The Thrift Savings Plan (TSP) offers federal employees and members of the uniformed services a way to save for retirement, combining the benefits of a traditional pension plan with those akin to a 401(k). For individuals looking to potentially maximize their retirement savings through Roth contributions, the TSP-60-R form serves as a critical bridge. Specifically designed to facilitate the transfer of Roth money from existing Roth 401(k), 403(b), or 457(b) plans into the TSP, this form underscores a strategic move for those aiming to consolidate their Roth balances under the TSP’s umbrella. Crucially, it's worth noting that the TSP draws a line by not permitting transfers from Roth IRAs. Accuracy and compliance with the specific stipulations laid out in the form are paramount, as the form mandates thorough personal information, and requires certification from both the participant and the plan administrator from which the funds are originating. This process not only necessitates a clear understanding of one’s current retirement savings structure but also a strategic foresight into how such transfers fit into broader financial planning for retirement. The form's fine print highlights the importance of a completed TSP-60-R form and a corresponding check to ensure a smooth transaction, alongside detailed stipulations about the eligibility of the Roth money being transferred, making it essential for participants to review their distribution's qualifications with their plan representative beforehand.

| Question | Answer |

|---|---|

| Form Name | Form Tsp 60 R |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | fillable tsp 60, tsp60 r fillable form, how to fill out the tsp 60, tsp 60 |

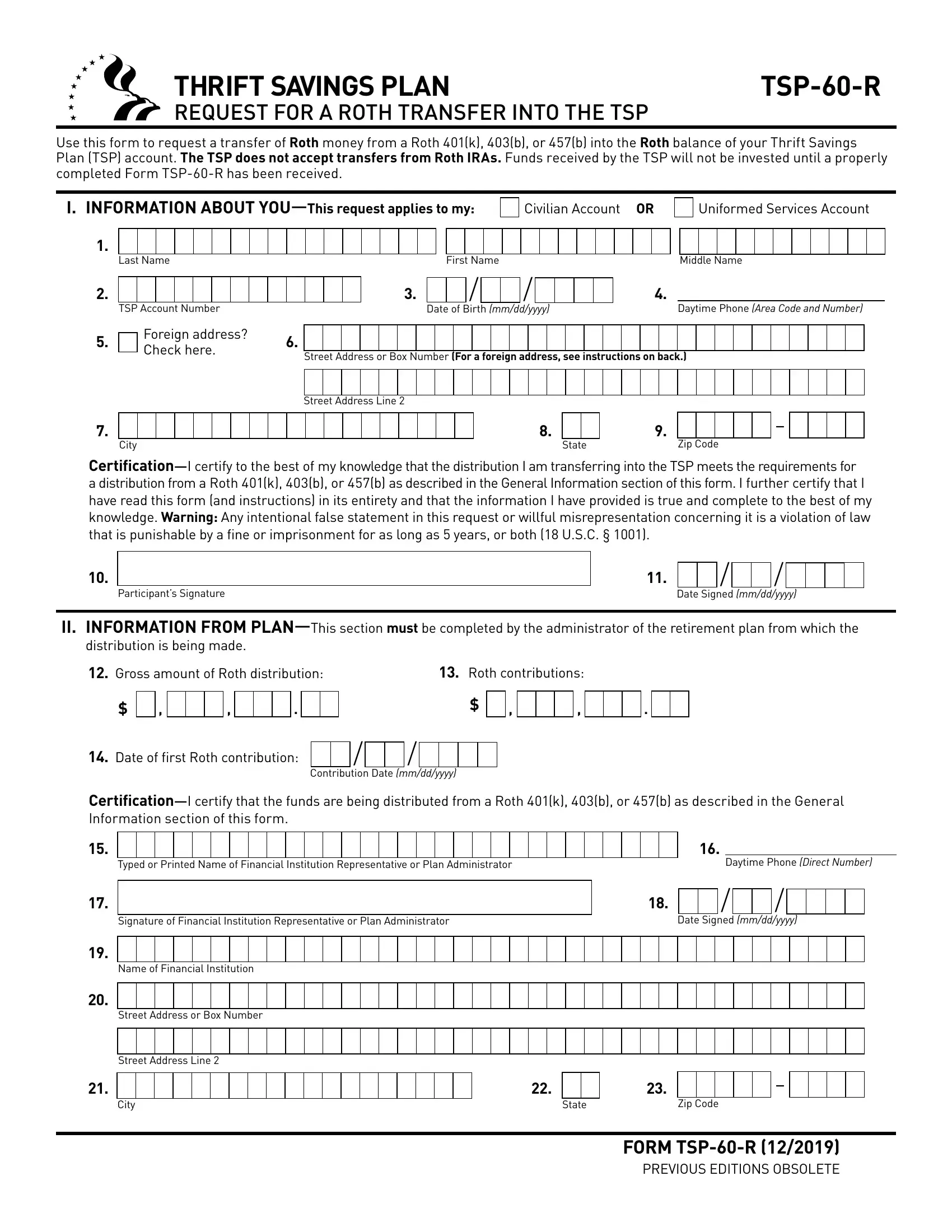

THRIFT SAVINGS PLAN |

REQUEST FOR A ROTH TRANSFER INTO THE TSP

Use this form to request a transfer of Roth money from a Roth 401(k), 403(b), or 457(b) into the Roth balance of your Thrift Savings Plan (TSP) account. The TSP does not accept transfers from Roth IRAs. Funds received by the TSP will not be invested until a properly completed Form

I.INFORMATION ABOUT

Civilian Account OR

Uniformed Services Account

1.

2.

5.

Last NameFirst NameMiddle Name

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

/ |

|

|

|

/ |

|

|

|

|

|

|

4. |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

TSP Account Number |

|

|

|

|

|

|

|

|

|

|

Date of Birth (mm/dd/yyyy) |

|

|

|

|

|

|

|

|

|

Daytime Phone (Area Code and Number) |

||||||||||||||||||||||||||||||

|

Foreign address? |

6. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Check here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

Street Address or Box Number (For a foreign address, see instructions on back.) |

|||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street Address Line 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

7.

City

8.

State

9.

Zip Code

–

10.

Participant’s Signature

11.//

Date Signed (mm/dd/yyyy)

II.INFORMATION FROM

12. |

Gross amount of Roth distribution: |

|

|

|

|

|

13. Roth contributions: |

|

|

|

||||||||||||||||||||||||

|

$ |

|

, |

|

|

|

, |

|

|

|

. |

|

|

|

|

|

|

$ |

|

|

, |

|

|

|

, |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

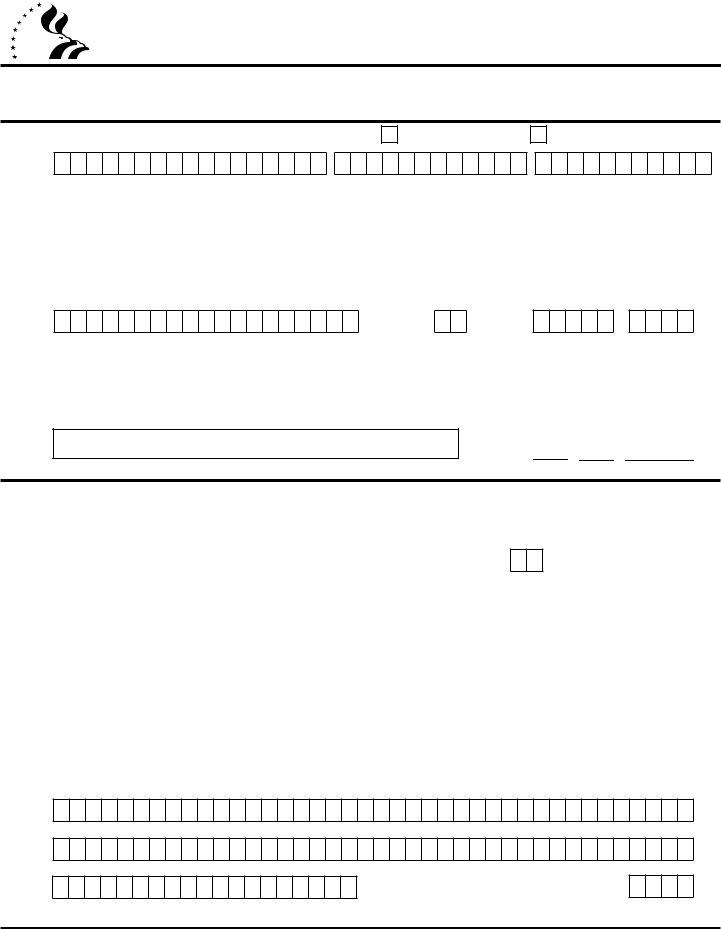

14. |

Date of first Roth contribution: |

|

|

|

|

/ |

|

|

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

Contribution Date (mm/dd/yyyy) |

|

|

|

|

|

|

|

|

|

|||||||||||||

.

15.

17.

19.

20.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16. |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Daytime Phone (Direct Number) |

|||||||||

Typed or Printed Name of Financial Institution Representative or Plan Administrator |

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18. |

|

|

/ |

|

|

/ |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Signature of Financial Institution Representative or Plan Administrator |

Date Signed (mm/dd/yyyy) |

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Financial Institution

Street Address or Box Number

Street Address Line 2

21.

City

22. |

|

|

23. |

|

|

|

|

|

– |

|

State |

Zip Code |

|||||||

FORM

PREVIOUS EDITIONS OBSOLETE

FORM

Use this form to request a transfer of Roth money from a Roth 401(k), 403(b), or 457(b) into the Roth balance of your Thrift Savings Plan (TSP) account. The TSP does not accept transfers from Roth IRAs. You must have an open TSP account with a balance when your request is received by the TSP. Note: Money cannot be transferred into a beneficiary participant account.

The TSP is a retirement savings and investment plan for federal employees and members of the uniformed services. Congress established the TSP in the Federal Employees’ Retirement System Act of 1986. The TSP is to be treated as a trust described in 26 U.S.C. § 401(a), which is exempt from taxation under

26 U.S.C. § 501(a). TSP regulations are published in title 5 of the Code of Federal Regulations, Parts

You must complete Section I of this form, then provide the entire package to your plan administrator to complete Section II. In order for your request to be processed, it must include a completed Form

Note: If you intend to make a withdrawal from your TSP account, please wait until you receive confirmation that your transfer has been completed before requesting the withdrawal.

SECTION I. Complete Items

and the address you provide on this form is different from the address in your TSP record, have your agency or service submit an address change for you. If you are separated from federal service or the uniformed services, you can update your address on tsp.gov.

The address on this form cannot be used to update your TSP record.

If you have a foreign address, check the box in Item 5 and enter the foreign address as follows in Items

First address line: Enter the street address or post office box number, and any apartment number.

Second address line: Enter the city or town name, other principal subdivision (e.g., province, state, county), and postal code, if known. (The postal code may precede the city or town.)

City/State/Zip Code fields: Enter the entire country name in the City field; leave the State and Zip Code fields blank.

Read the General Information section of this form, and sign and date Items 10 and 11 if the information is correct. If you cannot certify that your transfer meets all of the requirements described, you cannot transfer your distribution into the TSP.

If you have questions, call the ThriftLine toll free at

SECTION II. The instructions for Section II are intended for the plan representative.

If you are unwilling to complete this section, submit an IRS Letter of Determination or a letter on the organization’s letterhead confirming that the funds are being transferred from a qualified plan. Otherwise, we cannot deposit the funds into the participant’s account.

You must submit the completed Form

Either mail the check and form to:

|

TSP Rollover and Transfer Processing Unit |

|

P.O. Box 385200 |

|

Birmingham, AL |

Or fax to: |

|

|

If you fax this form, please send your check immediately to the TSP.

Item 12. Indicate the total gross amount of the Roth distribution that is being made from the plan.

Item 13. Indicate the amount of the distribution that comes from the participant’s designated Roth contributions (i.e., tax basis).

Item 14. Provide the specific date of the participant’s first designated Roth contribution to the plan. If you cannot provide the specific date, indicate the year that the participant made his or her first designated Roth contribution to the plan.

Items

Form

PREVIOUS EDITIONS OBSOLETE

FORM

Form

If the TSP does not receive a Form

If the TSP receives a check with appropriate identification, but without Form

Be sure to read all of the General Information and Instructions before you complete this form.

What Roth distributions will the TSP accept?

The TSP will only accept transfers of qualified and nonqualified Roth distributions from any applicable retirement plan, as defined in Internal Revenue Code (IRC) § 402(e)(1), under which an employee may elect to make Roth contributions. An applicable retirement plan includes a plan qualified under IRC § 401(a) (e.g., a 401(k) plan); an IRC § 403(b)

§457(b) plan maintained by a governmental employer. It does not include a Roth IRA.

The TSP will not accept rollovers of qualified or nonqualified Roth distributions that have already been paid to you.

To be accepted into the TSP, the distribution must be an “eligible rollover distribution.” An eligible rollover distribution is a distribution to a participant of all or a portion of his or her account. However, it cannot be

•one of a series of substantially equal periodic payments made over the life expectancy of the employee (or the joint lives of the employee and designated beneficiary, if applicable), or for a period of 10 years or more;

•a minimum distribution required by IRC § 401(a)(9);

•a hardship distribution;

•a plan loan that is deemed to be a taxable distribution because of default; or

•a return of excess elective deferrals.

Examples of eligible rollover distributions include a lump sum distribution after terminating employment, an

10 years, death benefit payments, or payments made to a spouse or former spouse pursuant to a qualified domestic relations order (QDRO).

Before submitting this form, a TSP participant who would like to transfer Roth money into the TSP should check with a representative of his or her plan to determine what portion of a distribution (if any) meets the applicable requirements.

Note: Participants are required to certify in Section I of this form that the distribution they are seeking to transfer into the TSP meets the applicable requirements. If a participant cannot sign the certification, the TSP cannot accept the transfer.

What is the difference between a “qualified” and a “nonqualified” Roth distribution?

A Roth distribution is considered qualified (i.e., paid

What is a “Roth Initiation Date”?

The TSP defines a Roth Initiation Date as the specific date of a participant’s first Roth contribution. The IRS uses January 1 of the calendar year associated with a participant’s first Roth contribution to determine whether Roth earnings are qualified.

What happens to a Roth Initiation Date at the time of a transfer?

If a participant has an existing Roth balance in his or her TSP account at the time of the transfer, the Roth Initiation Date will be the earlier of either the start date associated with the incoming Roth balance or the start date associated with the existing TSP Roth balance. This date will be applied to all Roth money already in the participant’s TSP account, as well as any future Roth contributions to the TSP.

If a participant does not have an existing Roth balance in his or her TSP account, the transfer will establish one, and the Roth Initiation Date will be the start date associated with the incoming Roth balance.

How much Roth money can a participant transfer or roll over into the TSP?

There is no limit to the number of transfers of Roth money that a participant can make. A participant can transfer all or any part of a Roth distribution that meets the applicable requirements.

However, a participant cannot roll over any Roth money into the TSP.

What is the difference between a “transfer” and a “rollover”?

A transfer (also known as a “direct rollover”) occurs when the participant instructs the distributing plan to send all or part of his or her eligible rollover distribution directly to the TSP instead of issuing it to the participant.

A rollover occurs when the distributing plan makes a payment to the participant (after withholding the applicable federal income tax) and the participant deposits all or any part of the gross amount of the payment into the TSP within 60 days of receiving it.

*Note to participant: The TSP cannot certify to the IRS that you meet the Internal Revenue Code’s definition of disability when your taxes are reported. Therefore, you must provide the justification to the IRS when you file your taxes.

Form

PREVIOUS EDITIONS OBSOLETE

FORM

What happens to the money once it reaches the TSP?

Money that is transferred into the TSP is allocated to the TSP investment funds according to the participant’s most current contribution allocation on file. Once the money is deposited into the participant’s TSP account, it is treated like employee contributions and will be subject to the same plan rules as all other employee contributions in the account. These rules may be different from the rules of the plan from which the transferred amount was distributed.

Note: Because the conditions under which the TSP will accept transfers and rollovers are strict, and there may be tax consequences, we recommend that you consult your tax advisor before you move money into the TSP.

How does the IRC annual elective deferral limit affect transfers?

Money that is transferred into the TSP is not applied to the annual elective deferral limit that is imposed on regular employee contributions.

How does a transfer affect installment payments?

If a TSP participant is receiving installment payments of a fixed dollar amount at the time of a transfer or a rollover, and the amount being transferred or rolled over is $1,000 or more, the TSP will recalculate the duration of the installment payments. The recalculation will take place at the time the transfer or rollover is processed. If the payment duration goes from less than 10 years to 10 years or more, the payments will no longer be eligible for transfer or rollover to an IRA or eligible employer plan. Tax withholding options will also change.

Participants receiving installment payments based on life expectancy have their payment amounts recalculated annually at the time of their first payment of the year. Transfers and rollovers into the TSP affect this recalculation by increasing the account

For more information, see the TSP tax notice Tax Information for TSP Participants Receiving Installment Payments.

What

The TSP will accept both transfers and rollovers of

§402(c)(8)(B). An eligible retirement plan includes a traditional individual retirement account (IRA), a SIMPLE IRA to which the participant has contributed for at least 2 years, and an eligible employer plan.

If you would like to transfer or roll over a distribution from an eligible retirement plan into the traditional

PRIVACY ACT NOTICE. We are authorized to request the information you provide on this form under 5 U.S.C. chapter 84, Federal Employees’ Retirement System. We will use this information to identify your TSP account and to process your request. In addition, this information may be shared with other federal agencies for statistical, auditing, or archiving purposes. We may share the information with law enforcement agencies investigating a violation of civil or criminal law, or agencies implementing

a statute, rule, or order. It may be shared with congressional offices, private sector audit firms, spouses, former spouses, and beneficiaries, and their attorneys. We may disclose relevant portions of the information to appropriate parties engaged in litigation and for other routine uses as specified in the Federal Register. You are not required by law to provide this information, but if you do not provide it, we will not be able to process your request.

Form

PREVIOUS EDITIONS OBSOLETE