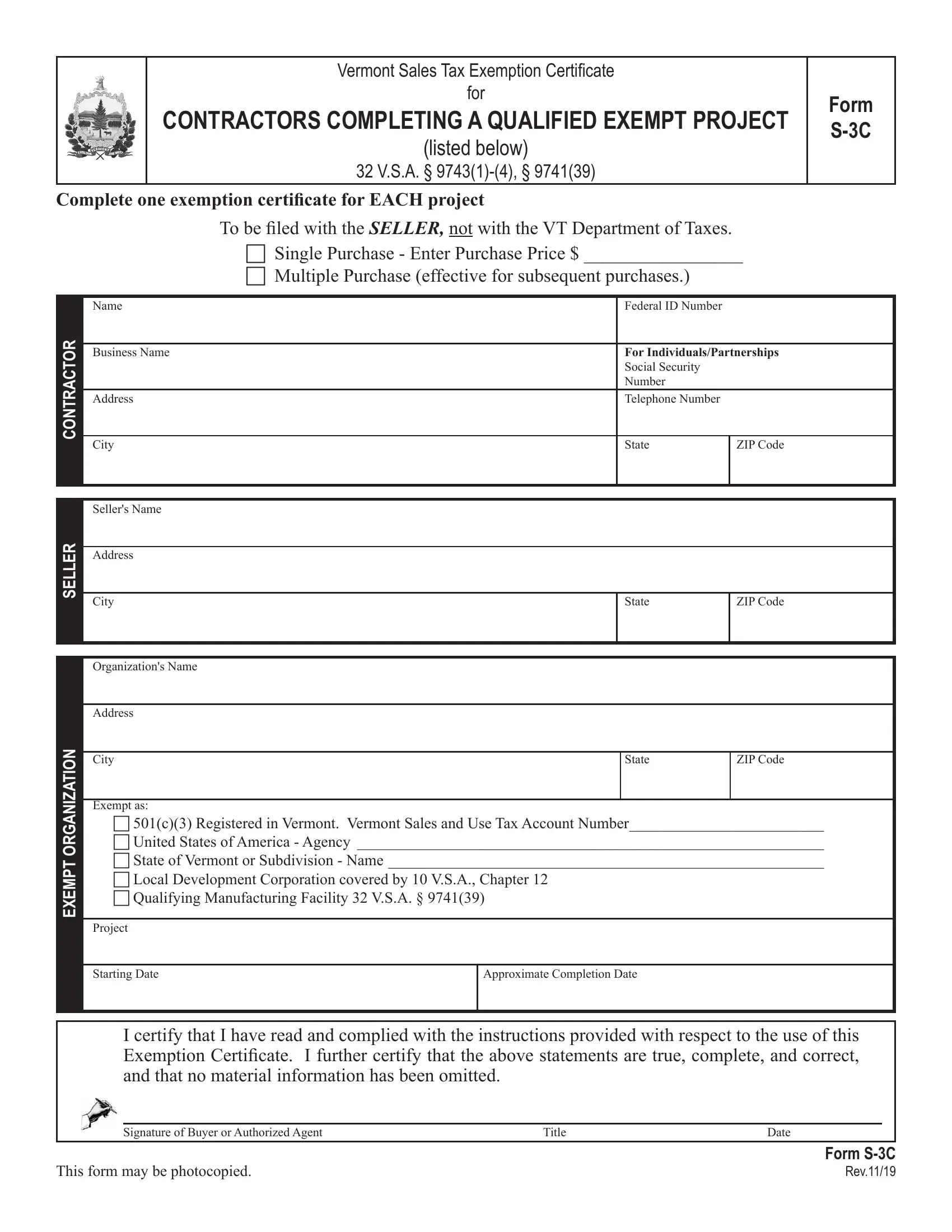

In the realm of construction and contracting within Vermont, navigating tax obligations with precision is paramount, and the S-3C Vermont form emerges as a critical tool in this endeavor for contractors working on qualified exempt projects. This form, rooted in the statutes 32 V.S.A. § 9743(1)-(4), § 9741(39), serves as a Sales Tax Exemption Certificate, enabling contractors to purchase materials and supplies without bearing the brunt of sales tax, provided these purchases are destined for specific exempt projects. It is meticulously designed to cater to a distinct category of purchases, whether they are single or multiple, and requires thorough information from the contractor, including Federal ID or Social Security Number, business details, and specifics about the seller and exempt organization benefitted by the project. Notably, the exemption only applies to tangible personal property that will be integrated into the real estate or consumed in the course of the job, with a clear directive that any deviation, such as the use of materials in a taxable project or purchases of equipment and tools, mandates the payment of use tax. The form underlines the importance of compliance and the need for contractors to furnish it to sellers, not to the Vermont Department of Taxes, embodying a safeguard for both parties through the stipulation of "good faith" acceptance. Furthermore, it delineates qualifying organizations and projects that can benefit from this exemption, highlighting the nuanced criteria that separate eligible from ineligible endeavors and ensuring that the form's misuse is curbed. Emphasized within the document is the seller's responsibility to retain these certificates as proof of tax-exempt sales, outlining a framework designed to streamline tax exemption processes for contractors, sellers, and qualifying organizations while ensuring adherence to Vermont's tax legislation.

| Question | Answer |

|---|---|

| Form Name | Form S 3C Vermont |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | vermont agricultrail tax exempt form, state of vermont tax exempt form, tax exempt form vermont, vermont sales tax exempt form |