Understanding the intricacies of tax forms is fundamental for businesses aiming to leverage available credits to minimize their tax liabilities. Among these, the New York State Department of Taxation and Finance's ST-100.1 form emerges as a critical document for Qualified Empire Zone Enterprises (QEZE). Specifically designed for entities certified under the Empire State Development (ESD) before or after April 1, 2009, this form serves as a quarterly schedule W report, detailing purchases eligible for sales and use tax credit. It’s not just a mere form but a gateway for qualifying businesses in designated jurisdictions—including Allegany County, Cayuga County, city of Auburn, Erie County, Herkimer County, Montgomery County, and Niagara County—to substantiate their eligibility for significant tax relief. The form intricately ties to the ST-100, New York State and Local Quarterly Sales and Use Tax Return, stressing the importance of accurate completion and submission alongside requisite documents such as Form AU-12, Application for Credit or Refund of Sales or Use Tax. Crucially, businesses must verify their eligibility through the Empire Zone Retention Certificate (EZRC) number, pass an employment test for the tax year preceding the period covered by the schedule, and meticulously report eligible purchases by the jurisdiction to claim their dues. This holistic approach underscores the state's effort to balance economic stimulation with precise tax compliance, making the ST-100.1 form a pivotal component of the QEZE program’s fiscal machinery.

| Question | Answer |

|---|---|

| Form Name | Form St 100 1 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 2009, june, 100, New_York |

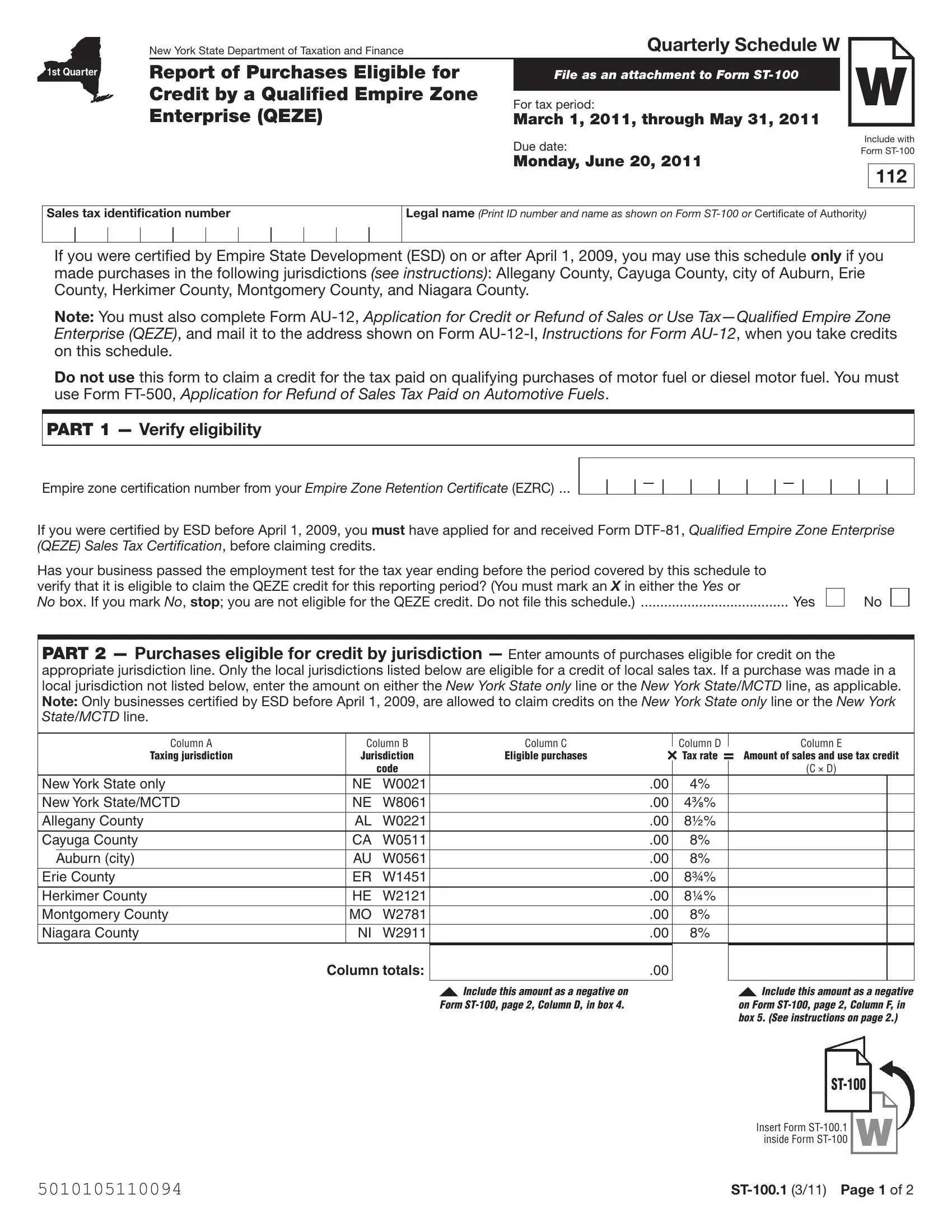

New York State Department of Taxation and Finance

Report of Purchases Eligible for Credit by a Qualified Empire Zone Enterprise (QEZE)

Quarterly Schedule W |

|

|

||

|

W |

|||

FILE AS AN ATTACHMENT TO FORM |

|

|||

|

|

|||

For tax period: |

||||

March 1, 2011, through May 31, 2011 |

|

|

||

Due date: |

Include with |

|||

Form |

||||

Monday, June 20, 2011 |

||||

|

|

|||

|

|

|

112 |

|

Sales tax identification number

Legal name (Print ID number and name as shown on Form

If you were certiied by Empire State Development (ESD) on or after April 1, 2009, you may use this schedule only if you made purchases in the following jurisdictions (see instructions): Allegany County, Cayuga County, city of Auburn, Erie County, Herkimer County, Montgomery County, and Niagara County.

Note: You must also complete Form

Do not use this form to claim a credit for the tax paid on qualifying purchases of motor fuel or diesel motor fuel. You must use Form

PART 1 — Verify eligibility

Empire zone certiication number from your Empire Zone Retention Certificate (EZRC) ...

—

—

If you were certiied by ESD before April 1, 2009, you must have applied for and received Form

Has your business passed the employment test for the tax year ending before the period covered by this schedule to |

|

verify that it is eligible to claim the QEZE credit for this reporting period? (You must mark an X in either the Yes or |

|

No box. If you mark No, stop; you are not eligible for the QEZE credit. Do not ile this schedule.) |

Yes |

No

PART 2 — Purchases eligible for credit by jurisdiction — Enter amounts of purchases eligible for credit on the appropriate jurisdiction line. Only the local jurisdictions listed below are eligible for a credit of local sales tax. If a purchase was made in a local jurisdiction not listed below, enter the amount on either the New York State only line or the New York State/MCTD line, as applicable. Note: Only businesses certiied by ESD before April 1, 2009, are allowed to claim credits on the New York State only line or the New York State/MCTD line.

|

Column A |

Column B |

Column C |

|

Column D |

|

|

Column E |

|

|

Taxing jurisdiction |

Jurisdiction |

Eligible purchases |

× Tax rate |

= |

Amount of sales and use tax credit |

|||

|

|

|

code |

|

|

|

|

|

(C × D) |

New York State only |

NE |

W0021 |

|

.00 |

4% |

|

|

|

|

New York State/MCTD |

NE |

W8061 |

|

.00 |

4⅜% |

|

|

|

|

Allegany County |

AL |

W0221 |

|

.00 |

8½% |

|

|

|

|

Cayuga County |

CA |

W0511 |

|

.00 |

8% |

|

|

|

|

|

Auburn (city) |

AU |

W0561 |

|

.00 |

8% |

|

|

|

Erie County |

ER |

W1451 |

|

.00 |

8¾% |

|

|

|

|

Herkimer County |

HE |

W2121 |

|

.00 |

8¼% |

|

|

|

|

Montgomery County |

MO |

W2781 |

|

.00 |

8% |

|

|

|

|

Niagara County |

NI |

W2911 |

|

.00 |

8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Column totals:

.00

Include this amount as a negative on Form

Include this amount as a negative on Form

Insert Form

5010105110094 |

Quarterly Schedule W Instructions

Report of Purchases Eligible for Credit by a Qualified Empire Zone Enterprise (QEZE)

Report transactions for the period March 1, 2011, through May 31, 2011.

Who may file

Complete and file Form

If you are taking credits on this schedule, you must also complete Form

The application must state that the credit has been claimed on a sales tax return and the period covered by that return. Supporting documentation must be filed with Form

If you were certified by Empire State Development (ESD) before April 1, 2009, you must have:

•

• receivedyourEmpire Zone Retention Certificate (EZRC) from ESD; and

• passedtheemploymenttestforthetaxyearendingbeforethe period covered by this schedule.

If you meet these qualifications, you may use this form to claim a credit for tax paid on qualifying purchases.

If you were certified by ESD on or after April 1, 2009, you must have:

• receivedyourEZRCfromESD;and

• passedtheemploymenttestforthetaxyearendingbeforetheperiod covered by this schedule.

If you meet these qualifications, you may use this form to claim a credit for tax paid on qualifying purchases, but only if the qualifying purchase is made in a locality that has elected to provide the credit. The following localities are currently eligible:

Allegany County

Cayuga County Auburn (city) Erie County Herkimer County Montgomery County Niagara County

If the locality where you made the purchase is not listed as an eligible locality, no credit of any taxes (State, MCTD or local) is available.

Specific instructions

Identification number and name — Print the sales tax identification number and legal name as shown on Form

PART 1 — Verify eligibility

EZRC number — Print the empire zone certification number from your EZRC issued by ESD.

Employment test — You must complete and pass the employment test using your employment numbers for the tax year ending before the period covered by Form

If your credit or refund claim covers periods from more than one tax year, you must complete the employment test for each tax year required.

Example: A business was certified by ESD with an effective date of February 15, 2008, on its Certificate of Eligibility. The business applied for and received QEZE sales tax certification from the Tax Department effective October 1, 2008. The business files taxes on a calendar year basis.

At the end of December 2008, the business completed the employment test for the 2008 tax year (January through December 2008) and determined that it qualifies for QEZE sales tax benefits for 2009.

At the end of December 2009, the business completed the employment test for the 2009 tax year (January through December 2009) and determined that it qualifies for QEZE sales tax benefits for 2010.

In March 2010, the business files Form

When filing Form

Mark an X in the Yes or No box if your business has passed the employment test for the tax year ending before the period covered by this schedule to verify that it is eligible to claim the QEZE credit. If you mark No, stop; you are not eligible for the QEZE credit. Do not file this schedule.

PART 2 — Purchases eligible for credit by jurisdiction

Column C — Eligible purchases — Enter in Column C your purchases eligible for credit on the appropriate jurisdiction line.

If you were certified by ESD before April 1, 2009, use the jurisdiction line for the locality where the purchase was made. If a purchase was made in a local jurisdiction that is not listed, enter the amount on either the New York State only 4% line or the New York State/MCTD 43/8% line, as applicable.

If you were certified by ESD on or after April 1, 2009, credit is only allowed if the jurisdiction has elected to provide this credit (Allegany County, Cayuga County, city of Auburn, Erie County, Herkimer County, Montgomery County and Niagara County). If the locality has not made this election, no credit of any taxes (State, MCTD and local) is allowed. Do not make any entries on either the New York State only 4% line or the New York State/MCTD 43/8% line.

Column E — Amount of sales and use tax credit — For each jurisdiction, multiply the amount in Column C by the tax rate in Column D, and enter the resulting credit amount in Column E. After entering information for all jurisdictions required, separately total Columns C and E. Include the column totals on Form

Note: You may only take credit for the amount of tax owed on

Form

Filing this schedule

File a completed Form

Need help? and Privacy notification

See Form

5010205110094 |