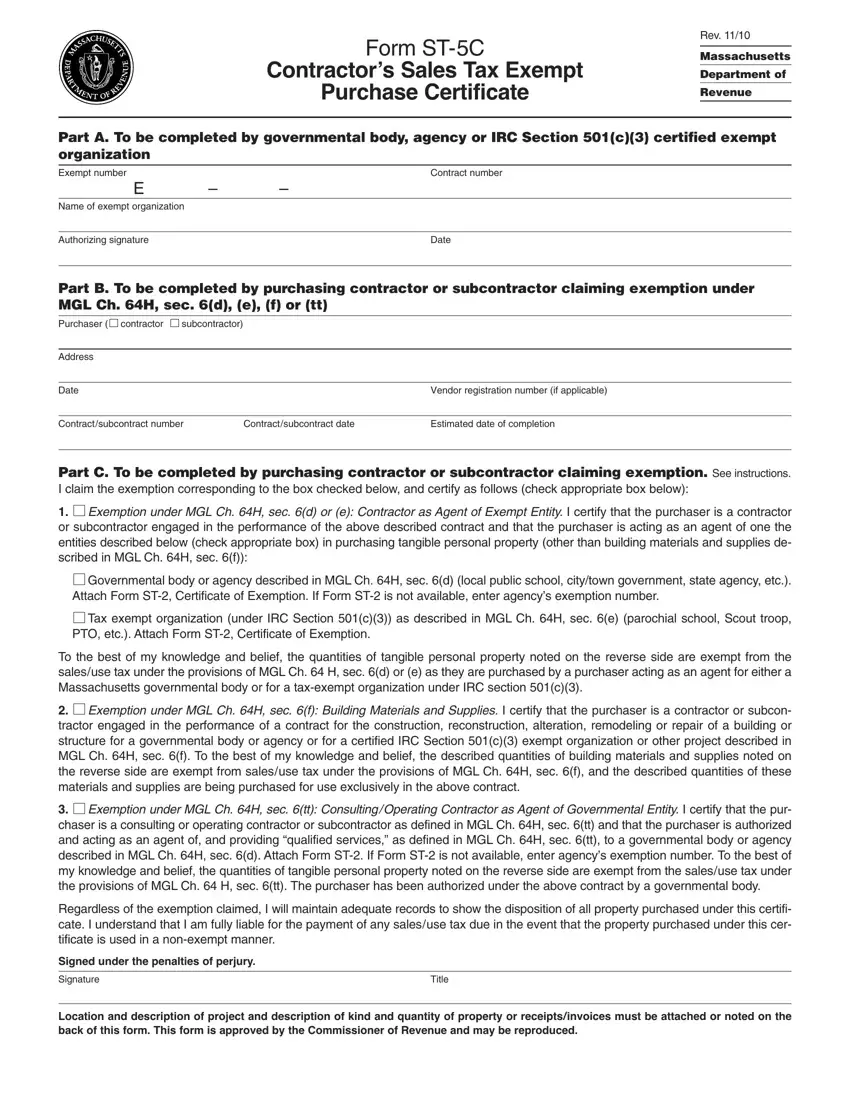

In the realm of construction and contracting within Massachusetts, understanding the application and scope of Form ST-5C is crucial for those engaged in projects with tax-exempt entities, including governmental bodies and IRC Section 501(c)(3) organizations. This Contractor’s Sales Tax Exempt Purchase Certificate, a vital document issued by the Massachusetts Department of Revenue, serves as a linchpin for contractors and subcontractors aiming to navigate the complexities of sales tax exemptions on their purchases. The form is meticulously structured into several parts to ensure comprehensive compliance and clarity. Part A necessitates input from the tax-exempt entity authorizing the exemption, while Part B and C are completed by the purchasing contractor or subcontractor, making claims under specific sections of Massachusetts General Law (MGL) Chapter 64H, section 6. These claims span various exemptions, including for building materials and supplies, as well as for purchases made by consultants or operating contractors acting as agents for a governmental body. The form not only facilitates the exemption process but mandates contractors to maintain detailed records to substantiate the exempt nature of their purchases, underlining the responsibility that accompanies the privilege of tax exemption. The penalty for misuse of this certificate underscores the serious nature of its application, serving as a reminder of the legal obligations that tie into the procurement process in tax-exempt scenarios. With additional support available through the Customer Service Bureau, this form embodies a critical resource for those engaged in exempt projects, ensuring compliance with state sales tax laws while supporting the completion of projects that benefit public and charitable interests.

| Question | Answer |

|---|---|

| Form Name | Form St 5C |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | st5c tax, st 5c form massachusetts, st5c, massachusetts form tax exempt |