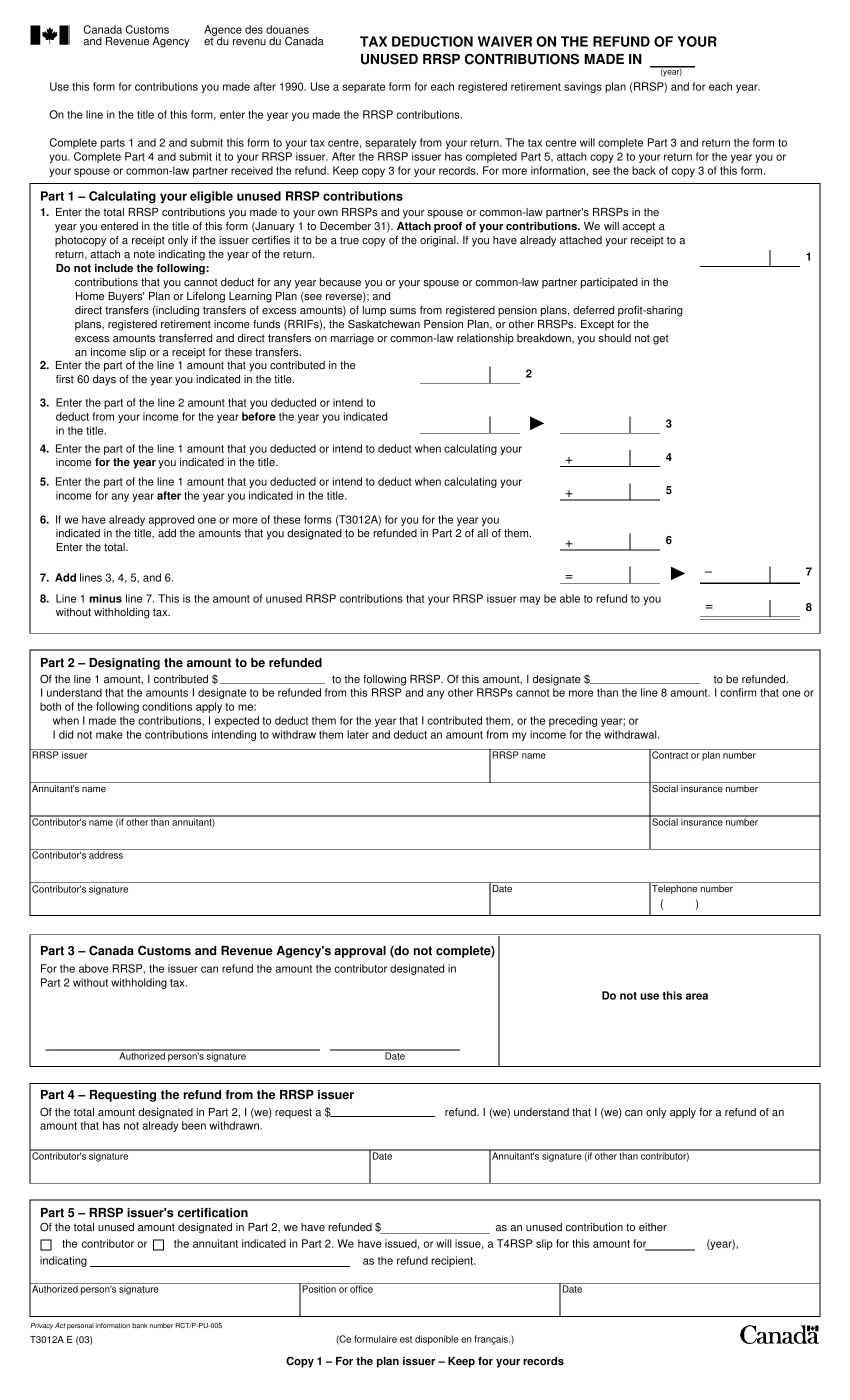

Navigating through Canada's tax system can seem daunting, especially when dealing with specific forms like the T3012A E form, crucial for individuals managing their Registered Retirement Savings Plan (RRSP) contributions. This form, which might not be familiar to everyone, plays a pivotal role for Canadians who have made unused RRSP contributions after 1990 and are seeking a tax deduction waiver for the refund of these contributions. The process is detailed and requires attention to each part: from calculating your eligible unused RRSP contributions to having the Canada Customs and Revenue Agency approve the tax deduction waiver. This includes carefully filling out parts 1 and 2, submitting the form to your tax centre, and then to your RRSP issuer, who, after completing their part, allows you to attach the necessary documentation to your tax return. Understanding the conditions under which you can request a refund without withholding tax, proving your contributions, and correctly reporting the refund on your tax return are all steps meticulously outlined in the T3012A E form instructions. Moreover, it’s essential to remember not to include contributions under certain conditions like those made under the Home Buyers' Plan or Lifelong Learning Plan, highlighting the form’s specificity to certain types of RRSP contributions.

| Question | Answer |

|---|---|

| Form Name | Form T3012A E |

| Form Length | 2 pages |

| Fillable? | Yes |

| Fillable fields | 1 |

| Avg. time to fill out | 42 sec |

| Other names | Agence, rrsp over contribution form, franais, RCT |